This worksheet only applies to company tax returns.

Base rate entity (BRE) classification is new from 1 July 2018. See Treasury Laws Amendment (Enterprise Tax Plan Base Rate Entities) Act 2018 which received Royal Assent on 31 August 2018.

Under this Act, the definition of a base rate entity (BRE) replaces the carrying on a business requirement with a passive income test.

The company is a BRE if:

-

it has an aggregated turnover below $50 million and

-

no more than 80% of assessable income is base rate income (BRI) passive income.

An example of BRI passive income would be income such as interest, dividends or rent.

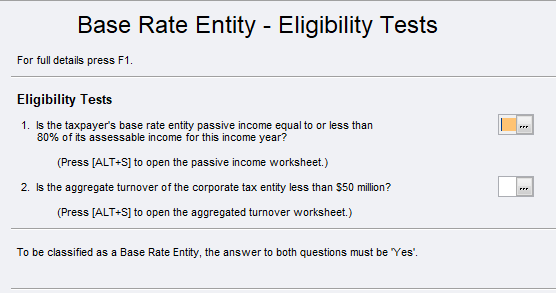

Is the company a base rate entity?

As different rates of tax apply to small business entities and base rate entities, we've provided 2 worksheets:

-

eligibility tests worksheet (bre)

-

passive income test worksheet (pit). Press Alt+S from the bre to access this worksheet.

Scroll to Item 3–Status of Company: label F2 and press Enter at the question Is the taxpayer a Base Rate Entity?

To complete the eligibility tests

If you answer No to either or both of these questions, close the worksheet and N will be passed to both the Small business entity question at label F1 and the Base rate entity question at F2.

If you press Alt+S to open the Passive income (PI) test worksheet, we'll default the answer based on the results of the PI test. Alternatively, if you have already calculated your PI and it's less than 80%, answer Y to question 1.

If you press Alt+S at question 2, you can complete the Aggregated turnover (AT) worksheet. We'll default the answer based on the results of the AT test. Alternatively, if you have already calculated your AT and it's less than $50 million, answer Y to question 2.

Answer Y to both eligibility questions to qualify for the lower 27.5% tax rate.

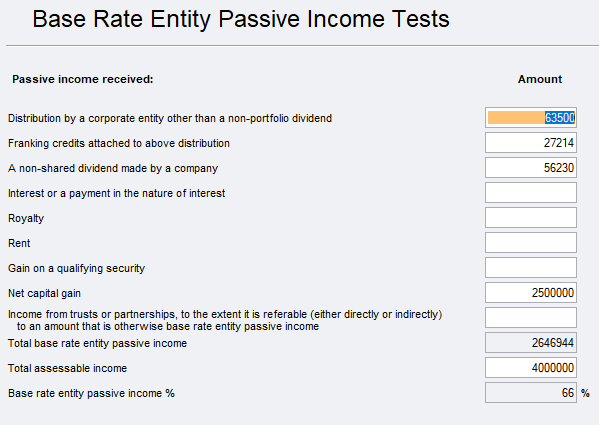

To complete the passive income test

Press Alt+S at question 1 to open the Base Rate Entity Passive Income Tests worksheet.

Enter amounts against the relevant income type. The Base rate entity passive income % is auto-calculated.

BRE passive income % is calculated by dividing Total base rate entity passive income by Total assessable income

If the answer is 80% or less, the company passes the first eligibility test.

Press F6 to close the worksheet. You've passed the first test.

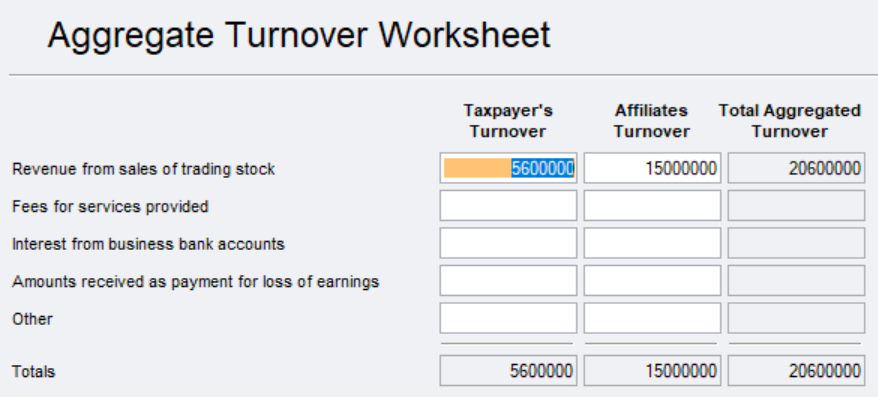

To complete and calculate the aggregated turnover

Press Alt+S at question 2 to enter details and complete the second eligibility test.

When the aggregate turnover is less than $50 million, you've passed the second test. Press F6 to close the worksheet.

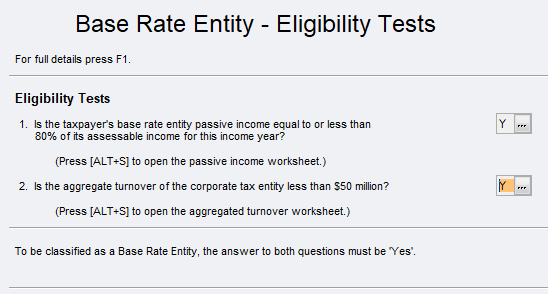

Both questions are now Y.

Press F6 and we'll pass a Y to the front cover Item 3: Status–label F2 Base rate entity.

With both eligibility tests passed, we'll calculate income tax in the Calculation Statement: Label T1 at the 27.5% BRE company tax rate.

Even though you may not be eligible for the reduced tax rate, you may still be eligible for other small business tax concessions. For example, accelerated depreciation and/or small business capital gains exemptions if you are a small business. To be eligible for these concessions, you must complete the small business eligibility tests worksheet sbe at item 3: Label F1.