2019 provisional tax is charged for income the estate or trust will earn in the 2020 income year. It is payable in two, three or six equal instalments. There are three options for paying provisional tax—standard, estimation and ratio.

If the estate or trust’s 2019 RIT is:

-

$2,500 or less it doesn’t have to pay provisional tax, although it can make voluntary payments

-

more than $2,500 but expected to be $2,500 or less for 2019, it may estimate 2020 provisional tax at nil (read IR6 Question 29 2020 provisional tax | IR6Question292020provisionaltax Estimationoption.)

-

more than $2,500 and expected to be more than $2,500 for 2019, it must pay 2020 provisional tax.

If you anticipate your RIT will exceed $2,500 for the 2020 year, see IR6 Question 29 2020 provisional tax | IR6Question292020provisionaltax Interest. You may be liable for interest from your first provisional tax instalment date.

Which option to use

Estates or trusts can use either the standard or estimation options to pay their provisional tax. If they’re registered for GST they may also be able to use the ratio option.

Estimating provisional tax on beneficiary income

When working out the tax on estimated beneficiary income, calculate the tax separately for each beneficiary, including estimated tax credits where applicable. The table below shows the 2020 individual tax rates for provisional tax.

|

2020 annual tax rates income range |

Tax rate |

|---|---|

|

Income to $22,000 |

10.5% |

|

$22,001 – $52,000 |

17.5% |

|

$52,001 – $70,000 |

30.0% |

|

$70,001 and over |

33.0% |

When using these tax rates to calculate 2020 provisional tax, you’ll also need to estimate the tax credits the beneficiary may be entitled to.

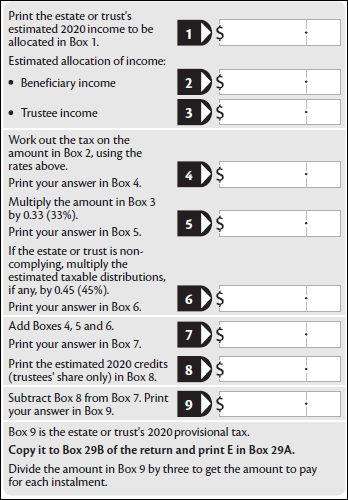

Use this worksheet to calculate the estate or trust’s 2020 provisional tax using the estimation option.

If you need more help read the guide Provisional tax (IR289).

Not taking reasonable care penalty

When you estimate the estate or trust’s 2020 provisional tax, your estimate must be fair and reasonable. If the 2020 RIT is greater than the provisional tax paid, you may be liable for a not taking reasonable care penalty of 20% of the underpaid provisional tax.

Interest

If the estate or trust has paid too much provisional tax on trustee income Inland Revenue may pay interest, or if it hasn’t paid enough, Inland Revenue may charge interest.

Interest for estates or trusts is calculated only on the tax payable on trustee income. Interest isn’t calculated if all income is distributed to the beneficiaries.

Interest the estate or trust pays is generally tax-deductible, while interest Inland Revenue pay is taxable income.

For more information about interest and penalties read the guide Penalties and interest (IR240).

If Inland Revenue pay interest, it continues to accrue until the date they refund the overpaid tax, or apply it to another liability.

Election to be a provisional tax payer

An estate or trust is a provisional tax payer for the 2020 year if its RIT for 2019 is more than $2,500. If the 2019 RIT is $2,500 or less, and:

-

the estate or trust made provisional tax payments for that year, and

-

payments were made under the estimation method (other than using the estimation method for its final instalment only).

It may elect to be a provisional tax payer for 2020. This may affect the interest it may be entitled to for that year.

To elect to be a provisional tax payer for the 2020 year, attach a letter to the front of the return.

Change in balance date

There are special rules about when provisional tax is due and how interest is calculated if there has been a change in balance date. Read the Provisional tax (IR289) guide for more information.

Tax pooling

Tax pooling allows taxpayers to pool provisional tax payments, offsetting underpayments by overpayments within the same pool. This reduces their possible exposure to late payment penalties and use-of-money interest. The pooling arrangement is made through a commercial intermediary, who arranges for participating taxpayers to be charged or compensated for the offset. For more information about tax pooling, including a list of intermediaries, go to www.ird.govt.nz (search keywords: tax pooling).

Payment dates

2020 provisional tax

Generally, an estate or trust with a 31 March balance date pays provisional tax by the following due dates:

|

First instalment |

28 August 2019 |

|

Second instalment |

15 January 2020 |

|

Third instalment |

7 May 2020 |

An estate or trust with a balance date other than 31 March pays provisional tax on the 28th day of the 5th, 9th and 13th months after the balance date.

Where payments would otherwise be due on 28 December or 28 April the due date is extended to 15 January or 7 May.

These dates will alter if:

-

the estate or trust is registered for GST, and

-

the GST filing frequency is six-monthly, or

-

provisional tax is paid by the ratio option.

If either of these situations apply to you, read the guide Provisional tax (IR289).

2019 end-of-year income tax

Estates or trusts that have an agent and an extension of time may have until 7 April 2020 to pay their tax. If you think this applies to you contact your agent for more information.

Otherwise, an estate or trust with a balance date between 1 March and 30 September must pay its end-of-year income tax and any interest by 7 February 2020.

An estate or trust with a balance date between 1 October and 28 February must pay its end-of-year income tax by the 7th day of the month before the following year’s balance date.