There are two questions at item 19 which are mandatory. For convenience, the answer is defaulted to No. Consider whether you need to change either to Yes.

Temporary residents do not need to show foreign investment income at this item.

Label B - Transfer of trust income

If the answer to the label W question is YES, an amount must be entered and you must complete an Other attachments schedule (att) and lodge it via PLS or, if lodging on paper, with the return. Include the taxpayer's name, address, TFN, the name of the non-resident trust and its trustee or trustees, and the amount of any attributable income in relation to the trust.

The transferor trust measures may apply if, at any time you directly or indirectly transferred or caused the transfer of property, including money, or services to a non-resident trust.

A trust is a non-resident trust if no trustee of the trust estate was an Australian resident and, trust estate’s central management and control was not in Australia at any time during the income year. Refer to the Foreign Income return guide available on the ATO website.

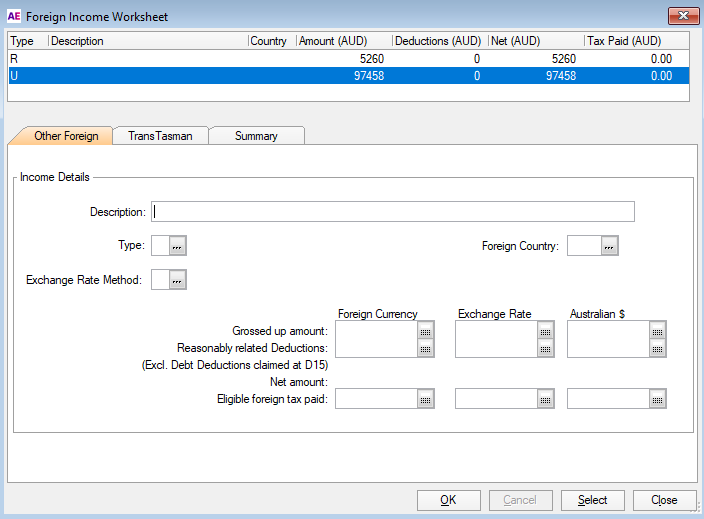

For the correct calculation of any foreign income tax offset (FITO), the amounts you enter at labels K or B are passed to the Foreign income worksheet (for). See Foreign income worksheet (for).

You must then:

-

go to item 20: Foreign source income and foreign assets or property and click label M to open the for worksheet.

-

Click the Worksheet button and check that the figures transferred are correct, then

-

Click Close and F6 to exit and save the for worksheet.