Reconciliation items are adjustments for tax purposes to reconcile the book Total profit or loss at item 6 label T, to Taxable income or loss at item 7 label T.

Use the worksheets Other Additions Items (add) and Other Subtraction Items (sub) to assist with the reconciliation. All figures entered will be passed to the correct label in the main return.

See Other Addition Items worksheet (add) and Other Subtraction Items worksheet (sub).

Companies that have one or more CGT events during the income year must complete a Capital gains tax schedule (BW) to lodge with the current year return if:

-

total current year capital gains are greater than $10,000, or

-

total current year capital losses are greater than $10,000.

Label G - Did you have a CGT event during the year?

This is a mandatory question and we've defaulted the answer to No.

If you've had a capital gains event during the current income year or substituted accounting period, you must answer the question Yes and complete labels G, M and A.

If the capital gain or capital loss exceeds $10,000, you must complete the ATO Capital Gains schedule (BW) to be lodged with the return.

Use the Capital gains worksheet (g) 2018 2018 2018 and we'll calculate the gain or loss for each asset disposed of and apply losses when the worksheet is closed. You can also share the Capital gain or loss with other taxpayers.

We'll also calculate the correct exemption or rollover code for label M.

Distributions of Capital gains from a trust that you've entered in the Distributions from trusts worksheet (dit) are also correctly dealt with in the worksheet (g). See Distributions received from trusts worksheet (dit)

The worksheet is powerful and has functionality to deal with most aspects of Capital gains. It will populate the ATO's Capital Gains schedule (BW) with the sum of all transactions in their various categories if you tick the Populate BW box in the Index of Capital gains transactions.

For the full details of the functionality available when using the worksheet (g) see Capital gains worksheet (g) 2018 2018 2018.

Label M - Have you applied an exemption or rollover?

At label M enter Yes if you've applied an exemption or rollover to the capital gain.

If you are not using the Capital gains worksheet (g), and you have more than one disposal where you have exempted the gain or rolled it over, then you must choose the code that represents the largest of the capital gains.

Label A - Net capital gain

Show at this label the company's net capital gain.

If you are not using the Capital gains worksheet (g) and the amount is $10,000 or more, you must complete the ATO's current year Capital gains schedule (BW).

If you are using the worksheet (g), then you close the worksheet, we'll add up all the transactions by category and apply losses category by category, current year, then prior year and pass all the values to the correct labels in the Return and to the Capital Gains schedule BW.

A company is not eligible for the CGT discount.

You may also need to lodge a Losses schedule if the Capital Loss is greater than $10,000.

Label U - Non-deductible exempt income expenditure

Show at this label any expenditure incurred in deriving exempt income included at item 7 label V.

Do not include

Expenditure incurred in deriving exempt income from retirement savings accounts (RSAs) and debt deductions allowed by section 25-90 of the ITAA 1997.

Click label U to open the Generic Schedule / Worksheet.

Label J - Franking credits

Show at this label the amount of franking credits attached to assessable distributions received from Australian corporate tax entities.

Do NOT include franking credits attached to:

-

A distribution the company receives indirectly through one or more partnerships or trusts. Include these at label D Gross distribution from partnerships item 6 or label E Gross distributions from trusts item 6.

-

A distribution that is exempt income or non-assessable non-exempt income, or

-

Franked distributions received from a New Zealand franking company. Include these at item 7, label C - Australian franking credits from a New Zealand company, or

-

A distribution where the shares are not held at risk as required under the holding period and related payments rules, or there is other manipulation of the imputation system. There is no entitlement to a franking tax offset in these circumstances.

Under the simplified imputation system a company is required to include in its assessable income the amount of franking credits attached to assessable franked distributions received.

Click label J to open the Dividends Worksheet for entities (div). All amounts will be passed passed to the relevant fields in the income tax return.

Maximum franking credit allowable

The maximum franking credit that can be allocated to a frankable distribution is based on a company's corporate tax rate for imputation purposes. For the current income year, a company's corporate tax rate for imputation purposes may be either 27.5% or 30% depending on the company's circumstances.

For most companies the sum of all allowable franking credits for the income year entered here is allowable as a tax offset and should be claimed in the Calculation statement at label C Non-refundable non-transferable and non-carry forward tax offsets.

For a Life insurance company (LIC) or organisation entitled to claim a refund of excess franking credits, the excess tax offset is claimed in the Calculation statement at label E Refundable tax offset and not at label C Non-refundable non-carry forward tax offsets.

In circumstances where the shares are not held at risk as required under the holding period and related payments rules, or there is other manipulation of the imputation system, the franking credit is not included in assessable income at label J and there is no entitlement to a franking tax offset.

