Deductions relating to Australian investment income (dai)

The dai worksheet is tailored to meet the needs of the type of return to which it is attached.

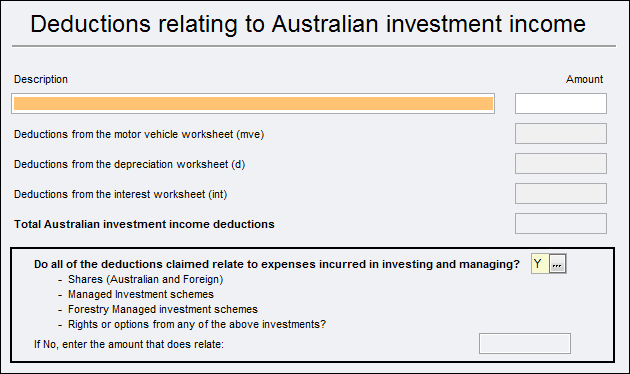

The dai worksheet is mandatory at item 16. This item is closed to data entry.

Enter deductions relating to Dividends received whether directly from a Company, listed or unlisted, or by Distribution from a Managed investment trust into the worksheet at this item and not at item 18.

Amounts entered in this worksheet, together with amounts that have been integrated from the Motor vehicle worksheet (mve), the Depreciation worksheet (d), and the deductions field of the Interest income worksheet (int) will be totalled and returned at label P in the main return.

If the Partnership was paid a dividend by a LIC directly and the dividend included a LIC capital gain amount, the Partnership can claim a deduction of 50% of the LIC capital gain amount. The listed investment company's dividend advice statement shows the LIC capital gain amount:

If all the expenses do not relate to income from investments, then change the answer to No and enter the unrelated amount in the field provided. The amount will be pre-filled to item 50, label G from where it will be transferred to the Distribution Statement to be distributed to the partners in their respective percentage interest in the Partnership. The Partner will need this amount when completing their personal income tax returns.

Deleting the dai worksheet from the return

To delete the worksheet entirely you should open the dai and check for amounts that have been integrated from the Motor vehicle worksheet (mve), the Depreciation worksheet (d), and the Interest income worksheet (int). If these are present, then you need to open those worksheets and set the relevant amounts to zero or delete the worksheets entirely.

When the integrated values in the dai worksheet are cleared, you can manually clear the content of the dai or delete it entirely.

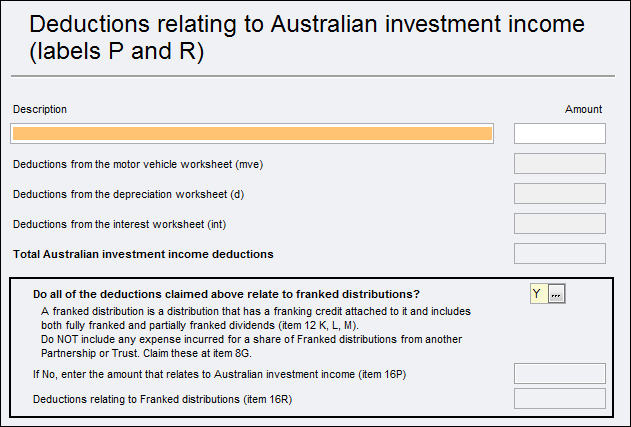

Amounts entered in this worksheet, together with amounts that have been integrated from the Motor vehicle worksheet (mve), the Depreciation worksheet (d), and the deductions field of the Interest income worksheet (int) will be totalled and returned at label P and/or label R in the main return in accordance with the dissection in the new Franked Distribution field below.

If the trust was paid a dividend by a LIC directly and the dividend included a LIC capital gain amount, the trust can claim a deduction of 50% of the LIC capital gain amount. The listed investment company's dividend advice statement shows the LIC capital gain amount:

If the LIC dividend is franked (either fully or partially) then include any deduction relating to a LIC capital gain in the Franked distributions field second from the bottom of the worksheet so that it is included in any amount that is to be integrated to label R.

If the LIC dividend is unfranked, then it will automatically be included in the amount that is integrated to label P.

The listed investment company's dividend advice statement shows the LIC capital gain.

If you change the answer to No, then you must enter the amount of the Total Australian investment income deductions in the field provided as this amount will affect the amount of Franked Distributions available for distribution to presently entitled beneficiaries at item 54.