This worksheet passes values to various items in the Individual, Trust and Partnership returns. It can be used for all other income tax returns, but there is no integration to those other returns.

From 1 July 2015, the ⅓ actual expenses method and the 12% original cost method were repealed, leaving the two methods:

-

cents per kilometre

-

logbook method.

-

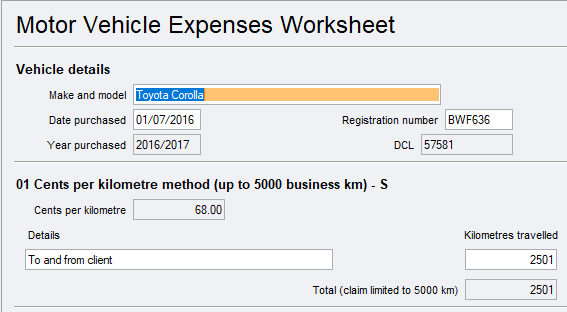

The rate for the current income year is 68 cents per kilometre. This rate is used for all motor cars, except:

-

motorcycles

-

vehicles with a carrying capacity of one tonne or more (such as a utility truck or panel van) or 9 passengers or more (such as a minivan).

-

-

The Commissioner of Taxation reviews the rate each year based on the average operating costs of a motor car.

-

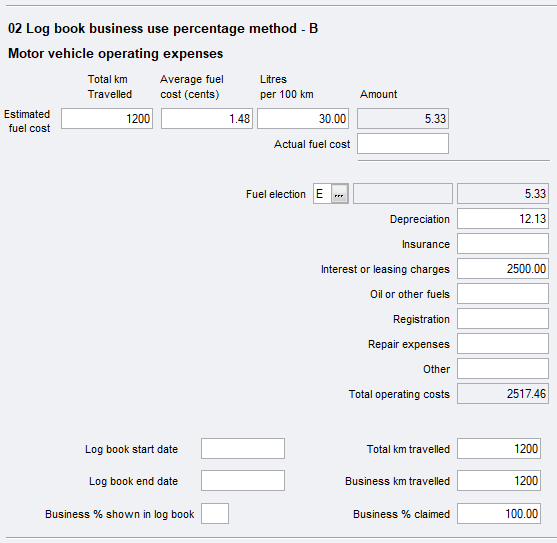

There is no change to the logbook method. The taxpayer must keep a logbook and the percentage of business use as the claim is based on the business use percentage of the expenses for the car. See this link for information on the logbook method.

-

The details of all motor vehicles roll over each year.

-

If you have more than 10 motor vehicles, MYOB Tax will consolidate the records in the Deductions schedule (DDCTNS). Motor vehicles using the cents per kilometre (Km) method integrate to the Deductions schedule first, in descending Km order, followed by the logbook method. This will assist with the consolidating record not breaching the 5,000 Km limit.

-

You can now enter amounts in dollars ($) and cents.

To complete vehicle details and cents per km method

Enter the details as required.

Some of these are needed for a valid ATO Deductions schedule (DDCTNS). They are also used when preparing the Motor Vehicle Substantiation Declaration for your client's signature.

ATO requirements for consolidation where you have more than 10 motor vehicles have meant changes, for example; the Logbook method:

-

Gross depreciation and Gross amount excluding depreciation aren't reduced by the Business %., and

-

Business kilometres travelled field contents are not lodged with the ATO

-

D1's total includes the business Km and log books methods amounts multiplied by the business %. This is not shown in the schedule

-

Repairs and maintenance is now known as Repair expenses totals in this form don't lodge to the ATO. We use them to cross reference amounts in the individual income tax return

-

The ATO may require you to substantiate how you calculated the Kms for the cents per Km method.

To complete the logbook method (business use %)

Do not include capital costs such as the purchase of the car or improvements to it.

-

A logbook, odometer records and written evidence for all car expenses except fuel and oil costs must be kept.

