Example - Solely Earned and Jointly Earned Investment Income

In the following example, the taxpayer, Sally, has taxable income of $14,331 included in which is salary and wages of $10,000 and work-related deductions of $299. Whilst these amounts are used in the calculation of the income test for Co-contributions purposes, they do not form part of the A3 labels.

Sally's has also earned some interest on her own account of $50 and a share of dividends with her partner, David, her share being a total of $4,000 with her share of the expenses being $6,500. Sally and her sister Cher have a jointly owned rental property and Sally's share of the rental income is $15,000 and her share of the expenses $10,000. Sally has also had a Distribution from a Managed Investment Trust of $2,345 which is solely earned income and an expense against that income of $265.

Open the worksheet scc by pointing at the A3 label and left clicking with the mouse, or select the worksheet from Preparation > Schedule > Super Co-contributions.

To open Part A which relates to Solely earned investment income and Solely earned Business income and deductions, click label A or press [Enter] at any one of the greyed-out fields.

Using the income described above, you will dissect Sally's A3 labels income and deductions as follows:

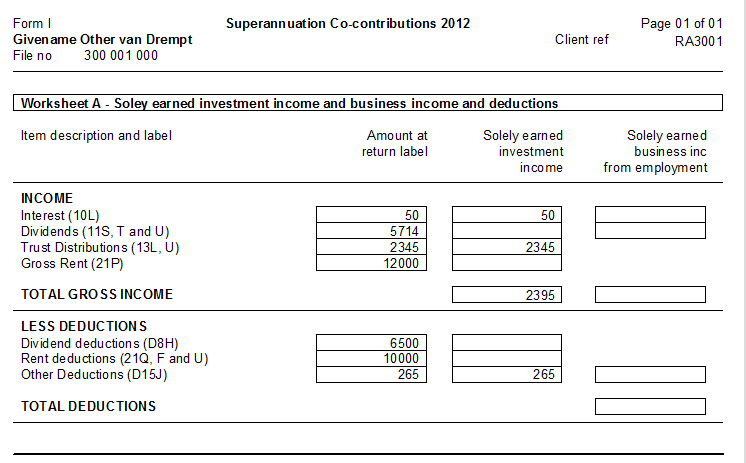

Solely earned Investment income and expenses

Interest item 10 label L | 50 |

Distribution from MIF item 13 label U | 2345 |

Expenses relating to MIF D15 label J | 265 |

For these purposes the deductions are ignored. The result for Solely earned investment income is therefore (50 + 2,345) = 2,395

Jointly earned investment income - Group 1 - Sally and David

Dividends item 11 label T | 2800 |

Franking credit item 11 label U | 1200 |

Deductions at D8 related to dividends | 6500 |

The Group 1 dividends income less deductions results in a loss, therefore the transactions are ignored for the purposes of calculating the value to integrate to the main return label.

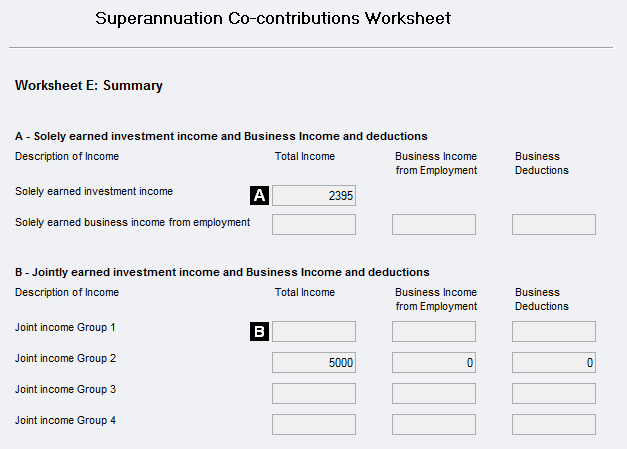

Jointly earned investment income - Group 2 - Sally and Cherie

Rental income item 21 label P | 15000 |

Rental Deductions 21 label U | 10000 |

The result of the Group 2 Rental property is income of $5,000 and this income is included in the value that integrates to the main return.

The Summary shows the sum of $7,395 at label F and this is made up of the solely earned Trust distribution of $2,395 and the gain from the jointly owned rental property of $5,000. As previously mentioned, the loss on the dividend income does not count for these purposes.

The following is the Printed report which shows that only those items that have values at income or expense labels are printed.

Integration from the Summary to the return:

The following screen shot is of the Solely earned income amounts that have been entered.

The jointly earned income worksheet provides for a maximum of 4 different groups, to open a group, enter a name in the Group Name field.

Now dissect the amounts that relate to jointly earned investment income and deductions:

As can be seen from the following screen shot of the Section E, the Summary, the jointly owned dividends resulted in a loss and therefore does not count and zeroes are returned.

.png?inst-v=94fe6bfd-7618-4a9a-8cc5-ffe2e53a2f49)

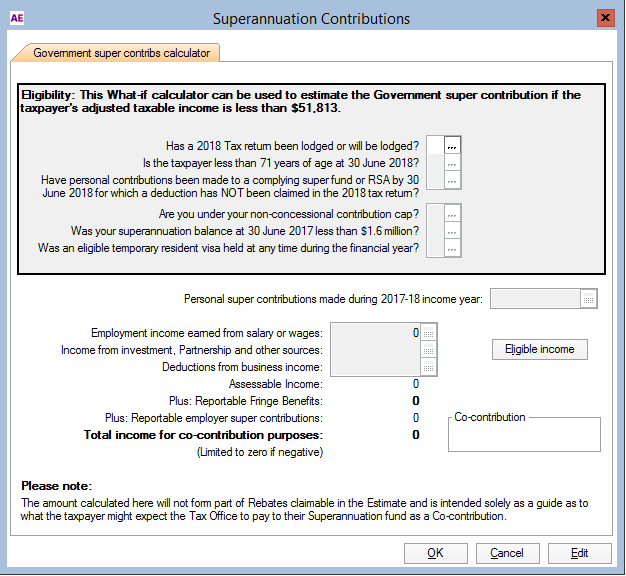

The Co-Contributions What-if Calculator

When you open the Co-Contributions What-if Calculator, you see the effects of all the entries from the income tax return that are considered as income for these purposes.

The amounts that have been integrated to the labels in the return are now reflected in the What-if Co-Contribution calculator which provides an estimate of what the taxpayer may expect by way of a Government co-contribution based on information that is in the return. This is not to say that the ATO may not adjust some balances depending on information provided from other sources.