2021 provisional tax is charged for income the authority will earn in the 2021 income year. It’s generally payable in two, three or six instalments. There are three options for calculating provisional tax—standard, estimation and ratio.

If the Maori authority’s 2020 RIT is:

-

$2,500 or less it doesn’t have to pay provisional tax, but it can make voluntary payments.

-

$2,500 or less it doesn’t have to pay provisional tax, but expected to be $2,500 or less for 2021, it may estimate 2021 provisional tax at nil

-

more than $2,500 and expected to be more than $2,500 for 2021, it must pay 2021 provisional tax using one of the payment options.

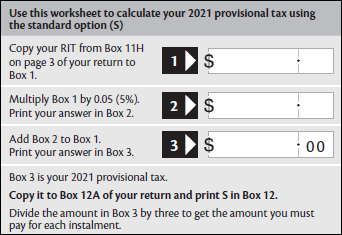

Standard option

If you use this option, write S in Box 12 of the return and the amount of 2020 provisional tax in Box 12A. 2020 provisional tax is the 2019 RIT plus 5%.

If the authority’s 2020 return hasn’t been filed by the first instalment of 2021 provisional tax, the provisional tax is the 2019 RIT plus 10%.

If you’re filing your return after 28 August 2020 your instalment amounts may be different. Please read our Provisional tax (IR289) guide.

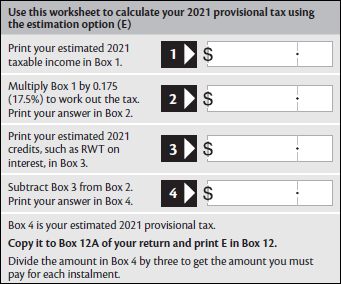

Estimation option

Maori authorities can estimate their 2021 provisional tax. They can re-estimate any number of times up to and including their third instalment due date. If the authority’s 2021 RIT is expected to be less than the 2020 tax, estimating may prevent the authority from paying more than it has to.

An estimate must be “fair and reasonable” at each instalment it applies to. Read the notes on the next page about the not taking reasonable care penalty if you use the estimation option.

If the authority estimates its provisional tax, write “E” in Box 14 and the amount of 2021 provisional tax in Box 14A.

If you estimate your provisional tax your instalments should be one-third of your estimation.

If you’re using the ratio option and select E at Box 12 this will mean that you’re electing to stop using the ratio option.

Not taking reasonable care penalty

When you estimate the authority’s 2021 provisional tax, your estimate must be fair and reasonable. If the 2021 RIT is greater than the provisional tax paid, you may be liable for a not taking reasonable care penalty of 20% of the underpaid provisional tax.

Interest

If the authority has paid too much provisional tax, Inland Revenue may pay interest, or if it has not paid enough provisional tax, Inland Revenue may charge interest.

Interest the authority pays is tax deductible, while interest Inland Revenue pay is taxable income.

Payment dates

How to make payments

You can make payments by:

-

direct debit in myIR

-

credit or debit card at ird.govt.nz/pay

-

internet banking - most New Zealand banks have a pay tax option.

When making a payment, include:

-

your IRD number

-

the account type you are paying

-

the period the payment relates to.

Find all the details of our payment options at ird.govt.nz/pay

Late payment

If you do not pay a bill on time, you may have to pay penalties and interest.

If you can’t pay your tax by the due date, call Inland Revenue on 0800 775 247. They will look at your payment options, which may include an instalment arrangement, depending on your circumstances.

Find out more at ird.govt.nz/penalties