Interest from all New Zealand sources must be shown in the return. Write the total of all RWT deducted in Box 13A. If the company has had NRWT deducted from New Zealand interest, include this in Box 13A. Add up all the gross interest amounts (before the deduction of any tax) and write the total in Box 13B.

Interest on broken term deposits

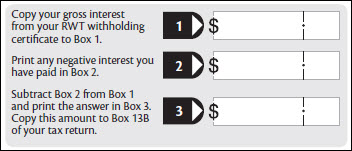

If you have broken a term deposit during the year, you may have to account for “negative interest”. This is interest repaid on the term deposit and may reduce the amount of interest to declare on the tax return.

If the term deposit was broken in full, or it was business-related, deduct the negative interest from the gross interest amount shown on the RWT withholding certificate (IR15 or equivalent statement).

Deduct the allowable negative interest part, using the worksheet below, before entering the gross amount at Question 13 of the tax return. In all other cases, the negative interest is deductible in a later tax return when the term deposit matures.

Worksheet