Item 7 - Reconciliation to taxable income or loss

Reconciliation items are adjustments for tax purposes to reconcile the book Total profit or loss at item 6 label T, to Taxable income or loss at item 7 label T.

Use the worksheets Other Additions Items (add) and Other Subtraction Items (sub) to assist with the reconciliation. All figures entered will be passed to the correct label in the main return.

See Other Addition Items worksheet (add) and Other Subtraction Items worksheet (sub).

Companies that have one or more CGT events during the income year must complete a Capital gains tax schedule (BW) to lodge with the current year return if:

- total current year capital gains are greater than $10,000, or

- total current year capital losses are greater than $10,000.

Show at this label any expenditure incurred in deriving exempt income included at item 7 label V.

Do not include

Expenditure incurred in deriving exempt income from retirement savings accounts (RSAs) and debt deductions allowed by section 25-90 of the ITAA 1997.

Click label U to open the Generic Schedule / Worksheet.

Show at this label the amount of franking credits attached to assessable distributions received from Australian corporate tax entities.

Do NOT include franking credits attached to:

A distribution the company receives indirectly through one or more partnerships or trusts. Include these at label D Gross distribution from partnerships item 6 or label E Gross distributions from trusts item 6.

A distribution that is exempt income or non-assessable non-exempt income, or

Franked distributions received from a New Zealand franking company. Include these at item 7, label C - Australian franking credits from a New Zealand company, or

A distribution where the shares are not held at risk as required under the holding period and related payments rules, or there is other manipulation of the imputation system. There is no entitlement to a franking tax offset in these circumstances.

Under the simplified imputation system a company is required to include in its assessable income the amount of franking credits attached to assessable franked distributions received.

Click label J to open the Dividends Worksheet for entities (div). All amounts will be passed passed to the relevant fields in the income tax return.

Maximum franking credit allowable

The maximum franking credit that can be allocated to a frankable distribution is based on a company's corporate tax rate for imputation purposes. For the current income year, a company's corporate tax rate for imputation purposes may be either 27.5% or 30% depending on the company's circumstances.

For most companies the sum of all allowable franking credits for the income year entered here is allowable as a tax offset and should be claimed in the Calculation statement at label C Non-refundable non-transferable and non-carry forward tax offsets.

For a Life insurance company (LIC) or organisation entitled to claim a refund of excess franking credits, the excess tax offset is claimed in the Calculation statement at label E Refundable tax offset and not at label C Non-refundable non-carry forward tax offsets.

In circumstances where the shares are not held at risk as required under the holding period and related payments rules, or there is other manipulation of the imputation system, the franking credit is not included in assessable income at label J and there is no entitlement to a franking tax offset.

See Trans-Tasman Imputation System Overview for further information.

Show at label C amounts of Australian franking credits from a New Zealand company that are included in assessable income because of a franked distribution paid to the company by a New Zealand company or because of its receipt indirectly through a partnership or trust. To work out whether the distribution is included in assessable income, refer to the ATO publication Foreign income return form guide (NAT 1840).

Use the Foreign income worksheet to record these transactions and to return calculated figures to the relevant labels in the main return.

Click label C to open the Foreign income worksheet (for).

If the shares or interests are not held at risk as required under the holding period and related payments rules, or there is other manipulation of the imputation system, do not include the Australian franking credit in assessable income at label C and there is no entitlement to a franking tax offset.

For most companies the amount of Australian franking credits included at label C is allowable as a tax offset and should be claimed in the Calculation statement at label C Non-refundable non-transferable and non-carry forward tax offsets. If the company is a life insurance company or organisation entitled to claim a refund of excess franking credits, claim the refundable amount in the Calculation statement at label E Refundable tax offsets.

A dividend from a New Zealand franking company may also carry New Zealand imputation credits. An Australian resident cannot claim any New Zealand imputation credits.

Subtraction labels

Show at this label any amounts claimed as a deduction during the current income year that are deductible under section 46FA of the ITAA 1936.

Click label C to open the Generic Schedule / Worksheet.

This deduction is allowable in certain cases for an on-payment of unfranked non-portfolio dividend by a resident company to its non-resident parent.

Where a deduction is claimed under section 46FA, the claiming entity is required under section 46FB of the ITAA 1936 to maintain an unfranked non-portfolio dividend account and complete item 8, label L-Balance of unfranked non-portfolio dividend account at year end.

Show at this label the deduction claimed for capital expenditure on buildings, which includes eligible capital expenditure on extensions, alterations or improvements. Exclude capital expenditure for mining infrastructure buildings and timber milling buildings.

Click label I to open the Capital works deductions worksheet (sbw). Integration from the Capital Works Deductions worksheet (sbw) is either directly to label I in the return or to a Rental Schedule you have prepared for this return.

If you choose to integrate to 'rent', a Rental schedule must already have been started for this return.

For more information on capital works deductions refer to Appendix 2 of the Company tax return instructions.

