Provisional tax is generally payable because you earned income during the year that either:

-

wasn’t taxed, or

-

was taxed at the wrong rate.

Provisional tax is usually payable in three instalments during the year. For example, if your 2020 residual income tax (RIT) (Box 30H of your return) is more than $2,500, you’ll become a provisional tax payer and will be liable to pay 2021 provisional tax.

For more information on provisional tax see our Provisional tax guide (IR289).

Payment dates

Provisional tax is payable on the instalment dates that fall more than 30 days after the date you ceased employment. If you have to pay provisional tax, you must pay it in:

-

three equal instalments if you ceased employment more than 30 days before the first instalment date

-

two equal instalments if you ceased employment 30 days or less before the first instalment date and more than 30 days before the second instalment date, or

-

one instalment if you ceased employment 30 days or less before the second instalment date.

For the income year ending 31 March 2021, you’ll pay:

-

three equal instalments (28 August 2020, 15 January 2021 and 7 May 2021) if you ceased employment before 28 July 2020

-

two equal instalments (15 January 2021 and 7 May 2021) if you ceased employment between 29 July and 16 December 2020

-

one instalment (7 May 2021) if you ceased employment on or after 16 December 2020.

Payment options

You have three options for paying provisional tax—the standard option (S), the estimation option (E) or the ratio option (R).

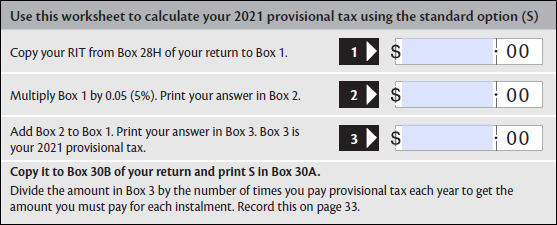

Standard option

Under this option, your 2021 provisional tax is the same as your 2020 RIT (where it is more than $2,500) plus 5%.

If your RIT is over $60,000 special interest rules apply to you—please read the guide Provisional tax (IR289).

If you’re filing your return after 28 August 2020 your instalment amounts may be different. Please read the guide Provisional tax (IR289).

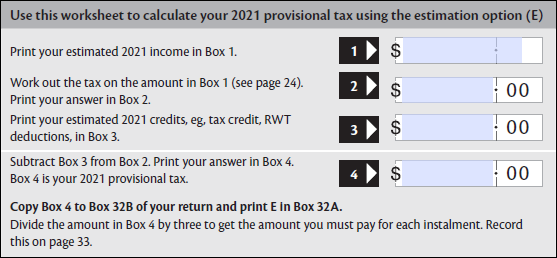

Estimation option

Anyone can estimate their provisional tax. If you expect your 2021 RIT to be lower than your 2020 RIT, estimating will keep you from paying more than you have to.

Your estimate must be fair and reasonable at the time you make it, and at each instalment date. You can be charged a penalty and/or interest if you don’t take reasonable care when you estimate your provisional tax.

If you’ve chosen to pay your 2021 provisional tax using the standard option, you can still estimate your provisional tax any time up to and including your final instalment date. Once you’ve chosen the estimation option you can’t change back to the standard option in that income year. You can re-estimate any number of times up to and including your final instalment date. Your last estimate becomes final at this date.

If you’re filing your return after 28 August 2020, your instalment amounts may be different. Please read the guide Provisional tax (IR289).