Label I - Interest Deductions

From 1 July 2018 where you have expenses of this nature, the ATO requires you to lodge a Deductions schedule (DDCTNS).

These new requirements have seen both the Interest deductions worksheet (idd) removed and the ATO Interest and dividend deductions schedule (BJ) discontinued.

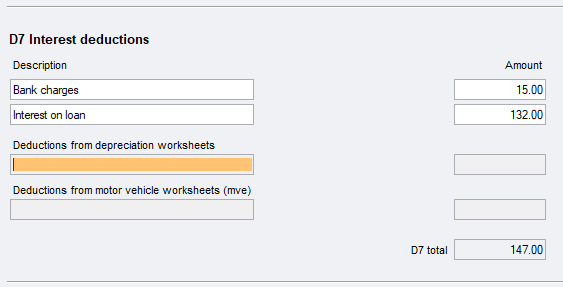

Click label I to open the ATO Deductions schedule at D7. Do not aggregate your interest expenses as each must be detailed separately. For this purpose you can have up to a total of 20 entries.

To add a row press Ctrl+Insert. To remove excess rows, press Ctrl+Delete.

Amounts allocated to item D7 from the Motor vehicle worksheet (mve) 2023 and the Depreciation worksheet (d) will be passed to the Deductions schedule.

On closing the Deductions schedule, we'll pass the total of the amounts entered to item D7 label I in the income tax return.

Thin Capitalisation

If the taxpayer has debt deductions, such as interest, the claim may be affected by the thin capitalisation rules. These rules may apply if:

-

the taxpayer is an Australian resident for tax purposes and has (or any associate entities have) certain overseas interests, and the debt deductions combined with those of the associate entities were more than $2 million for the current income year, or

-

the taxpayer is a foreign resident with operations or investments in Australia and the debt deductions against Australian assessable income (combined with those of the associate entities) were more than $2 million for the current income year.

You cannot have interest deductions if there is no interest income at item 10.