-

That part of the net income of the trust that has not been assessed to either a presently entitled beneficiary or the trustee on behalf of a presently entitled beneficiary; see Is a beneficiary presently entitled to a share of the income of the trust estate?

-

shares of the net income of a trust on behalf of individual or company beneficiaries not in their capacity as trustee of a trust estate who are presently entitled to a share of the income of the trust estate but are non-resident at the end of the income year; refer to Item 29 - Overseas transactions (Trust Returns) for additional information

-

shares of the net income of a trust on behalf of beneficiaries who are presently entitled to a share of the income of the trust estate but are under a legal disability

-

If the trust is a Special Disability trust and the 'principal beneficiary' is an Australian resident at the end of the income year, the 'principal beneficiary 'is treated as being under a legal disability

The rate of tax payable by the trustee will depend on the type of trust and the beneficiary's individual circumstances.

If the beneficiary is presently entitled to a share of the income of the trust estate, not under a legal disability, and is a resident at the end of the income year, then the beneficiary, not the trustee, is taxed on that same percentage share of the net income of the trust.

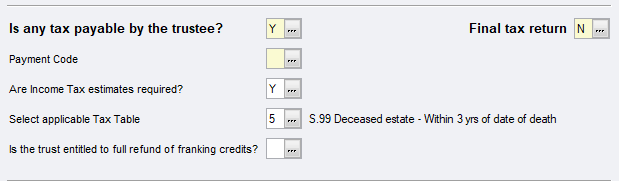

If the trustee is liable to pay any tax, print X in the Yes box at this item even if payments have been made in advance. Otherwise print X in the No box. The beneficiary or trustee pays tax on the net income of the trust. Net income means the total assessable income calculated as if the trustee was a resident taxpayer, less all allowable deductions, except deductions for net farm management deposits. In the case of any beneficiary with no beneficial interest in the trust corpus, past losses are required to be met out of corpus.