You're here to find out how to apply the different depreciation incentives in MYOB Tax.

The order of applying the depreciation, if more than one incentive applies:

-

Temporary full expensing (TFE)

-

Instant asset write-off (IAWO)

-

Backing business investment (BBI)

-

General depreciation rules

Based on the rules and thresholds, we've made changes to the depreciation worksheet to help you choose the correct threshold.

Small business using simplified depreciation rules

To apply TFE

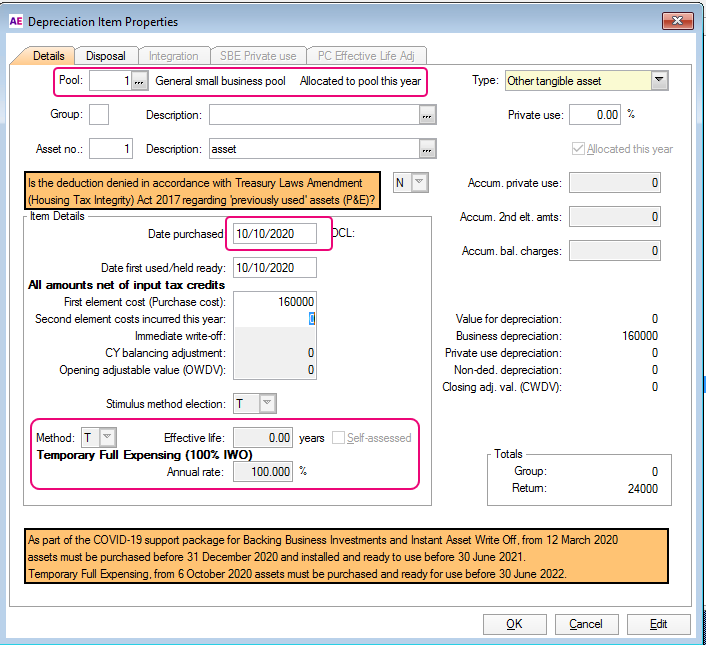

If you're an SBE using simplified depreciation rules, you must use TFE if the asset is first used/held on or after 6 October 2020.

To apply TFE

-

Select Y at the SBE Eligibility tests.

-

In the depreciation worksheet, TFE method will apply automatically if:

-

-

the asset is added to the general small business pool,

-

date purchased is on or after 6 October 2020.

-

There is no threshold limit to apply TFE.

To apply BBI or Instant write off

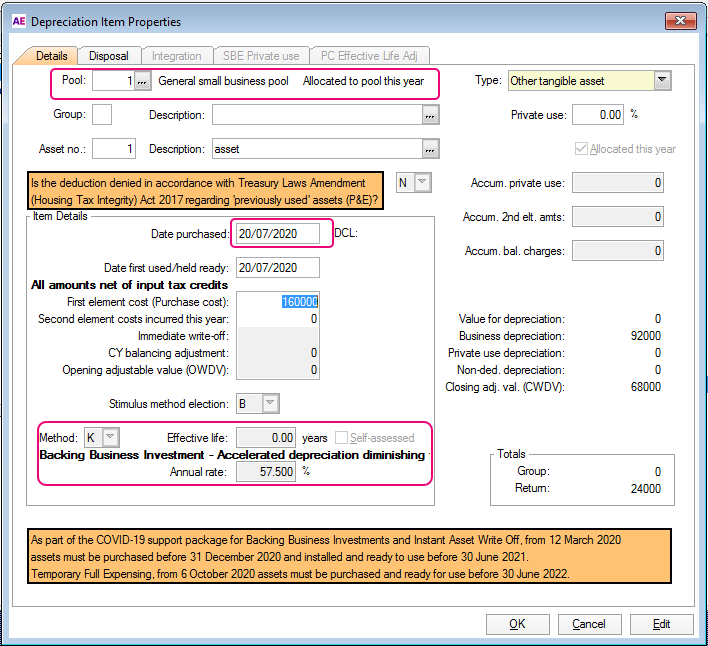

If you're an SBE using simplified depreciation rules, you can use:

-

instant write off (IAWO) rules to depreciate the asset at 100%

-

Backing business investment rules (BBI) to depreciate the asset at 57.5%.

To apply Instant write off method

-

Select Y at the SBE Eligibility tests.

-

In the depreciation worksheet, the Instant write off (IAWO) method will apply automatically to a pooled asset if the following date and thresholds conditions are met:

|

Date when the asset was used or installed |

Threshold |

|---|---|

|

11 March 2020 and prior |

$30,000 |

|

12 March 2020 to 5 October 2020 |

$150,000 |

To apply Backing business investment (BBI) method

-

Select Y at the SBE Eligibility tests.

