Item 20 - Foreign source income and foreign assets or property

See Item 20 - Foreign source income on the ATO website for further information.

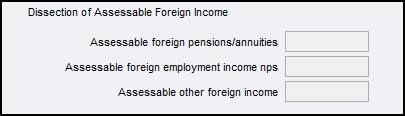

Assessable foreign pension/annuities: Is the total of labels L and D.

Assessable foreign employment income nps: Is the total of worksheet at Label T.

Assessable other foreign income: Is the gross income associated with amounts at labels R, M and F prior to any expenses incurred in earning that income and covers foreign rental income, other foreign source income other than foreign salary or wages and foreign pensions or annuities, and Australian franking credits from a New Zealand company.

We pass the sum of these two fields to label E Assessable foreign source income.

Click this link for the information on Item 20 - Foreign source income on the ATO website.

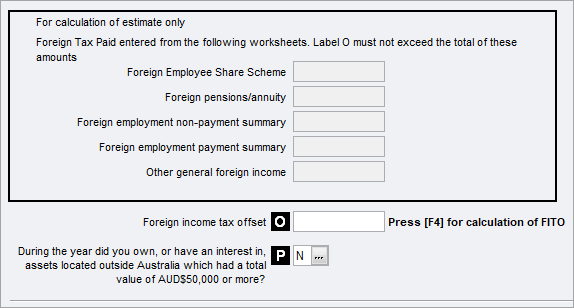

The amount at label U is made up of:

- Item 1 Salary or wages with the Code F (including any additional entries made in the Additional PAYG Summary worksheet (egc)), plus

- any amount of a lump sum payment in arrears on which foreign income tax has been paid, less

- any amount included at items D1 to D5 that have been keyed in the screen behind this label.

There may be an entitlement to a foreign income tax offset for the difference between the foreign tax paid and the Australian tax payable on that income.

The holding dialog at label U provides a breakdown of the amount at the label.

When the foreign source income worksheet (for) is completed and saved, label O will be closed to data entry. Because of the complexity of the foreign tax credit calculation, integration to label O is only performed when you click F4 to produce the Estimate.

If you are not using the worksheets but have entered amounts directly in the fields in the special calculator only box ‘For calculation of estimate only’, then you must not enter an amount at label O. When you click F4 the calculator will fill label O from the amounts you've already entered elsewhere.

To refresh the value at label O, you must press F4 each time any of the amounts at this item are changed.

F4 and the Generic worksheet at label O

Tax has a schedule of one sort or another behind every label. Where there is no ATO schedule, tailored worksheet, grid or holding dialog for the particular label or field, Tax automatically opens a Generic Schedule.

Do NOT attach a Generic schedule to label O as this prevents the F4 function from refreshing label O.

If you have attached a generic schedule, then you must delete it. To do that, select Preparation > Delete Schedules and remove the entry titled ‘foreign income tax offset field (E135)’.

Once the generic worksheet is removed, click F4 to see the value at label O updated.