Key point

There is often a crossover between personal and business use of goods and services. You need to adjust your GST return to reflect this.

In some instances, you may need to calculate a GST adjustment to either pay GST, for example, for a business asset used privately, or claim back GST that’s already been paid, for example, for a private asset used for business. See part 4 of this guide.

You may also need to make adjustments for certain late claims and credit or debit notes that include GST at the old rate of 12.5%.

For other adjustments, you’ll need to work out the private or exempt portion of various income and expenses.

Many small businesses get help from their accountant/tax agent for adjustments. If you don’t have an accountant/tax agent, see page 25 for more information, go to www.ird.govt.nz/gst or call Inland Revenue on 0800 377 776.

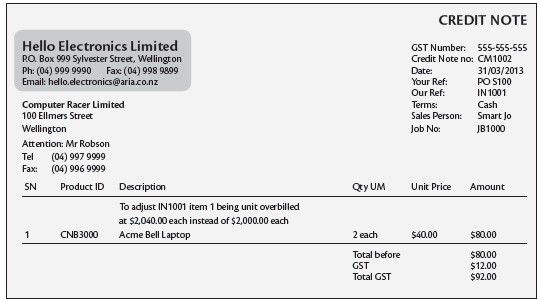

Credit and debit notes

You may have to include credit and debit notes in your calculations when you’re making an adjustment.

-

Credit notes are issued when the price of a supply has reduced after a tax invoice was issued, for example, the return of faulty goods.

-

Debit notes are issued when the price increases after a tax invoice has been issued.

Example