Label K - Low value pool deduction

From 1 July 2018 where you have work-related expenses of this nature, the ATO requires you to lodge a Deductions schedule (DDCTNS).

The item at label K is no longer open to edit and you must click label K to open the Depreciation worksheet (d).

Low-value assets are depreciating assets that are not low-cost assets but which, at the beginning of the income year, had an opening adjustable value of less than $1,000 under the diminishing value method.

Only include at this item a deduction for Low-Value Pool items that were used in your work as an employee (work-related deductions items D1 to D5), or in earning rental income (Item 21).

Low cost and low value assets used in conducting a business to generate assessable income and added to a Low Value Pool must be claimed at Item P8.

You can only have one low-value pool and once you choose to allocate a low-cost asset to the low-value pool, all low-cost assets the taxpayer starts to hold in any subsequent income year must also be allocated to the pool.

When you close the Depreciation worksheet (d) we'll pass the amount to:

Item D6: label K

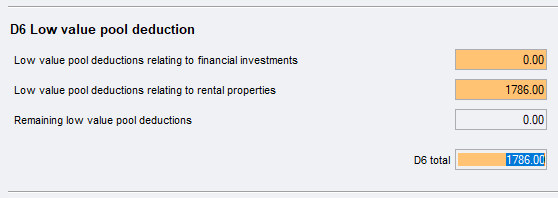

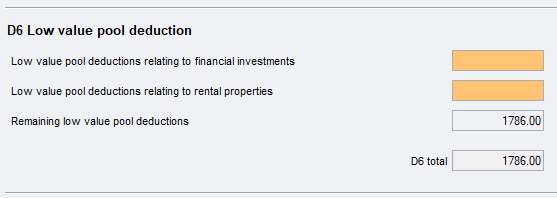

Deductions schedule D6

You must now dissect the amount at D6 in the Deductions schedule into the amount related to financial investments and/or the amount relating to rental properties you might own.

To do this,

Click Deductions Schedule in the Navigation pane, ATO Schedules.

Scroll down to D6 Low value pool deduction and do the dissection. As you key an amount the figure in the Remaining low value pool deductions field is reduced. This field must be zero for a valid PLS lodgment.