Assets performs depreciation calculations for both Tax and Accounting purposes. It's up to you as to whether you want to calculate depreciation for Tax only, Accounting only or both.

If you choose to calculate depreciation for both methods, you can choose which calculation you'd like to post depreciation journals for. These settings are saved for subsequent years so you'll only need to revisit these tasks where a change is required.

Tax vs. Accounting depreciation

If you've been using the Fixed Assets module in AO Classic or another asset tracking software, you may not have had to differentiate between Tax and Accounting depreciation.

In Australia, these tax rules are often the cause of difference when comparing Tax and Accounting depreciation for an asset with the same opening written down value and depreciation rate. For example:

-

In a leap year (e.g. 2012, 2016 and 2020), assets held for a full year are calculated for tax purposes at 366 days held over 365 days in a year. The same assets held for a full year are calculated for accounting purposes at 365 days held over 365 days in a year.

-

Motor vehicles may be subject to the Depreciation Cost Limit when calculating depreciation for tax purposes, however, the depreciation cost limit is not applied in the calculation for accounting purposes.

Keeping an assets register for accounting purposes can also help you keep track of the actual value of your fixed assets. Although the ATO or IRD perceive an asset to be "written-off", your client may still hold the asset which may still be worth something.

Setting up the register

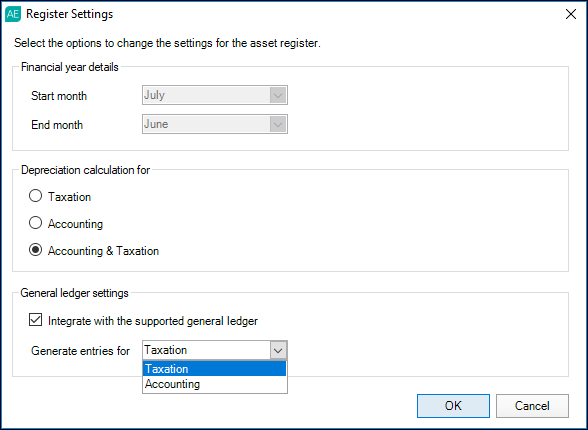

1. Specify your Asset Register settings

-

Click the Client Accounting > Asset tab.

-

On the TASKS bar, click Register settings.

-

In the Register Settings window in the Depreciation calculation for section, select the depreciation calculation type to be used:

-

Taxation only

-

Accounting only

-

Accounting and Taxation

-

-

If you wish to integrate the Asset Register with the supported general ledger, select the Integrate with the supported general ledger checkbox.

If you previously used the Asset Register without general ledger integration, the Integrate with the supported general ledger checkbox is not available.

-

If you have selected Accounting &Taxation under the Depreciation calculator for header, from the Generate entries for drop-down menu, choose what entries will be generated from depreciation calculations where:

Calculation type

then...

Taxation only

Depreciation calculations will generate taxation entries automatically

Accounting only

Depreciation calculations will generate accounting entries automatically

Accounting and Taxation

Select depreciation journals you want to be posted back into Trial balance view or Workpaper Period from either Accounting or Taxation.

-

-

Click OK. Changes are saved to the Asset Register and the Register Settings window closes.

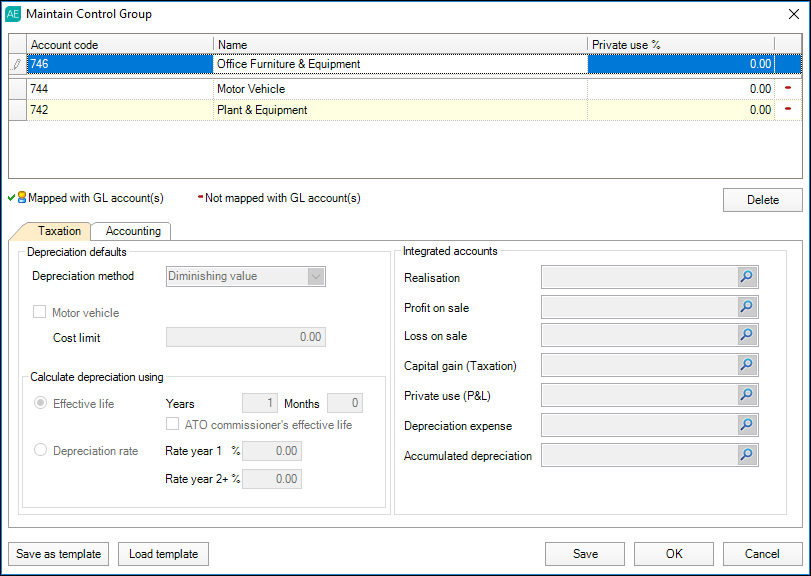

2. Add your Control Groups and integration accounts

-

From the Client Accounting > Assets tab, click Maintain control group on the TASKS bar.

