You can calculate your IETC:

-

by using the worksheets provided in this section

-

by calling the Inland Revenue self-service line.

IETC

The IETC is a tax credit for individuals whose annual net income* is between $24,000 and $48,000. Your annual net income is shown at Box 27 “Income after expenses” in your return.

* Net income means your total income from all sources, less any allowable deductions or current year losses (not including any losses brought forward).

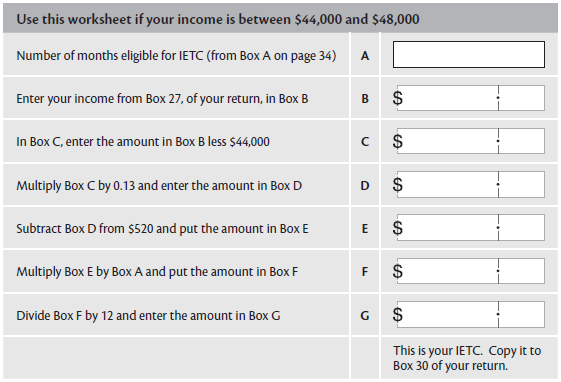

If you’re eligible for IETC, but earn over $44,000, your annual entitlement to IETC decreases by 13 cents for every dollar earned above $44,000.

For the period 1 April 2018 to 31 March 2019, you’ll be entitled to IETC for any months:

-

you were a New Zealand tax resident

-

you or your partner weren’t entitled to Working for Families Tax Credits (or received an overseas equivalent) and you didn’t receive:

-

an income-tested benefit

-

NZ Super

-

a veteran’s pension or

-

an overseas equivalent of any of the above.

You’re a tax resident if you lived in New Zealand for more than 183 days in the last twelve months, or have a permanent place of abode in New Zealand. For more information, read the guide New Zealand tax residence (IR292).

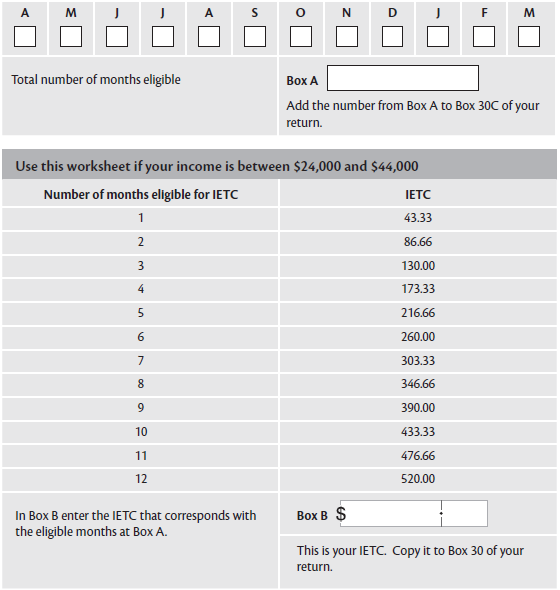

To work out the months you’re entitled to this tax credit, use the total number of whole months the criteria applied to.

If you didn’t meet the above criteria for even one day of any month you won’t be entitled to IETC at all for that month, so don’t include it in your calculation.

Calculating your IETC

Enter the start and end dates when you had any overseas income that excludes you from being eligible for IETC at Box 30B on your return.

If the overseas income continued past the end of the year enter the end date for the income as 31/03/2019.

If you have more than one date range for the overseas excluded income, attach a note telling Inland Revenue of the date ranges. You’ll also need to include any dates you weren’t a New Zealand tax resident.

Tick the boxes below for each month (between 1 April 2018 and 31 March 2019) you were entitled to the IETC for the full month.