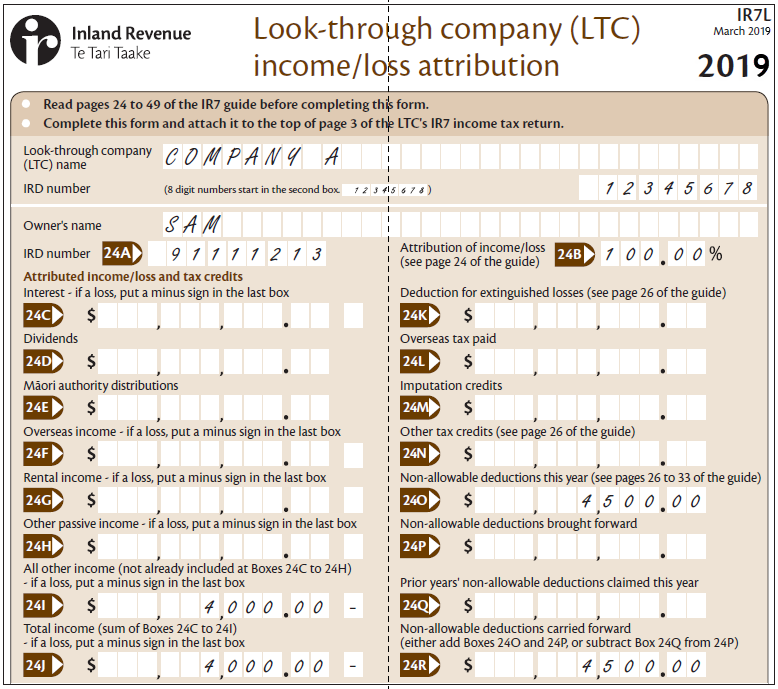

The following details are for Company A which is an LTC:

|

IRD number |

12–345–678 |

|

Total gross income |

$6,000 |

|

Expenses/deductions |

$10,000 |

|

Loss |

$4,000 |

|

One owner (shareholder): |

Sam (100%) |

|

IRD number |

91–111–213 |

|

Sam’s owner’s basis |

$5,500.00 |

Company A is in a partnership with another LTC.

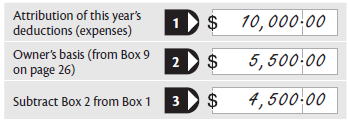

Calculate the non-allowable deductions for Sam:

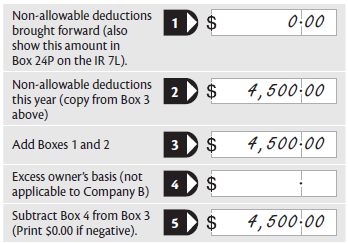

Box 3 is Sam’s non-allowable deductions this year. The amount in Box 3 ($4,500) is shown at Box 24O.

Box 5 is Sam’s non-allowable deductions to carry forward. The amount in Box 5 ($4,500) is shown at Box 24R.

Company A’s IR7L would look like this:

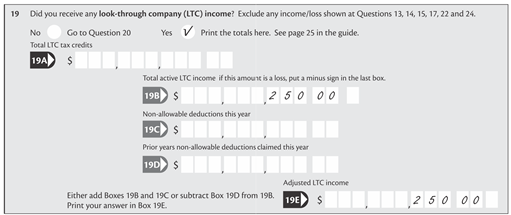

Sam’s Individual income tax return (IR3) Question 19 would look like this:

Sam’s adjusted LTC income is in effect calculated by subtracting his allowable deductions ($5,500) from Company A’s gross income ($6,000) = $500.