What does the Stapled Structures Act cover?

The Stapled Structures Act includes the following:

Schedule 1 ensures that trading income that is converted to passive income via a stapled structure or distributed by a trading trust, and income from agricultural land and residential housing (other than affordable housing), will be subject to a 30% withholding tax rate. Fund payments, to the extent that they are attributable to non-concessional MIT income (NCMI), will be subject to a 30% withholding tax rate.

Data entry into the labels:

|

Income category |

Label at this item |

Include this in another label in the return |

|---|---|---|

|

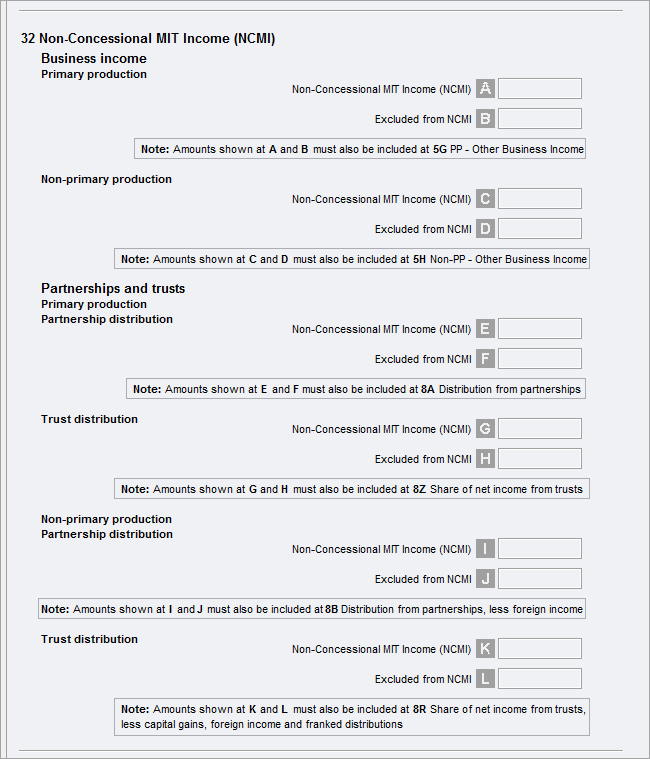

Business income |

Label A: Primary Production – Non-Concessional MIT Income (NCMI). Label B: Primary Production – Excluded from Non-Concessional MIT Income (NCMI). |

Item 5 Label G - Other Business income |

|

Label C: Non-Primary Production –Non-Concessional MIT Income (NCMI). Label D: Non-Primary Production – Excluded from Non-Concessional MIT Income (NCMI). |

Item 5 Label H - Non-PP – Other business income |

|

|

Primary production (Partnership distributions) |

Label E: Primary Production – Non-Concessional MIT Income (NCMI) Distribution from Partnerships. Label F: Primary Production – Excluded from Non-Concessional MIT Income (NCMI) Distribution from Partnerships. |

Item 8 Label A - Distribution from partnerships |

|

Primary production (Trust distributions) |

Label G: Primary Production – Non-Concessional MIT Income (NCMI) Share of Net Income from Trusts. Label H: Primary Production – Excluded from Non-Concessional MIT Income (NCMI) Share of Net Income from Trusts. |

Item 8 Label Z - Share of Net Income from Trusts |

|

Non Primary production (Partnership distributions) |

Label I: Non-Primary Production –Non-Concessional MIT Income (NCMI) Distribution from Partnerships less foreign income. Label J: Non-Primary Production – Excluded from Non-Concessional MIT Income (NCMI) Distribution from Partnerships less foreign income. |

Item 8 Label B - Distribution from Partnerships less foreign income. |

|

Non- Primary production (Trust distributions) |

Label K: Non-Primary Production –Non-Concessional MIT Income (NCMI) Share of Net Income from trusts, less capital gains , foreign income and franked distributions. Label L: Non-Primary Production – Excluded from Non-Concessional MIT Income (NCMI) Share of Net Income from trusts, less capital gains , foreign income and franked distributions. |

Item 8 Label R - Share of net income from trusts, less capital gains, foreign income and franked distributions. |