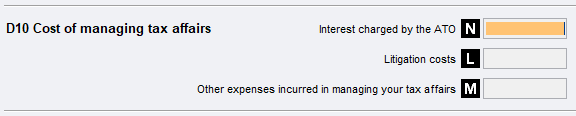

From 1 July 2018, you need to separate your client's expense claim into 3 components at label D10.

Label N: Interest charged by the ATO includes:

-

General interest charge (GIC)

-

Shortfall interest charge (SIC)

-

Late payment interest (LPI).

Label L: Litigation costs include:

-

Court and administrative appeals tribunal fees,

-

Solicitor, barrister and other legal costs incurred in managing your tax affairs.

Label M: Other expenses incurred in managing your tax affairs include:

-

tax agent fees for preparing and lodging your tax return and activity statements

-

travel to get tax advice from a recognised tax adviser

-

obtaining a valuation needed for a deductible donation of property.

-

Fees paid to a recognised tax adviser are deductible in the year they are incurred.

-

You can't claim for the cost of tax advice given by a person who isn't a recognised tax adviser.

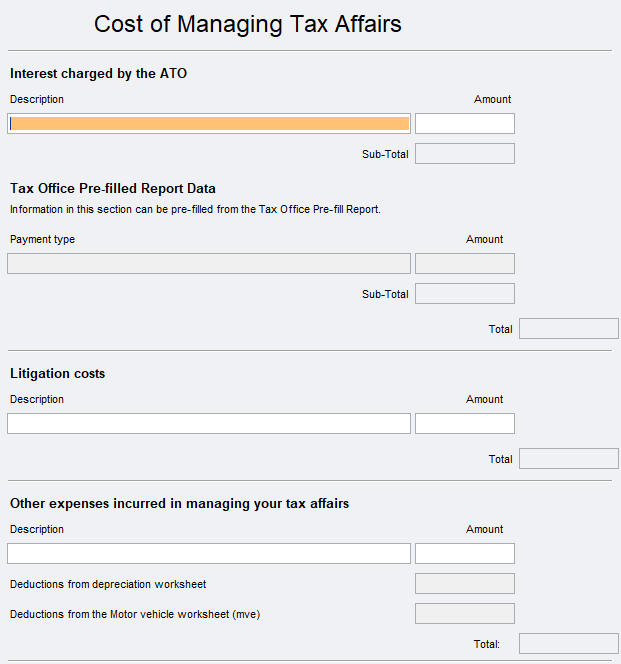

To complete the D10 worksheet

Each section comprises a repeatable data entry row.

To add rows, press Ctrl+Insert. To delete rows, press Ctrl+Delete.

For ATO interest charged at label N, pre-fill from the ATO Pre-fill report is available. See Pre-fill manager for further information.

If you've completed the Motor vehicle worksheet (mve) or the Depreciation worksheet (d), then any relevant amounts are pre-filled for Costs of managing tax affairs—label M.

Totals will be filtered through to the relevant label when you close the worksheet.