Before completing the worksheet and claiming the ESIC tax offset, it's important to read Early stage investor tax offset on the ATO website.

The Fund in this example has already completed the claim for the Early stage venture capital limited partnership tax offset.

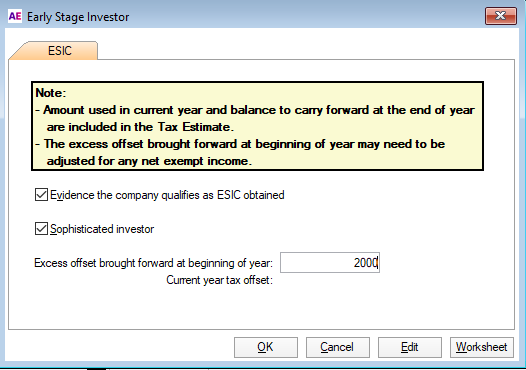

You'll find this worksheet in the Calculation statement at D3.

To complete the worksheet

-

Click in Goto (F2) and enter D3 and click the label to open the worksheet.

The Evidence the company qualifies as ESIC obtained question is mandatory. Click the Sophisticated investor checkbox if investor has passed the sophisticated investor test for at least one of the acquisitions. Enter any Excess offset brought forward from the previous year, adjusting the excess to take account of any net exempt income under Div 65 of the ITAA 1997.

It isn't necessary for the Fund to have passed the Sophisticated investor test if the ESIC tax offset was the result of a share of distribution from a partnership or trust.

-

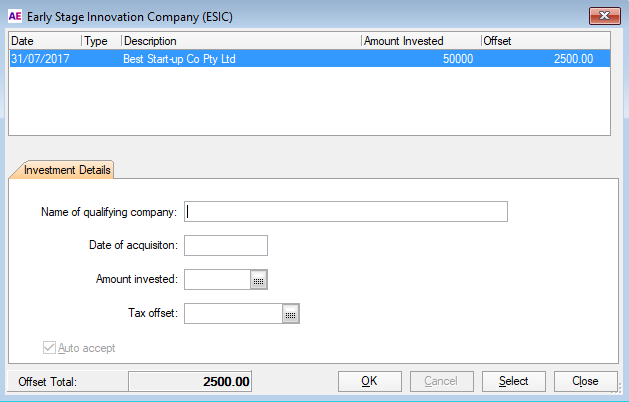

Click the Worksheet button and enter the required details. Calculate and enter the offset expected.

-

Press F6, click OK or the Save icon to accept the transaction and see it move into the stored area at the top of the worksheet, leaving the fields open for any further entries.

If there are no further transactions, click Close to return to the front entry screen.

-

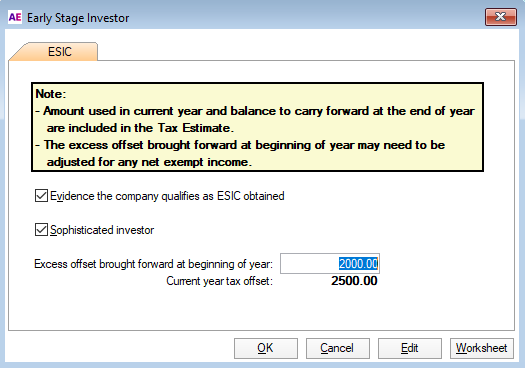

Press F6, click OK or the Save icon to exit the front entry screen. We'll filter the totals through to labels D3 and D4.

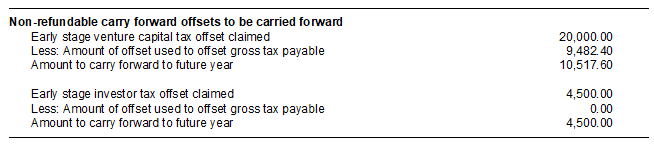

As there is also an offset claimed for the Early stage venture capital scheme, the sum of the two is pre-filled at label D - Non-refundable carry forward tax offsets.

F4 Estimate

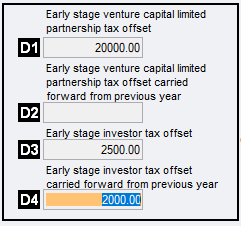

These offsets are detailed separately in the F4 estimate and limited to Tax payable after the application of Non-refundable tax offsets. Any excess can be carried forward to the following year.

The excess, if any, shown in the estimate at the foot of the estimate, has not been adjusted for Div 65 of the ITAA 1997 for the effects of any net exempt income (foreign and Australian) where applicable.

The ESIC offset is not included in the calculation of GDP-Adjusted income for PAYG income tax instalments purposes.

CCH References

20-700 Outline of innovation incentives