Completing the Income and Expenses

Entering the rental income

From 1 July 2020, the PLS Multi-property rental schedule (RNTLPRPTY) replaces the ATO Rental schedule (RS,) and must be lodged for Individuals owning one or more rental properties.

If you've completed more than one rental schedule, we'll combine all the details and send them to the ATO as one schedule.

|

Field |

Description |

|---|---|

|

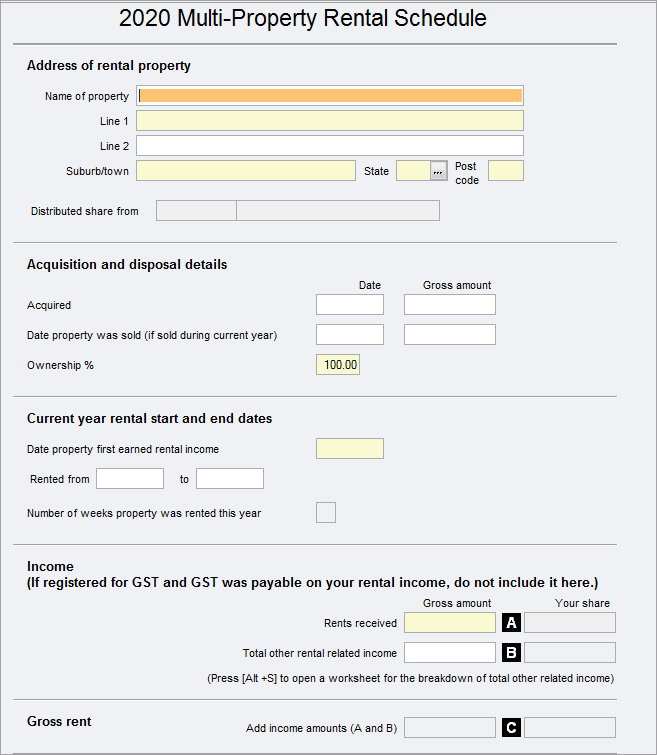

Address of the rental property |

Enter the address of the rental property. Make sure there are no special characters in the address fields. The allowed characters are numbers, alphabets and &/'\-\(\) \*#,\.]). |

|

Acquisition and disposal details |

|

|

Acquired |

Enter the date and the purchased amount

|

|

Date property was sold (if sold during the current year) |

Enter the date when the property was sold and the selling value. |

|

Ownership % |

Enter the % of ownership for this taxpayer. This is a mandatory field. You can enter decimal values in this field. For example, 33.33% |

|

Current year rental start and end dates |

|

|

Date property first earned rental income |

This is a mandatory field. |

|

Rented from to |

Enter the dates when the property was rented from (within the financial year) |

|

Number of weeks the property was rented this year |

This is a calculated field based on the dates entered in Rented from and to. (This field is not part of any calculation of income or expenses) |

|

Income |

|

|

Rents received |

Enter the Gross amount when the property is rented. Do NOT reduce this figure by deducting agent's commission or other costs. |

|

Total other rental related income |

Use the grid to enter other rental related income such as rental bond money, insurance compensation, letting or booking fees. This change was made as only the totals get transmitted to the ATO. |

|

Your share |

This is a calculated field.

