In March 2020, the government introduced a time-limited 15-month investment incentive to support business investment and economic growth over the short-term, by accelerating depreciation deductions.

These depreciation rules apply to businesses with an aggregated turnover between $10 million and $500 million and small business entities (SBE) with a turnover of less than 10 million.

The new rules are:

-

The instant write-off amount has increased to $150,000 for assets purchased on or after 12th March 2020.

-

Using an accelerated rate to depreciate the cost of assets.

In circumstances where the entity is not an SBE different accelerated depreciation rules apply.

Instant write-off

The instant asset write-off threshold has increased from $30,000 to $150,000.

To qualify for an instant write-off:

-

the business turnover should be less than $500 million.

-

the asset must have been purchased and first used or installed and ready for use on or after 12 March 2020.

-

the asset must be used for business purposes. If there's private use, claim only the business %.

Business with turnover of less than $500 million (not a SBE)

Entities with turnover between $10 million and $500 million do not qualify for the simplified depreciation rules.

For each new asset, the accelerated depreciation deduction applies in the income year that the asset is first used or installed ready for use for a taxable purpose. The usual depreciating asset arrangements apply in the subsequent income years that the asset is held.

Instant asset write-off (assets costing less than $150,000)

|

Date when the asset was used or installed |

Eligible businesses with a turnover of |

Threshold |

|---|---|---|

|

12 March 2020 to 30 June 2020 |

More than 10 million and less than $500 million |

$150,000 |

|

01 July 2019 to 11 March 2020 |

Less than $50 million |

$30,000 |

Accelerated rate (assets costing more than $150,000)

To qualify for an accelerated rate, the asset must be newly purchased and not been used/held previously.

The accelerated rate of depreciation can be applied for assets costing more than $150,000. The entities will be able to deduct:

-

50% of the cost of the asset plus the amount of the usual depreciation deduction that would apply calculated after first offsetting a decline in value of 50%.

You can apply this depreciation for the two methods:

-

Prime Cost (P)

-

Diminishing value (D)

Accelerated rate calculation

Formula: (Asset cost * 50%) plus (applying the usual percentage Diminishing value/Prime Cost method after deducting the 50%)

For example:

-

Asset cost: $200,000.

-

Annual rate: 10%

-

Date first bought/used: 01/04/2020 (held of 91 days)

First 50% deducted: (200,000 * 50%) = $100,000

Applying the usual method of depreciation

100000 * 10% * (91/365) = $2493

Total business depreciation: $100,000 + 2493 = 102493.

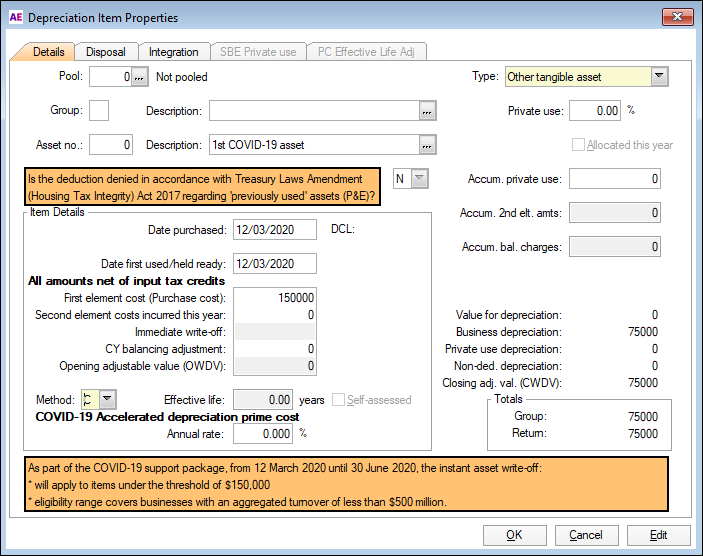

To add an asset using the COVID rules

To qualify for the depreciation, answer Y at the COVID -19 support for Business questions.

These questions can be found in a:

-

company return at item 3 Status of company (front cover).

-

individual return at item 15 under label A.

-

partnership return and the trust return immediately before item 6.

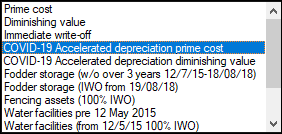

In the depreciation worksheet (d), we've added 2 new COVID-19 depreciation method codes for prime cost and diminishing value.

For the correct calculation, make sure:

-

the Date purchased and Date first used/held is on or after 12 March 2020.

-

to select the relevant COVID-19 code at Method.

You'll also see on-screen messages related to the new COVID-19 rules

Business with turnover of less than $10 million (SBE)

If you’re a small business with an aggregated turnover of less than $10 million and use the simplified depreciation rules.

For any asset over the instant asset threshold, apply the accelerated depreciation.

