The Tax application calculates this amount from the amounts entered at labels H1, H2, H3, H4, H5, H7 and H8, displayed on the left of the Calculation Statement (Company) tab.

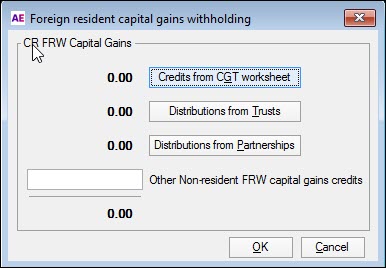

Label H8 - Credit for foreign resident capital gains withholding amounts

Show at label H8 the total amount of tax withheld from payments to the company that were subject to foreign resident capital gains withholding in Australia. Include at H8 the Company's share of foreign resident capital gains withholding credits distributed to the Company from its share of net income from a partnership or a trust or from any other source.

You should only claim at H8 a credit equal to the amount of foreign resident capital gains withholding paid by a purchaser to the ATO on your behalf. The ATO would have issued you with confirmation of this amount.

Do not include credits for amounts withheld from foreign resident withholding (excluding capital gains) at H8. Include these at H2 Credit for tax withheld - foreign resident withholding (excluding capital gains).