Label C - Australian franking credits from a New Zealand company

See Trans-Tasman Imputation System Overview for further information.

Show at label C amounts of Australian franking credits from a New Zealand company that are included in assessable income because of a franked distribution paid to the company by a New Zealand company or because of its receipt indirectly through a partnership or trust. To work out whether the distribution is included in assessable income.

Use the Foreign income worksheet to record these transactions and to return calculated figures to the relevant labels in the main return.

Click label C to open the Foreign income worksheet (for).

If the shares or interests are not held at risk as required under the holding period and related payments rules, or there is other manipulation of the imputation system, do not include the Australian franking credit in assessable income at label C and there is no entitlement to a franking tax offset.

For most companies the amount of Australian franking credits included at label C is allowable as a tax offset and should be claimed in the Calculation statement at label C Non-refundable non-transferable and non-carry forward tax offsets. If the company is a life insurance company or organisation entitled to claim a refund of excess franking credits, claim the refundable amount in the Calculation statement at label E Refundable tax offsets.

A dividend from a New Zealand franking company may also carry New Zealand imputation credits. An Australian resident cannot claim any New Zealand imputation credits.

Label E - TOFA Income from financial arrangements not included at item 6

If the company has financial arrangements to which the TOFA rules apply, include at item E TOFA income from financial arrangements not included in item 6:

-

Assessable gains under the TOFA rules from financial arrangements which have not been shown at item 6.

The Taxation of financial arrangements worksheet (tof) is provided at this label for dissection and record-keeping purposes.

Label B - Other assessable income

Click label B to open the Other Addition Items worksheet (add) which contains a full list of items making up this label.

The total of the amounts entered into the fields at the top of the ‘add’ worksheet under the heading Other Assessable Income Label B integrates to Label B in the return.

Label W - Non-deductible expenses

Show at this label expense related adjustments that are added back to the amount shown at label T Total profit or loss item 6 to reconcile with the amount shown at label T Taxable income or loss item 7.

Click label W to open the Other Addition Items worksheet (add) which contains a full list of items making up this label. The total of the amounts entered into the fields at the bottom of the worksheet under the heading Non-Deductible Expenses Label W integrates to Label W in the return.

Depreciation Expense amounts integrate from the amount entered into the Reconciliation Other Additions Schedule (add) at the field Depreciation as per Accounts - Label X. The Depreciation worksheet provides for you to compile an index of assets that you maintain from year to year.

If a forex loss for accounting purposes shown at item 6 exceeds the deductible forex loss, show the difference at label W. For more information about forex measures, refer to Foreign exchange gains and losses in the current year.

If Australian and foreign sourced capital losses for accounting purposes are included at label G Unrealised losses on revaluation of assets to fair value item 6, show them also at label W. For Australian taxation purposes, include any net capital loss with any unapplied capital losses carried forward to later income years and at label V Net capital losses carried forward to later income years at item 13.

Label D - Accounting expenditure in item 6 subject to R&D tax incentive

Show at this label the expense amounts included at the expenditure labels in item 6-Calculation of total profit or loss, which relate to amounts that are subject to the R&D tax concession provisions (Australian owned R&D tax concession and foreign owned R&D tax concession).

Generally, these amounts include expense amounts for accounting purposes related to Research and Development activities, for which different amounts will be claimed for income tax purposes.

Click label D to open the Research and development tax incentive (BY).

You should also include at label D losses on disposal of assets used in R&D incentive, the expense amounts included at the expenditure labels at item 6 Calculation of total profit or loss, which relate to amounts that you are claiming as a notional R&D deduction under the R&D tax incentive provisions. Generally, these amounts include expenditure for accounting purposes on R&D activities, which are used in calculating the R&D tax offset, rather than being claimed as allowable deductions. In addition, also include at label D Accounting expenditure in item 6 subject to R&D tax incentive losses on disposal of assets used in R&D activities which are subject to the R&D tax incentive that were shown at label S All other expenses item 6 and any book depreciation expenses for assets used in Research & Development activities which are subject to the R&D tax incentive that were included at label X Depreciation expenses item 6 (any amounts not subject to the R&D tax incentive must be included at label W Non-deductible expenses item 7).

If no expense amounts relating to R&D deductions have been included at item 6 (for example, amounts are capitalised) enter a zero (0) at label D Accounting expenditure in item 6 subject to R&D tax incentive.

The amount shown at label D Accounting expenditure in item 6 subject to R&D tax incentive in the company tax return must be the same as the amount shown at label D-Preliminary calculation - Add-back of research and development (R&D) accounting expenditure on the Research and development tax incentive schedule.

