This worksheet has been redesigned to meet the requirements for preparing and lodging the ATO's Deductions schedule (DDCTNS). It assists also with the application of the deductible amount under S82AA.

The Work-related self-education Expenses worksheet (sed) 2018 2018 has been redesigned to comply with ATO changes.

-

You can only claim self-education expenses that related to your work as an employee at the time you were studying

-

The deduction cannot be claimed if the self-education was undertaken in order to get a new job or commence a new income earning activity

-

If you've received a PAYG payment summary foreign employment, or you are a Working holiday maker you can claim any expenses related to a course you undertook here

-

You can have up to 20 sets of details. To add a row, press Ctrl+Insert. To delete a row, press Ctrl+Delete

-

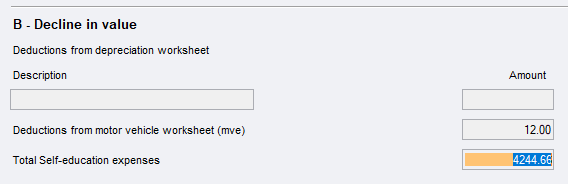

Motor vehicle expenses and Depreciation expenses relating to D4 are passed from the Motor vehicle worksheet (mve) and the Depreciation worksheet (d)

-

So that the expenses are reduced by the s82A reduction amount of $250, you must enter your expenses under the right category. These are in worksheet order A, D, C E and B

-

If you enter expenses in $c you'll need to ensure that they end in a whole $ figure to avoid V172D.

-

Totals in this form are not lodged with the ATO. They are used to to cross reference amounts in the individual income tax return.

If you have more than 10 motor vehicle worksheets (mve), any using the cents per Kilometre method are passed to the DDCTNS first in descending order (highest Km. number to lowest number), followed by the log book method. This is to meet the ATO's requirements for consolidation which are to see that 5,000 Km limit isn't breached.

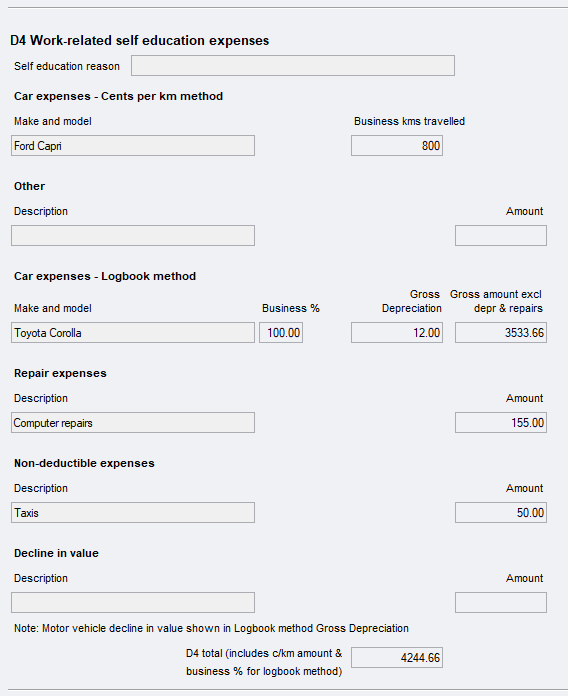

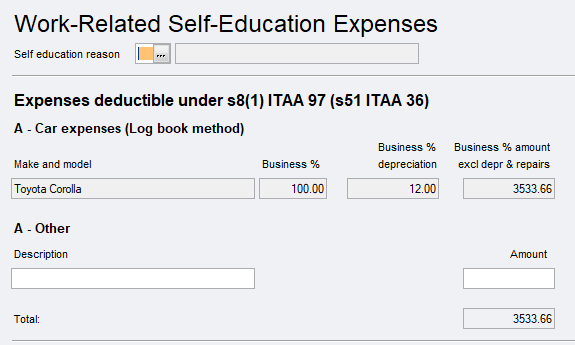

To complete item A - Car expenses Log book method

Complete the motor vehicle worksheet (mve) and select to apportion the costs to the Self-education worksheet (sed) if relevant. We'll default the information and values from the mve when you open the sed.

Other expenses at Section A include:

-

Text books

-

Stationer

-

Student Union fees and student services and amenities fees

-

Course fees

-

Public transport fees

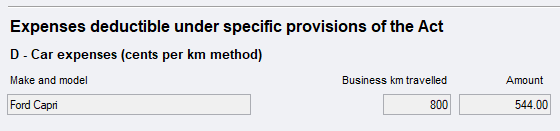

To complete item D - Car expenses per Km method

If you've completed the motor vehicle worksheet (mve) and selected to apportion some of the costs to the Self-education worksheet (sed), we'll default the information and values from the mve when you open the sed.

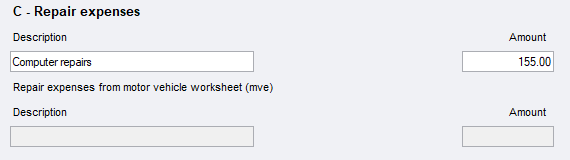

To complete label C - Repair expenses

Enter any Repair expenses

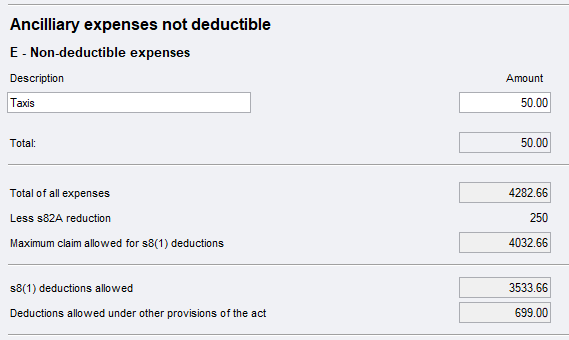

To complete item E - Non-deductible expenses, s82A and Totals

Enter any Non-deductible expenses. It is at this point that we apply the s82A deduction of $250.

To complete item B and Total self-education expenses to claim

To populate return labels and the Deductions schedule

When you close the sed worksheet, we'll add up the amounts and pass the values from the sed to:

-

Item D4 label D in the income tax return.

-

Item D4 the Deductions Schedule (DDCTNS).