-

In the Maintain Control Group window, click the first cell of the Account code column and enter the account code of the control group in the Account code cell.

-

Enter a control group name of up to 50 alphanumeric characters in the Name field. This field cannot be blank.

If you have selected Integrate with the supported general ledger when specifying your asset register settings, the Name field automatically displays the account name.

-

Enter a percentage between 0 and 100% for the group in the Private use % field.

-

Press Enter on your keyboard. The control group moves from the entry line to the table and the Taxation and Accounting tabs become available for input according to the configuration of the Asset Register.

-

On the Taxation and the Accounting tabs, fill in the following fields:

-

From the Depreciation defaults section, select the appropriate Depreciation method:

For the calculation type...

Select from the following

Taxation

-

Diminishing value

-

Immediate write-off

-

Prime cost

Accounting

-

Diminishing value

-

Exempt from depreciation

-

Immediate write-off

-

Prime cost

-

Straight line

If applicable, you can tick the Motor vehicle checkbox to apply the ATO cost limit to all motor vehicles allocated to the control group. This is best if you have purchased multiple motor vehicles in the same financial year. You can look up the cost limit on the ATO website: Car cost limit for depreciation.

-

-

Select your Calculate depreciation using preferences from the following options:

Field

Description

Effective Life (Taxation)

The depreciation rate is calculated based on the years and months entered. If applicable, tick the ATO commissioner's effective life checkbox.

Useful Life (Accounting)

The depreciation rate is calculated based on the useful life in years entered. Useful life is enabled only when the straight line method has been chosen.

Depreciation Rate

When this option is selected, the depreciation is calculated based on the rate that you enter in the Rate year 1 and Rate year 2+ fields.

-

In the Integrated accounts section, select or enter account codes to post journals for each of the following:

-

Realisation

-

Profit on Sale

-

Loss on Sale

-

Private use (must be a Profit and Loss account)

-

Depreciation expense

-

Accumulated depreciation

Account fields can be left blank, however, when posting journals to the general ledger, if an integrated account field has been left blank the journal may not be posted.

If you have mapped the integrated accounts with a configured and supported general ledger, the Mapped with GL account(s) icon (

-

-

-

Click Save. The Maintain Control Group window remains open.

Did you know? You can save your control group as a template to be re-used on another client or at a later date.

To save your control group as a template, click the Save as template button located on the bottom left of the Maintain Control Group window. Learn more about

Control group templates.

-

To create another control group, click the next cell of the Account code column and go step 4. Otherwise, click Close to exit the Maintain Control Group window.

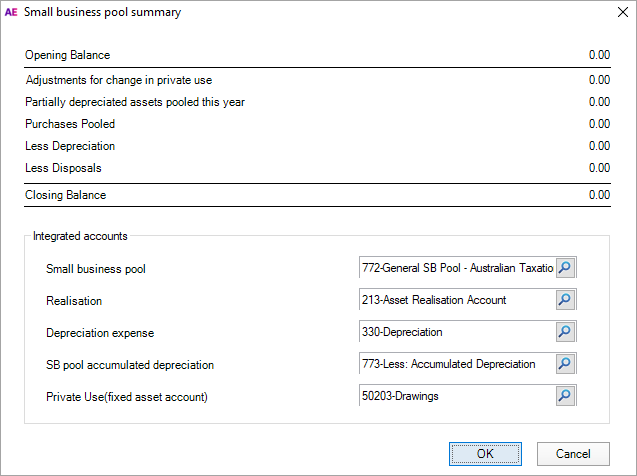

3. Set up a Small business or Low value pool (Optional, AU only)

This is applicable to Australia only. If you're in NZ, you can skip this task.

-

From your client's Client Accounting > Assets tab, double-click on an asset year to open the register.

-

From the TASKS bar, click Small business pool to create a small business pool or, Low value pool to create a low-value pool.

-

In the Integrated accounts section, select or enter account codes to post journals to.

-

When all integrated accounts have been chosen, click OK to save your changes and close the window.

Pick your path

The next task depends on whether you have moved your existing data or created a new, blank register. Click on the button below that relates to your situation.

![]()