Commercial debt forgiveness provisions may affect the calculation of some deductions. Refer to Appendix 1 of the Company tax return instructions.

Only use this label if the company has been declared to be an offshore banking unit (OBU) by the Treasurer under subsection 128AE(2) of the ITAA 1936. Otherwise disregard this label.

Click label P to open the Generic Schedule / Worksheet .

If you complete P, you must complete an International dealings schedule. See International dealings schedule on the ATO website for further information.

Subject to certain exceptions, an OBU is effectively taxed at the rate of 10% on income derived from offshore banking (OB) activities. In calculating an OBU's total income for the year, gross income from OB activities is shown at label R Other gross income item 6.

Total expenses from OB activities are shown at label S All other expenses item 6.

To get the effective 10% tax rate on OB activity income, section 121EG of the ITAA 1936 reduces the assessable income and allowable deductions from OB activities so that an OBU’s taxable income includes only the ‘eligible fraction’ (currently 10/ applicable company tax rate) of its net income from OB activities.

For information on the taxation of an OBU refer to Taxation Determinations TD 93/202 to 93/217, TD93/241, TD 95/1 and 95/2 and to the current year ATO Company instructions.

Show at this label income related adjustments that have to be subtracted from label T Total profit or loss at item 6 to reconcile with label T Taxable Income or loss at item 7.

Do not include amounts already included at Item 7 labels C Section 46FA deductions for flow-on dividends to V Exempt income.

Generally the amounts that are included at label Q Other income not included in assessable income are income for accounting purposes but not assessable for income tax purposes.

Exempt income is shown separately at label V Exempt income item 7. For more information on specific items refer to the current year ATO Company instructions (worksheet 2).

Click label Q to open the Other Subtraction Items worksheet (sub). The total of the amounts entered into the fields at the top of the schedule under the heading Other Income not included in assessable income Label Q integrates to Label Q in the return.

Refer to International dealings schedule available on the ATO website.

Show at this label expense related adjustments that are subtracted from label T Total profit or loss at item 6 to reconcile with label T Taxable income or loss item 7.

Do not include amounts already included at item 7, labels C to P.

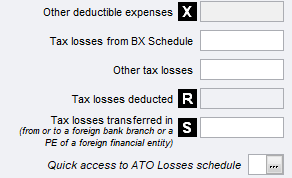

Generally label X Other deductible expenses shows amounts, including timing differences, that are an allowable deduction for income tax purposes but are not shown in the accounts or specifically shown at item 7, labels C to P.

Click label X to open the Other Subtraction Items worksheet (sub). The total of the amounts entered into the fields at the bottom of the schedule under the heading Other deductible expenses label X is passed to label X in the return.

For examples of specific items to be included and excluded. See Worksheet 2 of the current income year ATO Company instructions.

If the company is a life insurance company (LIC), include at label X Other deductible expenses the deduction it is entitled to if it receives a dividend from a LIC which includes a LIC capital gain amount. Refer to Item 16 - Life insurance companies and friendly societies only. Other companies are not entitled to this deduction.

On 1 March 2019, legislation was enacted that will supplement the current ‘same business test’ for company losses with a more flexible 'similar business test'. See:

- What's new - Increasing access to losses and

- LCR 2019/1 Business continuity test - carrying on a similar business

The new test will expand access to past year losses when businesses enter into new transactions or business activities.

In AE/AO you can't enter an amount directly at the label in the income tax return.

Separate fields are provided for companies and Head companies of a consolidated group.

If you've completed the Consolidated Groups Losses Schedule (bx), the amount we've passed that amount to this field.

Otherwise, to open the BX, press Alt+S.

Non-consolidated companies—Other Tax losses press Alt+S to open the Prior year losses worksheet (pyl) where you can manage your company prior year losses from year to year.

Show at this field only those tax losses of a prior income year that are deducted in respect of current income year under section 36-17 of the ITAA 1997. This includes any deductions for foreign losses converted to tax losses under Subdivision 770-A of the Income Tax (Transitional Provisions) Act 1997.

Subject to various rules, prior year tax losses are deducted in respect of a later income year or years in the order in which they were incurred-to the extent that they have not already been deducted

A quick access point to the Losses schedule (BP) is provided after label S. Selecting Y at the quick access to Tax Office Losses Schedule opens the:

- Consolidated Losses schedule (BX), or

- Losses schedule (BP)

depending on the selection you've made at item 3 label Z Consolidated group status. See ATO Losses schedule instructions on the ATO website for further information.

Show at label S the amount of tax losses transferred to the company from group companies under Subdivision 170-A of the ITAA 1997. See Tax losses deducted on the ATO website for further information.

A Generic Schedule / Worksheet is provided for dissection purposes.

Consolidated or MEC groups

Do not show tax losses transferred from subsidiary companies under Subdivision 707-A of the ITAA 1997. These losses should be shown in Part A items 1 or 2 of the Consolidated groups losses schedule.