Item 1 - salary, wages, commissions, bonuses etc

See Item 1 Income on the ATO website.

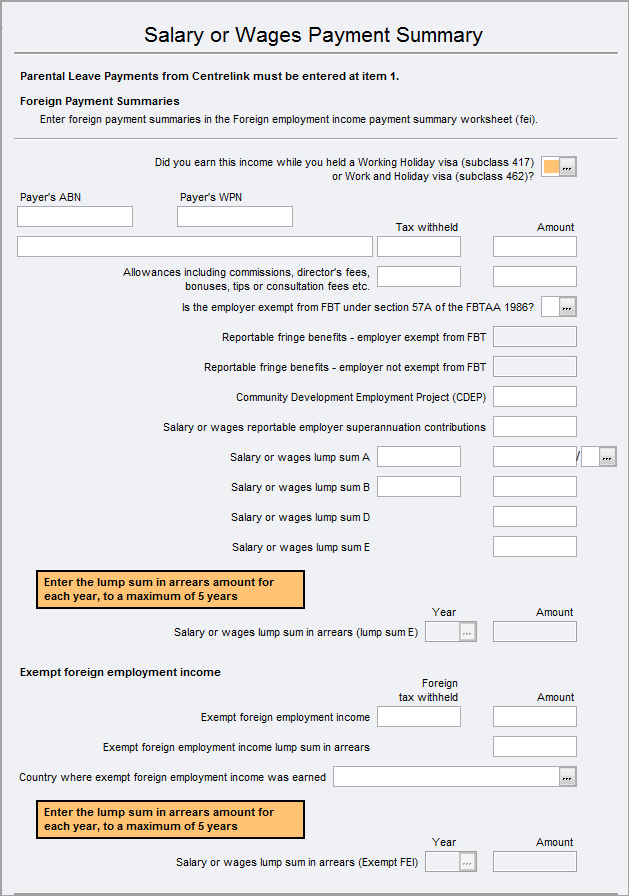

- Read the on-screen text and select Yes at the 416 or 462 working holiday visa question. We'll calculate tax at 15% on WHM income up to $37,000 earned during the current income year.

- Enter the Payer's ABN, WPN, Tax withheld and Amount.

- We'll populate Item 1 with the details and type H.

- Go to Item A4 in the Adj/Credits tab and select Label D - Working holiday maker net income. The working holiday maker net income worksheet opens

- Income from Item 1 is populated in the working holiday maker net income worksheet.

Complete the Salary and wages payment summary (egc) to report Australian income at Item 1. You can report up to 57 payments using this worksheet.

New fields in the worksheet

There are some new fields in the egc worksheet:

| Fields | Description |

|---|---|

| Is the employer exempt from FBT under section 57A of the FBTAA 1986? | Select Y/N at this question. This will enable/disable the Reportable fringe benefits - employer exempt and Reportable fringe benefits - employer not exempt from FBT |

| Community Development Employment Project (CDEP) | This amount is also reported at Item 5 - Australian Government allowances and payments like Newstart, Youth Allowance,Jobseeker and Austudy payments. |

| Salary or wages lump sum D | Genuine redundancy payments |

| Salary or wages lump sum E | lump sum in arrears (LSIA) payments |

| Salary or wages lump sum in arrears - Year/Amount | This filed will be enabled if you've entered an amount at Salary or wages lump sum E. |

| Exempt foreign employment income tax withheld and amount | This amount is also reported at Item 20 - Foreign source income and foreign assets or property |

| Exempt foreign employment income lump sum in arrears | This amount is also reported at Item 20 - Foreign source income and foreign assets or property |

| Country where exempt foreign employment income was earned | This amount is also reported at Item 20 - Foreign source income and foreign assets or property |

| Salary or wages lump sum in arrears (Exempt FEI) - Year/Amount | This field will be enabled if you've entered an amount at Exempt foreign employment income lump sum in arrears. |

Each payment can be broken down to a maximum of 5 years. Press CTRL + INSERT to add a record.

In MYOB Tax, you will also enter Reportable Fringe Benefits and Reportable Superannuation contributions that are notified on the PAYG Payment Summary. These amounts are passed to the Income Test Items IT1 and IT2 respectively.

From 1 July 2017, Reportable fringe benefits are reported separately in accordance with their exemption status under section 57A of the FBTAA 1986. Enter this amount at the correct field as defined on the Payment Summary.

If you received any reportable fringe benefits amounts of $3,773 or more, enter those amounts at the relevant field in the Reportable fringe benefits box. Do not enter amounts that are less than $3,773 as this will affect the calculation of the Adjusted taxable income (ATI) that is used for defining eligibility for some offsets, for example, dependency offsets and SAPTO.

Complete the Foreign employment income payment summary (fei) to report Foreign employment income at Item 1. You can report only 3 foreign employment payment summaries.