Not available in Accountants Office

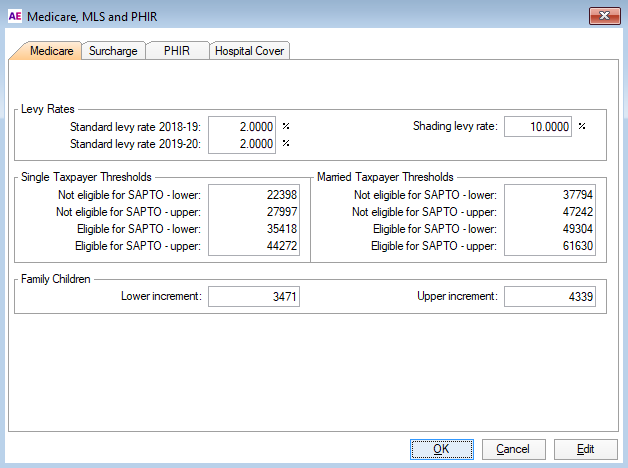

The Medicare levy table holds the income thresholds and shading-out ranges for single and married taxpayers and Australian Government Pension recipients for the Medicare levy and the Medicare levy surcharge.

Medicare levy rates and thresholds

All resident Australian taxpayers whose taxable income rises above the lower threshold must pay a Medicare levy of 2% of their taxable income.

Lower income levy threshold:

This is the standard Medicare levy payable by all taxpayers who are residents of Australia.

Upper income levy threshold:

This is the shading-out rate that applies to taxpayers who have income in excess of the threshold.

Additional child increment:

This is the amount by which the Medicare income threshold increases for each dependent child after the first.

If there are more than 6 dependent children or students, for each additional dependent child or student the lower limit increases by the lower increment and the upper limit increases by the upper increment.

For the Medicare levy exemption (but not the reduction), dependant means an Australian resident you maintained who was:

-

your spouse, or

-

your child under 21 years old, or

-

your child, 21 to 24 years old, who was receiving full-time education at a school, college or university and whose adjusted taxable income for the period you maintained the child was less than the total of $282 plus $28.92 for each week you maintained them.

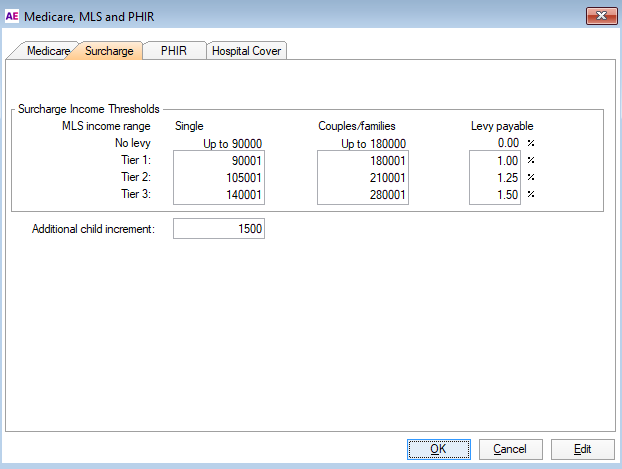

Medicare levy surcharge rates and thresholds

The Medicare levy surcharge is based on a three-tier system with the maximum rate for those without sufficient private health cover being 1.5% based on their Adjusted taxable income or Combined adjusted taxable income for these purposes.

Income range Single and Couples/families:

Lower limit:

This is the threshold of notional taxable income below which a taxpayer is exempt from the Medicare surcharge levy.

Upper limit:

If a taxpayer's notional taxable income falls within the lower limit (defined in the previous field) and the upper limit, the levy is shaded-in at the rate defined in the Shading Levy rate field for the excess amount over the lower limit.

Levy payable rate:

Where MLS applies when your notional income rises above the Tier 1 threshold of 1%, an additional surcharge applies to all Resident Australian taxpayers without adequate private health cover insurance.

Single:

Single taxpayers without adequate hospital cover insurance whose income rises above the lower threshold will pay a 1% MLS on their taxable income.

Couples/Family:

Families without adequate private patient hospital insurance are liable to an additional levy surcharge. This is the level of notional income above which the combined taxable income for a family with no dependent children incurs the additional Medicare levy rate.

Levy payable:

Where MLS applies when your income rises above the Tier 1 threshold of 1%, an additional surcharge applies to all Resident Australian taxpayers without adequate private health cover insurance.

Additional child increment:

This is the amount by which the surcharge income threshold is increased for each dependent child after the first.

If there are more than 6 dependent children or students, for each additional dependent child or student the lower limit increases by the lower increment and the upper limit increases by the upper increment.

For MLS purposes, your dependants (regardless of their income) are your:

-

spouse, even if they worked during 2018–19 or had their own income

-

children under 21 years old

-

children 21 to 24 years old who are studying full time at school, college or university.

Dependants must have been Australian residents and you must have contributed to their maintenance.

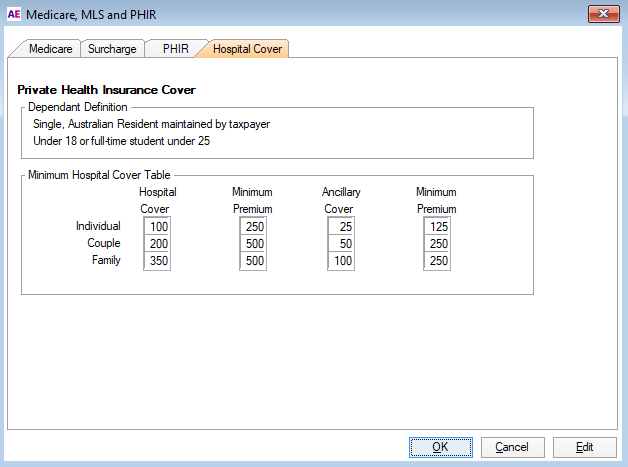

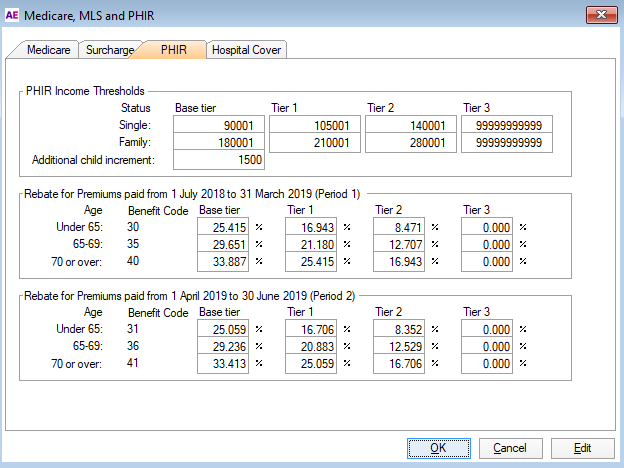

Private health insurance rates and thresholds

This table holds income the rates and thresholds as well as the rebates rates for premiums paid for the current year periods:

1 July to 31 31 March, and

indexed rates from 1 April to 30 June .

Single and Family Income Ceilings - these are the same as for the Medicare levy surcharge. Income refers to Adjusted income for Medicare levy surcharge purposes.

Hospital Cover minimum Premiums payable table.