Did you receive any New Zealand interest between 1 April 2018 and 31 March 2019:

-

in cash or by cheque

-

credited or added to your account

-

compounded and added to your investment

-

earned by a partnership, estate or trust, or from Inland Revenue?

You must show all New Zealand interest you receive. Include interest from banks, building and investment societies, credit unions, other securities and any loans you’ve made. Also include interest from Inland Revenue.

Don’t include any interest that has:

-

had NRWT deducted at the correct rate

-

been zero-rated under the approved issuer levy rules (AIL). See Approved issuer levy (AIL) for details.

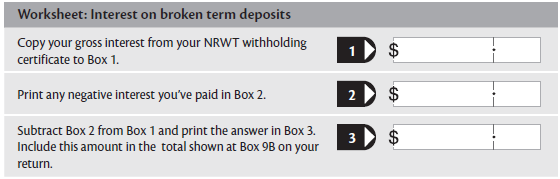

Interest on broken term deposits

If you’ve broken a term deposit during the year, you may have negative interest to account for. This is interest you’ve repaid on the term deposit. It may reduce the amount of interest you need to declare on your return.

If you broke the term deposit in full, or it was business-related, deduct the negative interest from the gross interest amount on your New Zealand NRWT withholding certificate (IR67). Deduct the allowable negative interest component using the worksheet below before entering the gross amount at Question 9B.

What to show in your return

The interest payer will send you a statement or an New Zealand NRWT withholding certificate (IR67). It will show the gross interest paid and the amount of tax deducted.

From each interest statement or certificate, copy the name of the payer, add up the amounts of tax deducted and the gross interest and print the totals in the boxes at Question 9.

Don’t send Inland Revenue your interest statements or certificates, but keep them in case they ask for them later.