Before completing the worksheet and claiming the ESVCLP tax offset, it's important to read the ATO information

Tax incentives for innovation

.

To complete the worksheet

-

Click in Goto (F2) and enter 22 then press Enter

-

Click label L to open the front entry screen of the esv worksheet.

-

The ESVCLP unconditionally registered on or after 7 December 2015 question is mandatory.

-

Enter any excess brought forward at the beginning of the year, adjusted in accordance with Div 65 of the ITAA 1997 for the effects of any net exempt income (foreign or Australian).

-

Click the Worksheet button and enter the details.

.png?cb=95aa418e1e6922ee83d707c9b3314cf0)

-

Press F6 or click OK or the Save icon to save the transaction. The transaction moves to the stored area of the worksheet and the running total shows at the bottom of the worksheet.

_2.png?cb=2063bc0ce18720c20f7dde7d9aec8877)

-

To add additional ESVCLP acquisition details repeat the process.

If you buy shares in the same Venture capital company at a different date, you must create a separate entry. Do not add a new acquisition to an existing one as there are capital gains implications on disposal.

-

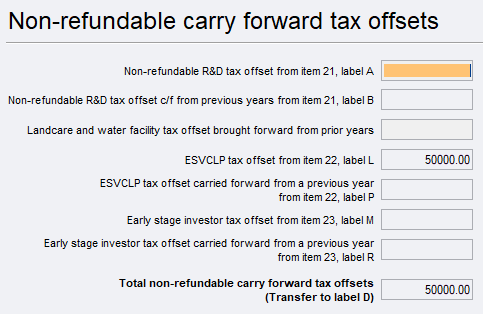

If there are no further transactions, click Close, then F6 or click OK or the Save icon at the front entry screen to close the worksheet. We'll filter the Offset total through to label L and to the Non-refundable carry-forward tax offsets worksheet (ncf) in the Calculation statement at label D: Non-refundable carry-forward tax offset

_3.png?cb=02603b8a857f7fe715e93cbad8df3288)

-

The F4 estimate prints a summary of the ESVCLP tax offset showing how it was applied and any excess to be carried forward at the end of the year.

The ESVCLP tax offset is not included when calculating GDP-Adjusted net income for PAYG Income tax instalments purposes.

To record any share of ESCVLP tax offset distributed to the company from a partnership or trust, you must enter these details in the:

-

Distributions from partnerships worksheet (dip), income item 6: Gross distribution from partnerships—label D. See Distributions from partnerships worksheet (dip) 2026

-

Distributions from trusts worksheet (dit), income item 6: Gross distributions from trusts—label E. See Trust income schedule (DISTBENTRT) and Distributions received from trusts (dit) 2026

Any share of ESVCLP tax offset received will be added to the esv worksheet with the Code D and will be included in the total offset to be claimed at Item 22: Early stage venture capital limited partnership tax offset—label L, and is then passed to the Calculation statement: Non-refundable carry forward tax offsets worksheet (ncf) at label D. See Non-Refundable carry forward tax offsets worksheet (ncf) 2026

CCH References

20-700 Outline of innovation incentives