-

The logbook is valid for five years.

-

If this is the first year you are using this method, you must have kept a logbook during the current income year.

-

The logbook must cover at least 12 continuous weeks.

-

If you started to use your car for business purposes less than 12 weeks before the end of the current income year, you can continue to keep a logbook into the next income year so that your logbook covers the required 12 weeks.

-

If you want to use the logbook method for two or more cars, the logbook for each car must cover the same period.

-

If you have not kept a logbook for the 5 income years prior to the current, you must have kept a new one for the current income year.

-

If you did not keep a new logbook for the current income year, you cannot use the logbook method.

-

If your car use changed, make a reasonable estimate of what your business use percentage would have been for the whole of the current income year, taking into account your:

-

logbook, odometer and other records

-

any variations in the pattern of use of your car

-

any changes in the course of earning your income

-

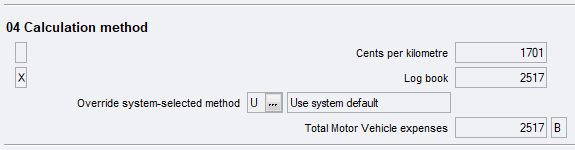

To choose the optimal method - per km or logbook

If you enter details for both the cents per Km and the log book methods, we'll automatically default the method with the largest claim amount.

You can change the default using the drop down list at the Override system-selected method.

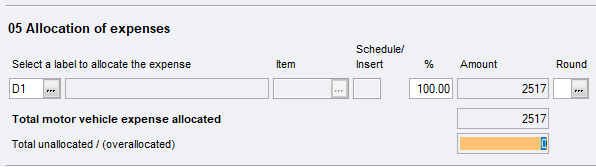

To allocate expenses to other items or worksheets

By default, the motor vehicle expenses deduction of 100% defaults to item D1 and from D1 to D10 in schedule W.

Where the mve expense is to be apportioned across more than one worksheet or item in the return, press Ctrl+Insert to open up another set of allocation fields.

Click F10 at the ellipsis and select an item to share to.

As the ATO abolished the BJ interest and dividends schedule, we removed these worksheets:

-

idd Interest deductions

-

ddd Dividend deductions.

We also removed schedule W as there's no integration from the mve to the ATO's schedule W.

|

Code |

Individual return integration points |

|---|---|

|

D1 |

Work-related car expenses (item D1) |

|

D2 |

Work-related travel expenses (item D2) |

|

D5 |

Other work-related expenses (item D5) |

|

D7 |

Interest deductions (item D7) |

|

D8 |

Dividend deductions (item D8) |

|

D10 |

Cost of managing tax affairs (item D10) |

|

b |

Business income worksheet (item P8) |

|

c |

Primary production income worksheet (item P8) |

|

dip |

Partnership distributions (item 13) |

|

dit |

Trust distributions (item 13) |

|

ref |

Foreign rental schedule (item 20) |

|

ren |

Rental income (item 21) |

|

sed |

Work-related self-education expenses (item D4) |

Rounding error

If the allocation of mve expenses results in an over-allocation of the expenses due to a rounding error, we've provided a rounding function for the adjustment.

The options available are:

-

Natural rounding: Expense amounts of 50 cents or more are rounded up and included in the allocated expense. Expense amounts of 49 cents or lower are rounded down with the odd dollar (if any) included in the Total unallocated / over-allocated expense.

-

D: Round down, the odd dollar is included in the Total unallocated / over-allocated expense.

-

U: Round up, the odd dollar is added to the expense for the label selected.

For trusts and partnerships the items for sharing mve expenses with are:

|

Code |

Partnership and trust return integration points |

|---|---|

|

18 |

Other Deductions (item 18) |

|

b |

NPP Income and expenses (Schedule B) |

|

c |

PP Income and expenses (Schedule C) |

|

dai |

Deductions relating to Australian investment income (dai) |

|

rep |

Rental Schedule (rep) |