Subtraction labels

Label C - Section 46FA deduction for flow-on dividends

Show at this label any amounts claimed as a deduction during the current income year that are deductible under section 46FA of the ITAA 1936.

If you complete label C, you must also complete an International dealings schedule (I) to lodge with the return via PLS.

Click label C to open the Generic Schedule / Worksheet.

This deduction is allowable in certain cases for an on-payment of unfranked non-portfolio dividend by a resident company to its non-resident parent.

Where a deduction is claimed under section 46FA, the claiming entity is required under section 46FB of the ITAA 1936 to maintain an unfranked non-portfolio dividend account and complete item 8, label L-Balance of unfranked non-portfolio dividend account at year end.

Label F - Deduction for decline in value of depreciating assets

Use the Depreciation worksheet (d) to manage all depreciating assets under the Small business simplified depreciation rules or Pooling. Refer to Depreciation worksheet (d).

The Depreciation Expenses shown at this label are accounting or book figures and if MAS Integration (AE) or Accounts Integration (Series 6 & 8) is used, the amount will default from the general ledger.

Click label F to enter the various amounts in the Generic Schedule / Worksheet .

If the company is not a small business entity using the simplified depreciation rules, include the deduction for decline in value of most depreciating assets for taxation purposes at label F Deduction for decline in value of depreciating assets.

This amount is often different from the amount of depreciation calculated for accounting purposes shown at label X Depreciation expenses item 6 and added back at label W Non-deductible expenses item 7.

If the company has allocated depreciating assets to a low-value pool, the deduction for decline in value of those assets is also included at label F Deduction for decline in value of depreciating assets.

If a depreciating asset is used in R&D activities, the notional decline in value amount will form part of your notional R&D deduction. Eligible companies can claim this notional R&D deduction amount in calculating the R&D tax offset.

If a decline in value amount is included as a notional R&D deduction, add back at label D Accounting expenditure in item 6 subject to R&D tax incentive at item 7 any related depreciation expenses included at label X Depreciation expenses item 6.

If you have elected to use the hedging tax-timing method provided for in the TOFA rules and you have a gain or loss from a hedging financial arrangement used to hedge risks in relation to a depreciating asset, work out separately:

-

The deduction for decline in value of depreciating assets (include this at F Deduction for decline in value of depreciating assets), and

-

Your gain or loss on the hedging financial arrangement; include this at either:

-

label E TOFA income from financial arrangements not included in item 6, item 7, or

-

label W TOFA deductions from financial arrangements not included in item 6 or item 7.

Include the decline in value of water facilities at label N Landcare operations and deduction for decline in value of water facility item 7.

For information about how to work out deductions for decline in value, refer to Appendix 6 of the Company tax return instructions.

If the company is a small business entity using the simplified depreciation rules, include deductions for depreciating assets at label X Depreciation expenses item 6.

If the company is not using the simplified depreciation rules, and is continuing to claim a deduction for any prior pool, this deduction should be included at X Depreciation expenses item 6.

Practice Statement PS LA 2003/8 provides guidance on two straightforward methods that taxpayers carrying on a business can use to help them determine whether expenditure incurred to acquire certain low-cost assets is to be treated as revenue or capital expenditure.

Subject to certain qualifications, the two methods cover expenditure below a threshold and the use of statistical sampling to estimate total revenue expenditure on low-cost items. Under the threshold rule, low-cost items with a typically short life costing $100 or less are assumed to be revenue in nature and are immediately deductible. The sampling rule allows taxpayers with a low-value pool to use statistical sampling to determine the proportion of the total purchases of low-cost tangible assets that are revenue expenditure.

Label U - Forestry managed investment scheme deduction

The Company may be able to claim a deduction at label U for payments made to an FMIS, if the Company:

-

Currently holds a forestry interest in an FMIS or has held a forestry interest in an FMIS during the current income year, and

-

Paid an amount to a forestry manager of an FMIS under a formal agreement.

The Company can claim a deduction at label U only if the forestry manager has advised you that the FMIS satisfies the 70% direct forestry expenditure rule in Division 394 of the ITAA 1997.

Show at label U the total amount of deductible payments made to an FMIS. If you complete label U, you must also complete Item 9 - Forestry Managed investment scheme labels G, H and I.

Click label U to open the Forestry managed investment scheme worksheet (fms).

Label E - Immediate deduction for capital expenditure

Companies in the mining, petroleum and quarrying industries show at label E the total amount of capital expenditure (other than on depreciating assets) claimed as an immediate deduction for:

-

Exploration and prospecting

-

Rehabilitation of mining or quarrying sites, and

-

Payment of petroleum resource rent tax.

