Before claiming the ESVCLP tax offset, it's important to read the ATO's information Tax incentives for innovation.

Taxpayer receives share of ESVCLP tax offset example

The taxpayer has already claimed an Early Stage Investment Company ESIC tax offset.

-

Once you have recorded the share of ESVCLP tax offset received in the Distributions from partnerships (dip) or the distributions from trusts (dit) worksheets have been completed at item 13: Partnerships and trusts—label O or U, you will see the effects of this in the ESVCLP worksheet (esv) at item T8.

-

Goto (F2) item T8 and click label K to open the front entry screen. Enter any excess ESVCLP brought forward from a previous year, adjusted for Div 65 of the ITAA 1997 to take account of any Net exempt income (foreign or Australian). Then click the Worksheet button.

-

The offset amount is automatically created in the esv worksheet. You can recognise it by the entry Type D.

.png?cb=ffc81736c0232396e6cde32b29848594)

-

If you have also invested in an ESVCLP company, enter those details in the acquisition details fields provided. You can have more than one acquisition but you must create a separate entry for each as there are capital gains implications on disposal.

-

Save each entry. When finished, click Close, and then click OK or press F6 and we'll filter the Offset total through to item T8: label K.

-

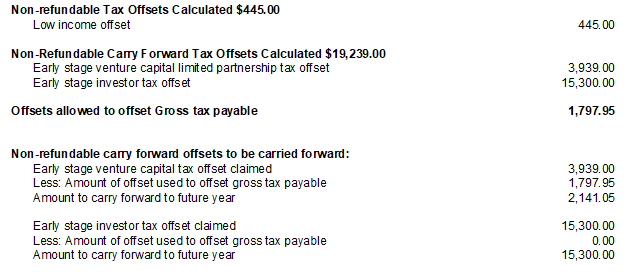

The F4 estimate includes a summary of how the offsets were applied and any excess to carry forward at the end of the year

The ESVCLP tax offset is not taken into account when calculating the GDP-Adjusted income for PAYG income tax instalments purposes.

CCH References

20-700 Outline of innovation incentives