This question will generally apply to authorities, including close companies, that own residential rental property in New Zealand or overseas that come within the residential property deduction rules in subpart EL of the Income Tax Act 2007. It will not apply if the authority is a company or a charity that is exempt from income tax.

Most residential rental properties are subject to the residential property deduction rules (also known as the ring-fencing rules). When they apply, your residential rental deductions generally cannot be more than your residential property income.

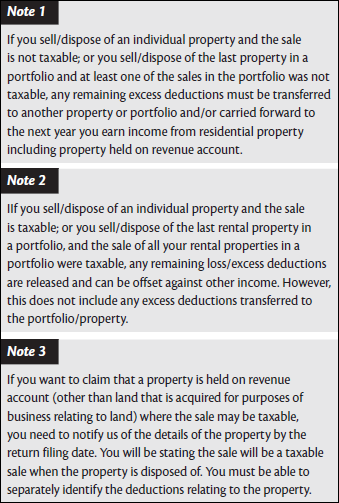

If your deductions are more than your income, the difference must be carried forward to the next year you earn residential income, including properties held on revenue account.

Refer to the Rental income - IR264 guide for information on when the rules apply, how to calculate your income, the amount of deductions you can claim this year, and the amount of any excess deductions that must be carried forward.

The residential rental deduction rules also apply to any authority that has borrowed money to acquire an interest in certain entities with significant rental property holdings - a residential land-rich entity - and has interest expenditure on the borrowed money.

Residential land-rich entity - a close company, partnership or look-through company that holds more than 50% of its assets by value in residential land directly or indirectly. They come under the interposed entities rules as part of the residential property deduction rules.

For more information about the interposed entity rules, see page 60 of the Tax Information Bulletin Vol 31 No.8 September 2019.

Completing Question 8 in your return

Tick the method you used to calculate your net residential property income and deductions. You can use one of the following:

-

Portfolio basis - combine the income and deductions for all rental properties in the portfolio.

-

Individual, property-by-property basis - the income and deductions of individual property is calculated separately to other property. You need to maintain separate records for each property to choose this option.

-

Combination of the property-by-property basis and portfolio basis - choose to apply different methods to different property. Some properties are held in a portfolio and others are held on property-by-property basis. Calculate and identify the amounts for Boxes 8A to 8F using your chosen method. Calculate your rental income and deductions as usual, as shown at boxes 4 and 14 on the Rental income - IR3R. You can then enter these figures in the Residential property deductions worksheets - IR1226 to help calculate the figures required to be entered in your return. You can print a copy from ird.govt.nz

Write the total residential income in Box 8A. This is the total of the following amounts:

-

-

all rental income from the portfolio (and/or individual property);

-

all depreciation recovery income for assets disposed of from the portfolio (or individual property);

-

net income from the taxable sale/disposal of a property in your portfolio (or individual property); and

-

all net residential rental income, depreciation recovery income and net income from the taxable disposal of the property from residential property excluded because it is held on revenue account.

-

Only include the net income from a disposal once.

Write the total residential rental deductions for residential rental properties in the Residential rental deductions in Box 8B.

This is the total before adjusting for excess deductions.

Write the total excess deductions brought forward from last year in Box 8C. This box cannot be completed for the tax year ending 31 March 2020.

Calculate the amount of allowable deductions you can claim this year adjusting for excess deductions. Write the total Residential rental deductions claimed this year in Box 8D. The amount that can be claimed and entered in box 8D depends on the methods chosen for all the authority’s properties. Use the IR1226 worksheets to help calculate the amount. This should equal Box 8B plus Box 8C less the amount of excess deductions for each property and/or property portfolio shown in Box 8F.

The amount cannot exceed total residential income at Box 8A, unless there was a taxable sale/disposal of a rental property.

Combine the net income results (after adjusting for any excess deductions) for all properties and write the total in Box 8E. Your total Net residential income in Box 8E cannot be a loss, unless the rental property or all the properties in the portfolio have been disposed of as taxable sales.

Any losses are counted as zero unless the loss is the result of either:

-

excess deductions released as the result of the taxable disposal of the rental property or all properties in a portfolio

-

claimable interest paid on your investment in a residential land-rich entity, (refer to the Rental income - IR264 guide).

Write the amount of all excess deductions for the year to be carried forward to next year in Box 8F.

This is calculated as Residential rental deductions Box 8B minus Residential rental deductions claimed this year Box 8D. This includes the amount of any excess deductions to be carried forward for interest paid on an investment in a land rich entity in Box 8F.

Notes