Generally, dividends are taxable. However, there is an exemption for dividends paid between members of a wholly owned group.

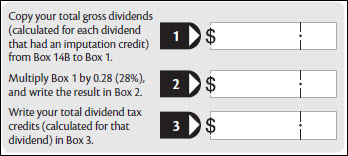

To work out the total gross dividends, add up all net dividends received, any imputation credits, and any RWT deductions. Write the total of all dividends in Box 14B.

The FDP rules have been fully repealed from 1 April 2017. Don’t include any FDP credits in box 14A.

Dividend tax credits

The total tax credits for dividends (such as imputation credits and FDP credits) you can claim is limited to the income tax payable (28%) on each dividend the company receives. This is to ensure that surplus tax credits are not used to shelter tax on other income.

Work out whether you need to apply this limitation to the dividend tax credits you will claim.

For each dividend, claim a dividend tax credit for the lower amount shown in Box 2 or Box 3.

Write the total dividend imputation credits you are allowed to claim in Box 14.

In Box 14A write the sum of your total dividend RWT credits you are allowed to claim.

If expenses are deductible against the dividend income, claim them at Box 19B.

Unit trusts

Distributions from unit trusts will generally be taxable. The statement you receive from the unit trust should show the amounts to include in the return.

Transfer of deductible expenses between member and master funds

From the 2002–03 income year a member fund may, in certain circumstances, elect to transfer deductible expenses to a master fund. The master fund must invest, in whole or in part, in the member fund. The master fund can then deduct the transferred expenses.

A member fund can include a group investment fund that derives Category A income, a public unit trust or a superannuation fund. A master fund can include a group investment fund that derives Category A income or a public unit trust.

A public unit trust includes:

retail unit trusts, whose units are offered to the public and which have 100 or more unit holders

wholesale unit trusts, whose units are held by widely held investment vehicles such as other unit trusts or superannuation funds.

Member or master funds wanting to take advantage of this provision should include details of the adjustment in a tax reconciliation statement accompanying the return. The information should accompany the returns of both funds involved in the transfer.

For more information see the Tax Information Bulletin (TIB) Vol 13, No 11 (November 2001).

Qualifying companies

Generally, if a qualifying company is a shareholder in a company that isn’t a qualifying company, all dividends the qualifying company derives from the other company are taxable.

Dividends derived by a company (that has been a qualifying company at any time before deriving the dividends) are taxable.

If a qualifying company is a shareholder in another qualifying company, only dividends with imputation credits attached and a return of a 10-year bonus issue before the 10-year period expires, are taxable. Dividends with no imputation credits attached, or a return of a 10-year bonus issue 10 years from the payment date, are exempt income.

A distribution of a 10-year bonus issue before the 10-year period has expired, made when the company winds up, isn’t taxable.

If you need more help, read the guide Qualifying companies (IR435).

Don’t send in the dividend statements with the return, but keep them in case Inland Revenue ask for them.