Working Holiday Makers

-

Read the on-screen text and select Yes at the 416 or 462 working holiday visa question. We'll calculate tax at 15% on WHM income up to $37,000 earned during the current income year.

-

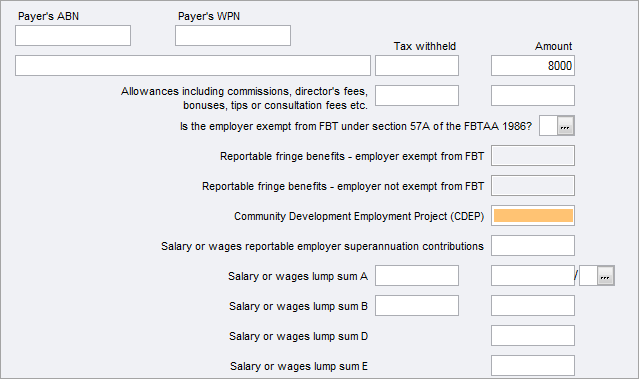

Enter the Payer's ABN, WPN, Tax withheld and Amount.

-

We'll populate Item 1 with the details and type H.

-

Go to Item A4 in the Adj/Credits tab and select Label D - Working holiday maker net income. The working holiday maker net income worksheet opens

-

Income from Item 1 is populated in the working holiday maker net income worksheet.

Reportable Fringe Benefits and Reportable Superannuation contributions

In MYOB Tax, you will also enter Reportable Fringe Benefits and Reportable Superannuation contributions that are notified on the PAYG Payment Summary. These amounts are passed to the Income Test Items IT1 and IT2 respectively.

From 1 July 2017, Reportable fringe benefits are reported separately in accordance with their exemption status under section 57A of the FBTAA 1986. Enter this amount at the correct field as defined on the Payment Summary.

If you received any reportable fringe benefits amounts of $3,773 or more, enter those amounts at the relevant field in the Reportable fringe benefits box. Do not enter amounts that are less than $3,773 as this will affect the calculation of the Adjusted taxable income (ATI) that is used for defining eligibility for some offsets, for example, dependency offsets and SAPTO.