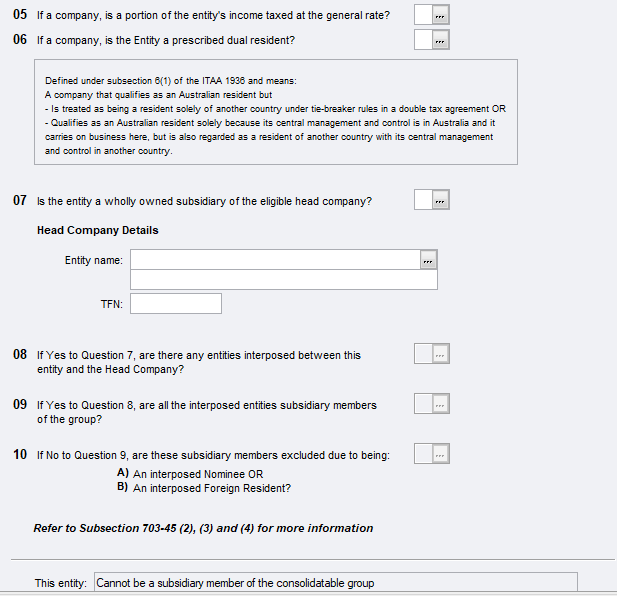

For an entity to be a subsidiary member of a consolidated group, the entity must:

-

be a company, partnership or trust

-

be a wholly-owned subsidiary

-

be an Australian resident

-

if it's a company, have some of its income taxed at the general company tax rate

-

not be an excluded entity, see Entity Classes for Tax Consolidation 2024.

Example of the Consolidation eligibility (subsidiary) worksheet (ces)

The questions are self-explanatory. See Business consolidation eligibility.

Depending on the answers you've provided, we'll calculate the subsidiary entity's eligibility and display the answer at the bottom of the worksheet.

%20first%204%20questions.PNG?cb=10d11ffe8c364b06ed10a976af6e34ff)