If the LTC received income from another LTC, write the details at Question 15.

A partnership does not receive income or deductions from an LTC. If two or more people jointly receive income or deductions from an LTC, they should show these on their own returns, not the partnership’s return.

LTCs are transparent (looked through), meaning the owners are treated as having received the income and incurred the loss of the company.

The LTC will normally supply the information required to complete your return.

Don’t include any of the following types of income received from another LTC at Question 15:

-

interest and RWT—show these at Question 11

-

dividends, imputation credits, and dividend RWT—show these at Question 12

-

Maori authority distributions and credits—show these at Question 13

-

overseas income and any credits attached—show these at Question 16, see IR7 Question 16 Overseas income

-

rental income—show this at Question 18, see IR7 Question 18 Rental income

-

other income—show this at Question 19, see IR7 Question 19 Other income.

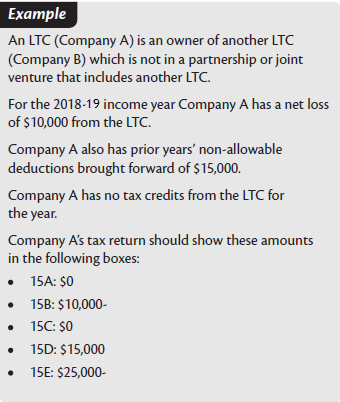

Change to the loss limitation rule

Before the 2018-2019 income year the amount of deductions an LTC owner (shareholder) could claim was subject to the loss limitation rule.

This rule limits the amount of deductions an owner can claim to the amount of their “owner’s basis”, which represents their economic interest in the LTC.

The loss limitation rule no longer applies to most LTC owners. It continues to apply for owners of LTCs that are in a partnership or joint venture that includes another LTC.

If the loss limitation rule no longer applies, any deductions which have been carried forward will be claimable this year. The example below explains how the tax return should be completed where this applies.