-

In the depreciation worksheet, the Instant write off (IAWO) method will apply automatically to a pooled asset:

Date when the asset was used or installed

Depreciation rate

12 March 2020 to 30 June 2020

30%

01 July 2020 to 5 October 2020

57.5%

Small business not using simplified depreciation rules

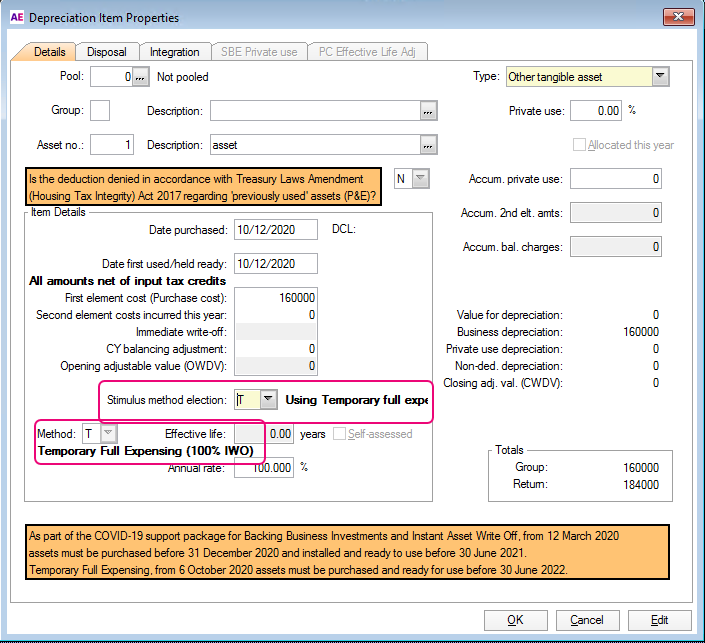

To apply TFE

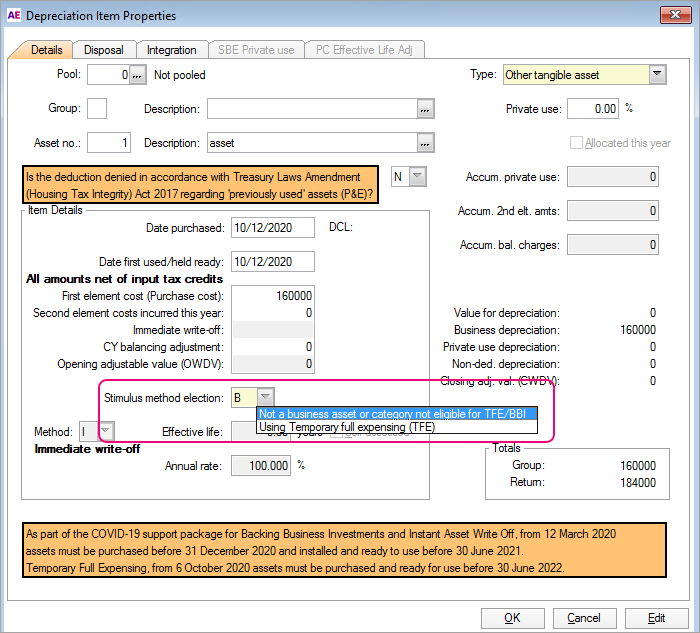

If you're an SBE not using simplified depreciation rules, you can choose to use TFE if the asset is first used/held on or after 6 October 2020.

We've added new fields to choose from under the stimulus method election:

-

Code N: Not a business asset or category not eligible for TFE/BBI

-

Code T: Using Temporary Full Expensing.

Depending on what code you chose, the methods will differ accordingly.