Click label E to open the Generic Schedule / Worksheet.

For more information about these deductions, refer to the ATO publication Guide to depreciating assets.

Label H - Deduction for project pool

Click label H to open the Depreciation worksheet (d) to establish the project pool and keep track of the project amount.

Show at this label the total amount of the company's deductions for project pools.

Label I - Capital works deductions

Show at this label the deduction claimed for capital expenditure on buildings, which includes eligible capital expenditure on extensions, alterations or improvements. Exclude capital expenditure for mining infrastructure buildings and timber milling buildings.

Click label I to open the Capital works deductions worksheet (sbw). Integration from the Capital Works Deductions worksheet (sbw) is either directly to label I in the return or to a Rental Schedule you have prepared for this return.

If you choose to integrate to 'rent', a Rental schedule must already have been started for this return.

For more information on capital works deductions refer to Appendix 2 of the Company tax return instructions.

Commercial debt forgiveness provisions may affect the calculation of some deductions. Refer to Appendix 1 of the Company tax return instructions.

Label Z - Section 40-880 deduction

Show at this label the total of the company's deductions allowable under section 40-880 of the ITAA 1997.

Click label Z to open the Depreciation worksheet (d). To integrate to the Section 40-880 deduction from the Depreciation worksheet (d) choose the method of depreciation as Business related (S.40-880).

The expenditure deductible under section 40-880 must be shown at label W Non-deductible expenses item 7 to the extent that it has been included as an expense at item 6.

For information about section 40-880 deductions refer to Appendix 6 of the Company tax return instructions.

Label N - Landcare operations and deduction for decline in value of water facility, fencing asset and fodder storage asset

Show at label N the company's total deductions for landcare operations expenses and for water facilities, fencing assets and fodder storage assets.

Tax provides for amounts to be entered in the 3 fields preceding label N. These are not ATO fields but are required to ensure that integration from the various worksheets may occur.

Do NOT include the deduction for the decline in value of water facilities at label F Deduction for decline in value of depreciating assets at item 7.

To the extent that expenditure on landcare operations and water facilities, fencing assets and fodder storage assets has been included as an expense at item 6, it must be shown at label W Non-deductible expenses item 7.

For information about deductions for landcare operations and water facilities, fencing assets and fodder storage assets, refer to Appendix 6 of the Company tax return instructions.

Worksheets are available if required at each of the three data entry fields:

Landcare operations: Press Alt+S to open the Generic Schedule / Worksheet.

Landcare deduction from Partnership distributions: Press Alt+S to open the Distributions from partnerships worksheet (dip)

Water, fencing and fodder: Press Enter to open the Depreciation worksheet (d) and choose the method of depreciation Water facility or fencing or fodder storage.

Label O - Deduction for Environmental protection expenses

Show at this label the amount of allowable expenditure on environmental protection activities (EPA). You can deduct expenditure to the extent that the taxpayer incurred it for the sole or dominant purpose of carrying on EPA. EPA are activities undertaken to prevent, fight or remedy pollution or to treat, clean up, remove or store waste from the taxpayer’s earning activity.

Click label O to open the Generic Schedule / Worksheet.

To the extent that deductible expenditure on environmental protection activities has been included as an Expense at item 6, it must also be shown at label W Non-deductible expenses item 7.

For information about deductions for expenditure on environmental protection activities refer to Appendix 6 of the Company tax return instructions.

Label P - Offshore banking unit adjustment

Only use this label if the company has been declared to be an offshore banking unit (OBU) by the Treasurer under subsection 128AE(2) of the ITAA 1936. Otherwise disregard this label.

Click label P to open the Generic Schedule / Worksheet .

If you complete P, you must complete an International dealings schedule.

Subject to certain exceptions, an OBU is effectively taxed at the rate of 10% on income derived from offshore banking (OB) activities. In calculating an OBU's total income for the year, gross income from OB activities is shown at label R Other gross income item 6.

Total expenses from OB activities are shown at label S All other expenses item 6.

To get the effective 10% tax rate on OB activity income, section 121EG of the ITAA 1936 reduces the assessable income and allowable deductions from OB activities so that an OBU’s taxable income includes only the ‘eligible fraction’ (currently 10/ applicable company tax rate) of its net income from OB activities.

For information on the taxation of an OBU refer to Taxation Determinations TD 93/202 to 93/217, TD93/241, TD 95/1 and 95/2 and to the current year.

Label V - Exempt income

Show at this label all income that is exempt from Australian tax.

Click label V to open the Generic Schedule / Worksheet.

