To lodge this form with the ATO, the applicant must be claiming a refund of franking credits and have no requirement to lodge a current year tax return.

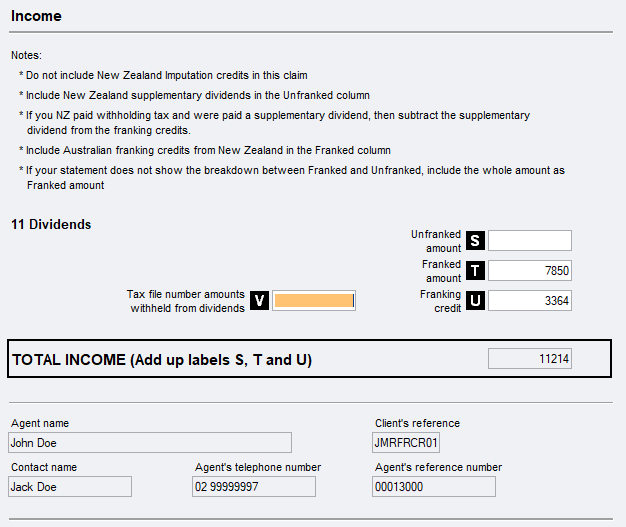

This is a short form individual return with front cover information and access to item 11 dividends fields: labels S, T, U and V from the Income tab.

be a resident of Australia for tax purposes for the whole of the income year

not be claiming a refund for a deceased estate.

If older than 18 years at the end of the income year:

Have total grossed-up dividend income of less than $18,200

The franking credit (item 11 label U) must be less than $5,461

There must be no other income or claim for rebates or tax offsets.

OR

If under 18 years of age at the end of the income year:

Have a total dividend income of $417

The franking credit (item 11 label U) must be less than $216

Have received dividends from shares (or non-share equity interest) in an Australian or New Zealand company, or were entitled to distributions from investments in a managed fund

Have a dividend or distribution statement showing franking credits (New Zealand imputation credits do not qualify), or

Amounts were withheld from the dividends because the applicant did not provide a tax file number to the investment body.

To convert an individual return to the Refund of franking credits short form

Open the return and click Return properties.

Select the Standalone refunds checkbox.

Click OK or F6 to exit. The client details are pre-filled.

Click the Income tab to open the Dividend worksheet (div) and enter the total amount of dividends received. We'll automatically calculate the franking credit. You can enter a different amount if your total differs due to partially franked dividends.

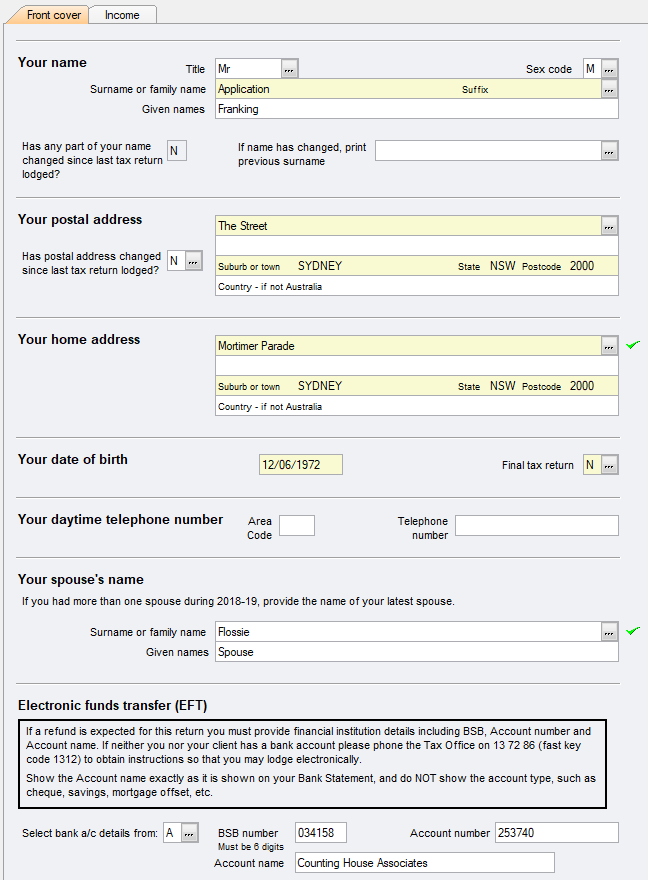

Front cover field descriptions

Item

Description

Tax File Number

The TFN defaults from the Return properties > GeneralTab. Tax file numbers are validated in accordance with PLS specifications. The TFN must not belong to anyone other than the taxpayer.

Are you a resident of Australia?

The default is Yes as you must be an Australian resident for tax purposes for the whole of the current income year to make this claim.

Home Address

The Home address must be a Street address. It can't be a Post Office Box or Private Mail Bag and must be the current residential address of the individual. These details default from the address as recorded on the Return PropertiesMail Tab.

Date of Birth

This is a mandatory field and must be completed. It defaults from the Defaults tab of the Return Properties. If the taxpayer is under 18 years of age at 30 June of the current income year, the dividend income and franking credit are reduced. Dates must be entered in the format dd/mm/ccyy. The century will default to 20, key a hyphen (-) to change the century to 19.

Daytime phone number

This is the taxpayer's daytime number and not the phone number of the Practice's contact. These are not mandatory fields but if one is completed then both must be completed.

Contact Name

This is the name of the person in the Practice to whom the ATO can direct enquiries in relation to the return. The name defaults from the Agent details nominated in the Return Properties >Staff Tab. If there is no Agent nominated in the Staff Tab, then the name defaults from the Control Record > Names/Audit Tab.

Tax agent contact number

This is the 'phone number of the contact for the return. It defaults from the Contact details nominated in the Return Properties >Staff Tab. If there is no agent nominated in the Staff Tab, the name defaults from the Control Record > Names/Audit tab.

Spouse name

If you are married or have a de facto spouse, enter the spouse's name. If you act for the spouse, click F10 to retrieve the spouse's details.

EFT details

This field is mandatory. The bank account details can be for a bank account other than the taxpayer's bank. If the bank account details have been set up in the Return Properties press F10 at Select account details from. Up to two sets of bank account details can be stored in the Bank a/cs tab. Your client, the applicant, must sign the EFT section of the PLS declaration.

CCH References

4-820 Refund of excess franking credits

21-010 Residence of individuals generally

Add this back if the tag forms are available. PD to confirm

For a PDF version of the Standalone Franking Credits return showing tags and tax codes, refer to Individual Standalone Claim.

JavaScript errors detected

Please note, these errors can depend on your browser setup.

If this problem persists, please contact our support.