|

Stimulus Method election |

Methods available |

|---|---|

|

Code N: Not a business asset or category not eligible for TFE/BBI |

|

|

Code T: Using Temporary Full Expensing |

|

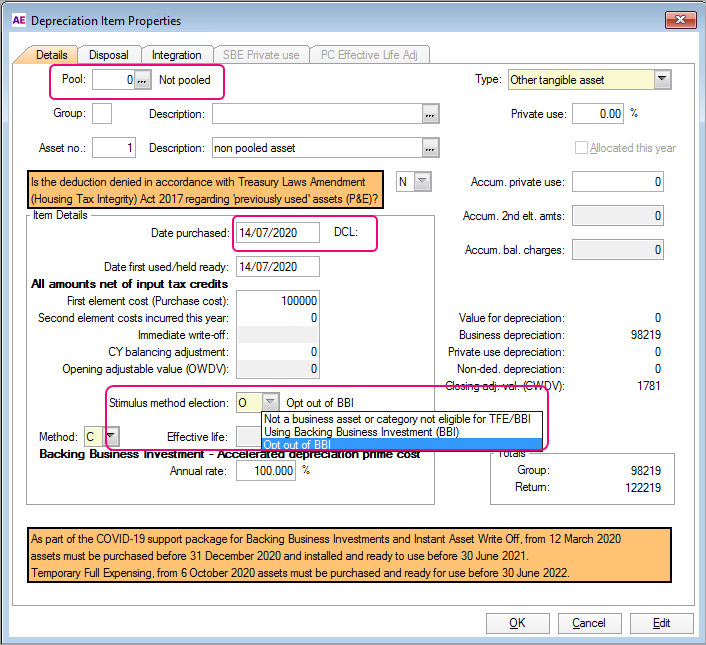

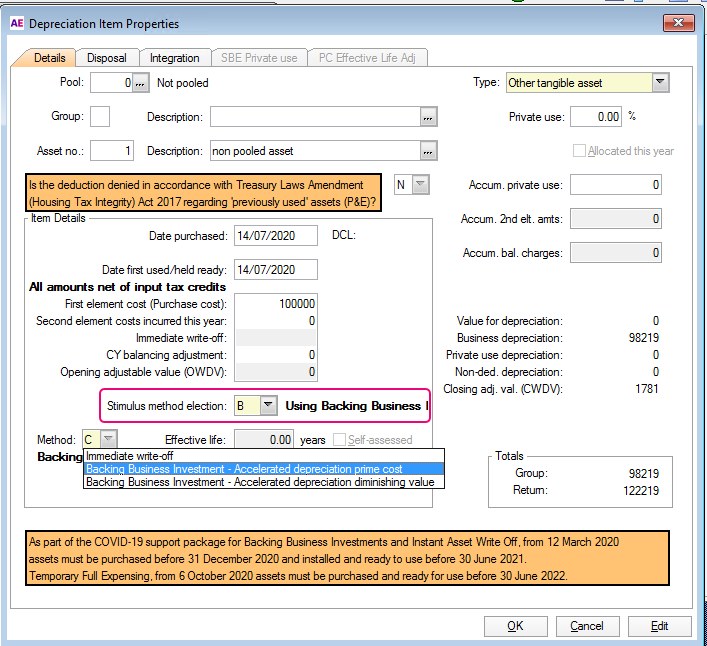

To apply BBI or Instant write off

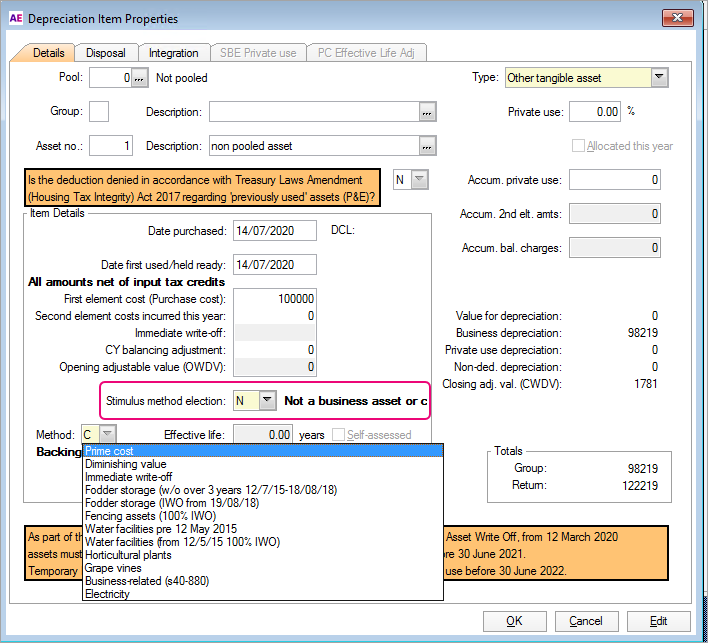

If an asset is not added to the pool, you may choose Backing Business investment depreciation rules for the asset.

We've added new fields to choose from under the stimulus method election:

-

Code N: Not a business asset or category not eligible for TFE/BBI

-

Code B: Using Backing business investment (BBI)

-

Code O: Opt out of BBI

Depending on what code you chose, the methods will differ accordingly.

|

Stimulus Method election |

Methods available |

|---|---|

|

Code N: Not a business asset or category not eligible for TFE/BBI or Code O: Opt out of BBI |

|

|

Code B: Using Backing business investment (BBI) |

|

Reference

Depreciation table

|

Business type |

Aggregated turnover |

Temporary full expensing

|

Instant asset write-off

|

Instant asset write-off

|

Backing business investment

|

|---|---|---|---|---|---|

|

Small business (SBE) |

Less than $10m |

|

|

|

|

|

Small business

|

Less than $10m |

|

|

|

|

|

Medium business |

$10m to less than $50m |

|

|

|

|

|

Medium to large business |

$50m to less than $500m |

|

|

|

|

|

Large business |

$500m to less than $5bn or using Alternative income test |

|

|

|

|