Do not include amounts that are not assessable income and not exempt income. For example any foreign income amounts that treated as non-assessable non-exempt income under section 23AH, 23AI, 23AJ, 23AK or 99B(2A) of the ITAA 1936. These amounts are shown at label Q Other income not included in assessable income item 7.

Do not include income exempt under an RSA. Exempt income from RSAs is taken into account in determining the net taxable income from RSAs at label V item 19.

Label Q - Other income not included in assessable income

Show at this label income related adjustments that have to be subtracted from label T Total profit or loss at item 6 to reconcile with label T Taxable Income or loss at item 7.

Do not include amounts already included at Item 7 labels C Section 46FA deductions for flow-on dividends to V Exempt income.

Generally the amounts that are included at label Q Other income not included in assessable income are income for accounting purposes but not assessable for income tax purposes.

Exempt income is shown separately at label V Exempt income item 7. For more information on specific items refer to the current year, see the ATO instructions.(worksheet 2).

Click label Q to open the Other Subtraction Items worksheet (sub). The total of the amounts entered into the fields at the top of the schedule under the heading Other Income not included in assessable income Label Q integrates to Label Q in the return.

Label W - TOFA Deductions from financial arrangements not included at item 6

If the company has financial arrangements to which the TOFA rules apply, include at this item:

-

Losses allowable under the TOFA rules from financial arrangements which have not been shown at item 6, and

-

The company's deductible transitional balancing adjustment for the income year

as a result of making the transitional election for existing financial arrangements.

There is a dissection worksheet available at the labels for dissection and record-keeping purposes. Click label W to open the Generic Schedule / Worksheet.

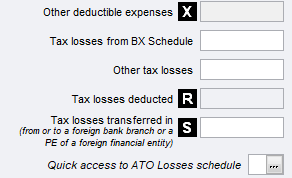

Label X - Other deductible expenses

Show at this label expense related adjustments that are subtracted from label T Total profit or loss at item 6 to reconcile with label T Taxable income or loss item 7.

Do not include amounts already included at item 7, labels C to P.

Generally label X Other deductible expenses shows amounts, including timing differences, that are an allowable deduction for income tax purposes but are not shown in the accounts or specifically shown at item 7, labels C to P.

Click label X to open the Other Subtraction Items worksheet (sub). The total of the amounts entered into the fields at the bottom of the schedule under the heading Other deductible expenses label X is passed to label X in the return.

For examples of specific items to be included and excluded. See Worksheet 2 of the current income year ATO Company instructions.

If the company is a life insurance company (LIC), include at label X Other deductible expenses the deduction it is entitled to if it receives a dividend from a LIC which includes a LIC capital gain amount. Refer to Item 16 - Life insurance companies and friendly societies only. Other companies are not entitled to this deduction.

Label R - Tax losses deducted

On 1 March 2019, legislation was enacted that will supplement the current ‘same business test’ for company losses with a more flexible 'similar business test'. See:

The new test will expand access to past year losses when businesses enter into new transactions or business activities.

Completing the fields that make up label R

In AE/AO you can't enter an amount directly at the label in the income tax return.

Separate fields are provided for companies and Head companies of a consolidated group.

If you've completed the Consolidated Groups Losses Schedule (bx), the amount we've passed that amount to this field.

Otherwise, to open the BX, press Alt+S.

Non-consolidated companies—Other Tax losses press Alt+S to open the Prior year losses worksheet (pyl) where you can manage your company prior year losses from year to year.

Show at this field only those tax losses of a prior income year that are deducted in respect of current income year under section 36-17 of the ITAA 1997. This includes any deductions for foreign losses converted to tax losses under Subdivision 770-A of the Income Tax (Transitional Provisions) Act 1997.

Subject to various rules, prior year tax losses are deducted in respect of a later income year or years in the order in which they were incurred-to the extent that they have not already been deducted

A quick access point to the Losses schedule (BP) is provided after label S. Selecting Y at the quick access to Tax Office Losses Schedule opens the:

-

Consolidated Losses schedule (BX), or

-

Losses schedule (BP)

depending on the selection you've made at item 3 label Z Consolidated group status.

Label S - Tax Losses transferred in (from or to a foreign bank branch or a PE of a foreign financial entity)

Show at label S the amount of tax losses transferred to the company from group companies under Subdivision 170-A of the ITAA 1997.

A Generic Schedule / Worksheet is provided for dissection purposes.

Consolidated or MEC groups

Do not show tax losses transferred from subsidiary companies under Subdivision 707-A of the ITAA 1997. These losses should be shown in Part A items 1 or 2 of the Consolidated groups losses schedule.