The ATO has decommissioned the payment summary schedule (PS) for individual returns and introduced a new schedule Business income statements and payment summaries (bip).

For ATO information on these income labels click the links to item P8 that are provided to take you to the ATO website. You may then need to expand the list in the left-hand panel and expand the list under Income, then click the label you require.

For former STS taxpayers, click this link for information on Concessions for small business entities on the ATO website.

Income

Expenses

See Business and professional item P8 Expenses on the ATO website for further information.

For ATO information on these expense labels click the links to item P8 that are provided to take you to the ATO website. You may then need to expand the list in the left hand panel, then expand the list of Expenses and click the exact label you require.

Reconciliation items

Use the Tax Reconciliation worksheet (Schedule A) to enter all income and Expense add backs and subtractions. The Reconciliation worksheet presents a comprehensive set of fields to enter adjusting amounts between accounting income and taxable income. Click Alt+S at any reconciliation item to open the Reconciliation worksheet (Schedule A). Refer to Schedule A Reconciliation.

See Business and professional item P8 Reconciliation items on the ATO website for further information.

Reconciliation adjustment labels

|

Label |

ATO Information |

|---|---|

|

Label A: Section 40-880 deduction |

|

|

Label L: Business deduction for project pool |

|

|

Label W: Landcare operations and business deduction for decline in value of water facility, asset and fodder storage asset |

See Landcare operation and business deductions for decline in value of water facility. |

|

Labels X and H: Income and Expense reconciliation adjustments |

|

|

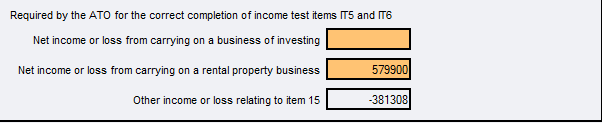

Dissection of net income/loss for ATI purposes |

The field in the MYOB Tax box is required to help the ATO in calculating Adjusted taxable income (ATI) or Rebate income (RI) for offset and certain credit purposes. |