% |

|

Gross rent |

This is a calculated field. Label A + B. |

Entering the rental expenses

|

Field |

Description |

|---|---|

|

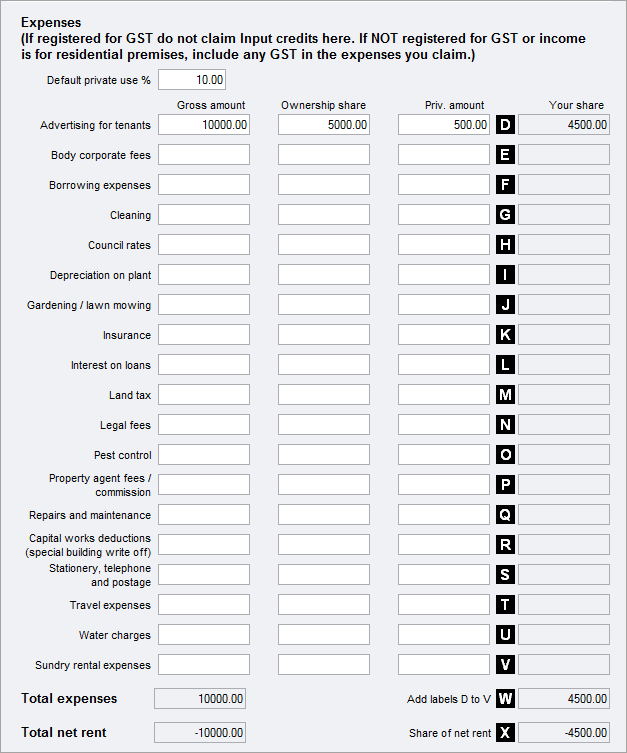

Default private use % |

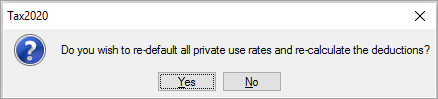

Enter the private use % and click Yes if you want to default this rate for all the expenses.

You can manually overwrite any expenses if the private use % is different. Use Private amount field to overwrite any amounts. |

|

Gross amount |

This is a mandatory field. You must enter an amount at this field if you're entering an amount at Ownership share or Private amount fields |

|

Ownership share |

This is a calculated field.

|

|

Private Amount |

This is a calculated field.

You can overwrite if the % of the private use is not the same as Default private %. Private.amount cannot be greater than the ownership share field. |

|

Your share |

This is a calculated field.

|

If the owner pre-pays a rental property expense such as insurance or interest on money borrowed, that covers a period of 12 months or less and the period ends on or before 30 June of the current income year, you can claim an immediate deduction.

A pre-payment that doesn’t meet these criteria and is $1,000 or more, may have to be spread over two or more years. This is also the case if the owner carries on the rental activity as a small business entity and has not chosen to deduct certain pre-paid expenses immediately.

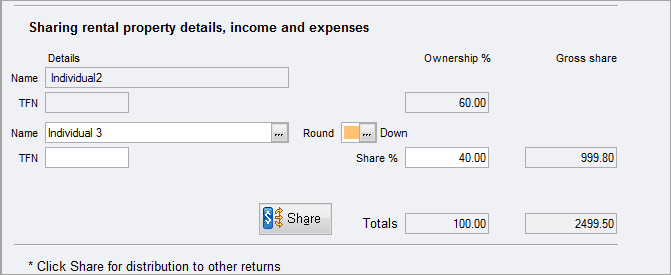

Sharing of Income and Expenses

This is the area of the worksheet where the details of co-owners of the property are entered, together with the share of the Net Rental Income each is to receive:

|

Name, TFN, Ownership %, Gross share |

There are 2 sets of these 4 fields. The first set is reserved for the Host return and is set with the details of the taxpayer. The ownership % is pre-filled from the ownership % field in the Acquisition and disposal details section. To complete the second owner,

To add another owner, press Ctrl + Insert to add a record. After you've entered all the details, click Share. |

|

Round |

Rounding may be necessary where the income to be shared results in uneven amounts. The default method applied in this schedule is Natural rounding: Click [F10] to display an index of rounding methods.

|

|

Gross Share |

This field is automatically calculated by Tax applying the % Share entered for the owner or co-owner to the Net income available for sharing |

|

Share |

Click the Share button after you've entered the Share %. This will calculate Totals field. If you make any change to the income, expenses, or ownership %, make sure to click Share for the Totals to update. |

For Accountants Enterprise and Series 6 & 8, when apportionment of income and expenses varies on an ad hoc basis between co-owners, click [F5] to copy the original schedule to the other owners, and edit each according to requirements.

When re-copying a rental schedule, the destination return's original copy will be overwritten if the address matches exactly that of the rental property already on file for the destination return. This avoids accidentally adding more than one schedule for the same property.