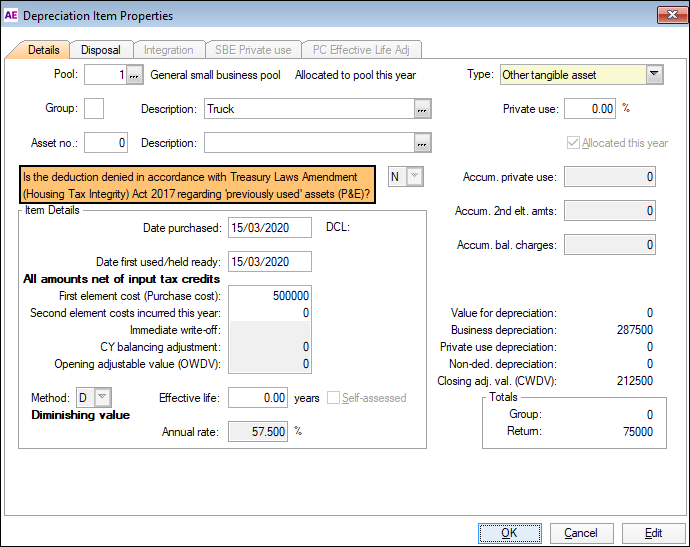

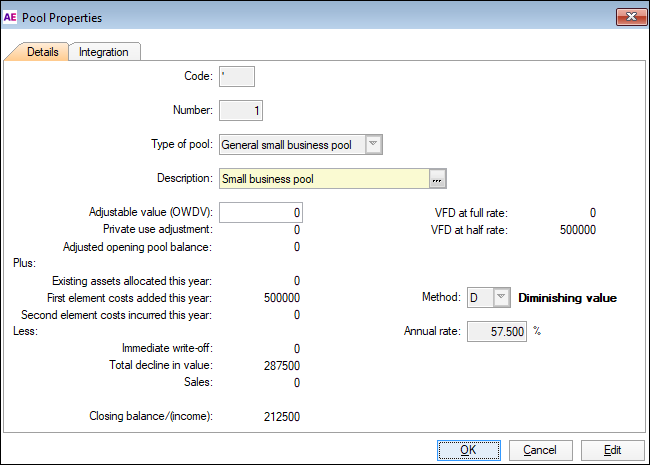

These assets are added to the general small business pool.

You can deduct an amount equal to 57.5% (rather than 15%) of the business portion of a new depreciating asset in the year you add it to the pool.

Instant asset write-off (assets costing less than $150,000)

If you choose the simplified business rules, you must use the instant write-off for the eligible assets. Assets costing less than $150,000 is an instant write-off when added to the general small business pool.

If the pool balance is less than $150,000, the pool is written off.

|

Date when the asset was used or installed |

Eligible businesses with a turnover of |

Threshold |

|---|---|---|

|

12 March 2020 to 30 June 2020 |

Less than 10 million |

$150,000 |

|

01 July 2019 to 11 March 2020 |

Less than $50 million |

$30,000 |

Accelerated rate (assets costing more than $150,000)

An asset is eligible for an accelerated depreciation rate using the simplified depreciation rules if the SBE has:

-

an aggregated income of less than $10 million,

-

an asset costing more than $150,000 and

-

the asset was first used and installed for tax purposes between 12 March 2020 and 30 June 2020.

In MYOB Tax, when you add an asset to the small business pool:

-

the depreciation deducted is 57.5% of the business portion of the new asset in the year that it’s added to the pool

-

in later years the asset depreciates at 30%, as part of the general small business pool rules.

This applies to companies, individuals, partnerships, and trusts.

To add an asset using the COVID rules

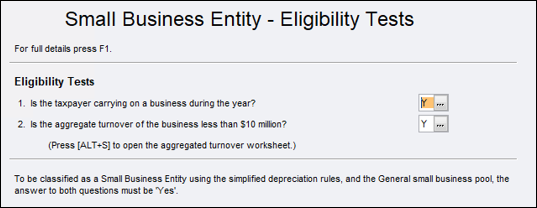

To qualify for the depreciation, you must answer Y to Eligibility tests questions 1 and 2 in the Small business entity - eligibility tests worksheet.

The COVID-19 questions default to Y and we calculate the depreciation using the COVID-19 rules for the entity.

In the depreciation worksheet (d), for the correct calculation:

-

the Date purchased and Date first used/held is on or after 12 March 2020.

-

if the asset cost is less than $150,000, it will be an instant write-off when adding to the pool.

-

if the asset cost is greater than $150,000, the new rate of 57.5% is applied.

The depreciation rate reverts to 30% (the standard rate for an SBE depreciation pool) from the second year onwards.

Depreciation rate threshold table