Did you receive any New Zealand interest between 1 April 2018 and 31 March 2019 from:

-

banks

-

Inland Revenue

-

building and investment societies

-

credit unions

-

securities

-

a partnership, look-through company, estate or trust

-

loans you’ve made?

If so, show all the New Zealand interest you received at Question 13B. If the interest is from a partnership, look-through company, estate or trust please tick Box 13C.

If you were charged commission on any of your interest, claim this at Question 26. Read the note about expenses at IR Schedules Other expenses and deductions.

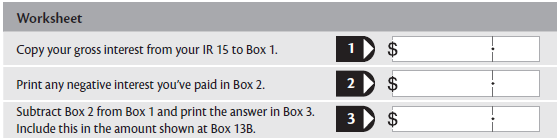

Interest on broken term deposits

If you’ve broken a term deposit during the year, you may have “negative interest” to account for. This is interest you’ve repaid on the term deposit. It may reduce the amount of interest you need to declare on your tax return.

If you broke the term deposit in full, use the worksheet below to deduct the negative interest from the gross interest amount shown on your Deduction certificate for RWT on interest (IR15) or equivalent statement. In all other cases, the negative interest is deductible in a later tax return when the term deposit matures.