Complete the rental schedule (BR) if the partnership owns property that it rents out.

You must:

-

lodge a Rental schedule (BR) when the partnership earns rental income or loss.

-

distribute any net rental income or loss to the partners.

You can't distribute all the income or loss to one partner.

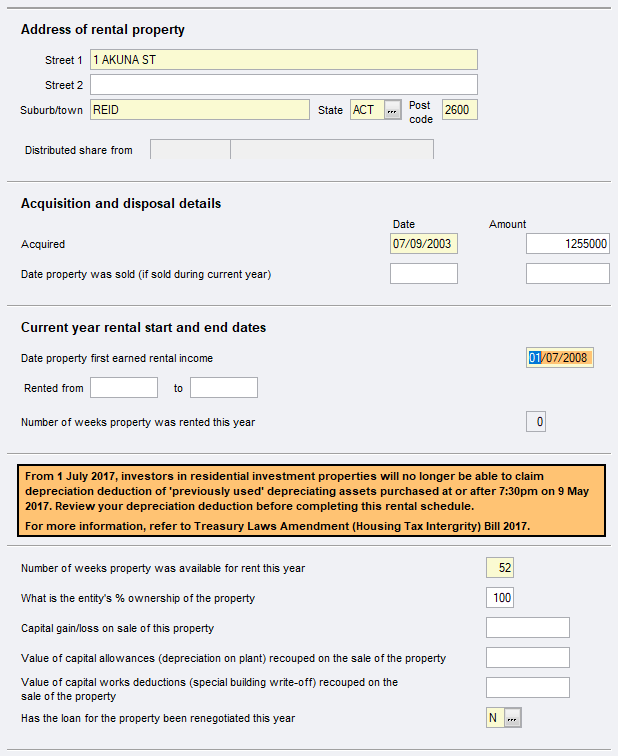

Property details example

We colour mandatory fields yellow. You must complete them.

If the property wasn't rented at all, leave the Rented from–to field blank.

If you don't enter the Rented from–to dates:

-

a zero is pre-filled at the Number of weeks property was rented this year field, and

-

52 weeks defaults to the Number of weeks property was available for rent this year.

Entering from–to dates triggers auto-calculation of the number of weeks.

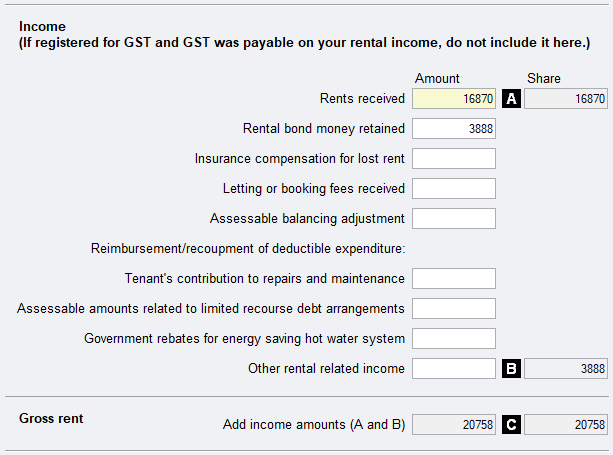

Income example

We've provided some non-ATO supplementary income fields. Entered amounts are totalled and shown at label B: Other rental related income.

These supplementary fields are for record keeping purposes only and aren't transmitted to the ATO.

Press Alt+S to open dissection grids.

Expenses example

If the partners used the property for a private purpose during the year:

–enter a default private use percentage (PU %) and we'll apply to all expenses expenses.

If private use applies to individual expenses only

–leave the PU % field empty. Then enter the PU % against those particular expenses.

Press Alt+S to open dissection grids.

Some grids have a link to other worksheets. For example:

-

depreciation deductions from the depreciation worksheet (d)

-

capital building allowance deduction from the sbw worksheet, and

-

motor vehicle expenses from the mve worksheet.

Column behaviour

|

Gross amount |

Is the total amount expended by the partnership for that expense. |

|

Share |

Where the field is greyed-out, the Share is auto-calculated when when you press the Share button. Note that the share for the Partnership is always 100%. The net income or loss must be distributed to the Partners in their respective share in the partnership at item 51: Statement of distribution. |

|

Pte use % |

If you've defaulted a PU %, we close this column of fields to edit. Otherwise, enter the PU % for the relevant expense. |

|

Priv amount |

Is calculated automatically if you've entered a PU%. |

|

Net amount |

Is the sum of the: Share less PU % |

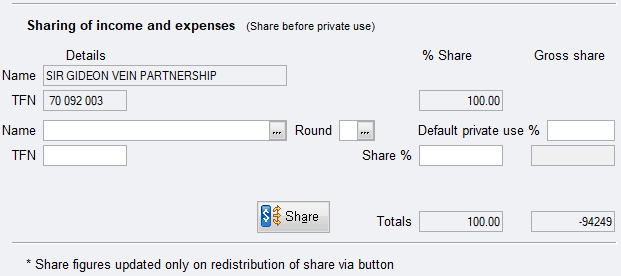

Sharing of income and expenses

Don't share income to the partners here. Do that in the Statement of Distribution at item 51.

For partnerships, the share % in this worksheet is set at 100%.

Clicking the Share button completes the expenses share column. Closing the schedule filters the totals through to the item 9: labels F, G, X and H.

The statement of distribution

The rental income or loss must be fully distributed to the partners in accordance with their share in the partnership.

If all the partners’ returns are handled by the practice, then the distribution will be to each of their individual returns in your tax database.

If you don't act for all the partners, distribution will still occur and a distribution statement prepared for that partner. You can print the distribution statement to pass on another tax agent..

The ATO cross-matches the partners’ returns to the partnership return income or loss. This means that you should lodge the partner's returns at the same time as the partnership return.