This support note applies to:

-

AO Statutory Reporter (NZ)

-

AE Statutory Reporter (NZ)

-

Workpapers (NZ)

We've made some improvements to the Tax Note in Statutory Reporter version 5.4.29.

The Tax Note provides a reconciliation of profit in the Profit and Loss Statement to the Taxable profit amount shown in the Tax return.

The Tax Note allows you to make several types of adjustments such as:

-

non-deductable expenses and non-assessable income

-

timing differences (deferred holiday pay, provision for doubtful debts)

-

losses brought forward.

to arrive at a taxable profit.

The steps below are a guide on how to set up your ledger for reporting in the Tax Note.

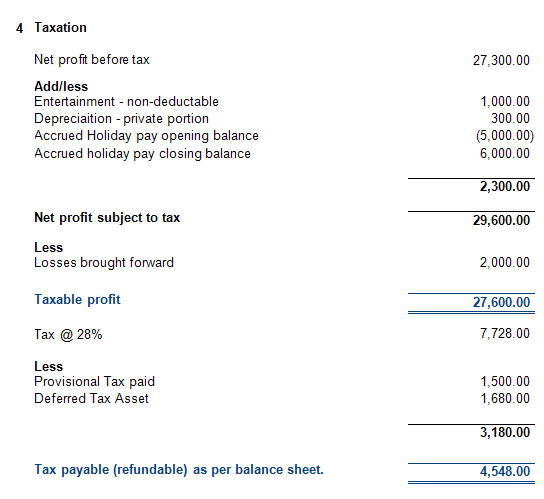

Example result

Using this approach, your Financial Statements should look similar to the following.

In this example, we've used the following balances:

-

$27,300.00 of Accounting income

-

$1,300 of non-deductible expenses

-

Deferred accrued holiday pay:

-

$5,000 at the beginning of the year

-

$6,000 at the end of the year (therefore actual amount of deferred tax at end of year is $6,000 x 28% = $1,680)

-

-

$2,000 of ax losses brought forward of

-

$1,500 provisional tax paid during the year.

Tax expense on Income Statement

Tax Note

Balance Sheet:

Notes to Balance Sheet - Tax Note

MYOB INTERNAL STAFF ONLY

CAT-28451