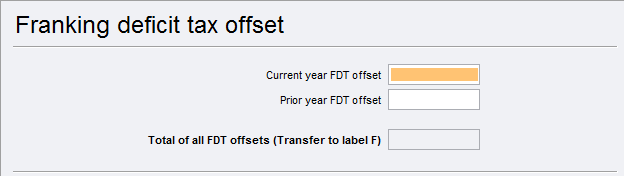

The tax offsets shown at label F are not refundable; they are only offset against gross tax to reduce it to zero, if there is any gross tax to be paid after labels C, D and E have been applied to gross tax. Any excess of FDT offset can be carried forward to the next income year.

Tax offsets to be shown at F include those as shown below:

Where the company has a franking deficit tax (FDT) liability, it can claim an FDT offset against its income tax liability.

Some special rules apply to life insurance companies to ensure that an FDT liability can only be offset against that part of the company's income tax liability that is attributable to shareholders. The amount of FDT liability that can be claimed as a tax offset is reduced in certain circumstances. Refer to the Franking account tax return and instructions (NAT 1382) for more information on how to calculate this amount.

There are also special rules that apply to late balancing entities that elect to determine their FDT on a 30 June basis. Refer to the Simplified imputation: franking deficit tax offset and Simplified imputation: FDT offset for late balancers for information from the ATO website.