Include interest from all New Zealand sources at Question 9.

The interest payer will usually send you an RWT withholding certificate (IR15), or similar statement, showing the gross interest paid and the amount of RWT deducted.

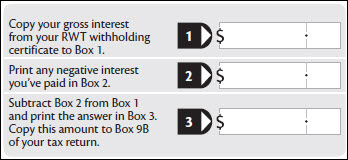

Write the total of all RWT deducted in Box 9A.

Add up all the gross interest amounts (before the deduction of any tax) and write the total in Box 9B.

If expenses are deductible against the interest income (for example, commission), claim them at Question 19. Read about expenses at IR6 Question 19 Expenses.

Don’t send in any interest statements or IR15 certificates with your return, but keep them in case Inland Revenue ask for them later.

Interest on broken term deposits

If you’ve broken a term deposit during the year, you may have to account for “negative interest”. This is interest repaid on a term deposit and may reduce the amount of interest to declare in your return.

If the term deposit was broken in full, or it was business related, deduct the negative interest from the gross interest shown on the IR15 or equivalent statement.

Deduct the allowable negative interest component, using the worksheet below, before entering the gross amount at Box 9B on your return. In all other cases, the negative interest is deductible in a future income year when the term deposit matures.

Worksheet

Interest paid or charged by Inland Revenue

If Inland Revenue paid you interest, include it in Box 9B for the income year the trust received the interest.

If the trust paid Inland Revenue interest, include it as a deduction in Box 19 of the return for the income year the interest is paid.

Interest from overseas

If the trust received interest from overseas, convert your overseas interest and tax credits to New Zealand dollars and show the amounts at Question 13. Please read the notes about overseas income at IR6 Question 13 Overseas income.

Income from financial arrangements

The financial arrangement rules generally require income or expenditure from financial arrangements to be spread over the term of the arrangement. Financial arrangements include term deposits, government stock, local authority stock, mortgage bonds, futures contracts and deferred property settlements.

Trustees are required to use a spreading method unless they are a cash basis person.

A person is a cash basis person if:

-

the value of all financial arrangements together is less than $1 million, or

-

the value of the income or expenditure from the financial arrangement is less than $100,000, and

-

the deferral of income or expenditure using the cash method rather than the actual method is less than $40,000.

A special rule applies for deceased persons. If the deceased person was a cash basis person at the date of death, the concession applies in the year of death and up to four succeeding years.

Any RWT from a financial arrangement will be deducted on a cash basis.

Different rules apply for financial arrangements entered into prior to 20 May 1999.

Sale or maturity of financial arrangements

Whether or not the exemption from the spreading methods explained earlier applies, when a financial arrangement matures or is sold, remitted, or transferred, a “wash-up” calculation known as a base-price adjustment must be carried out.

Cash basis persons can use the Sale or disposal of financial arrangements (IR3K) to perform the calculation. This form could be used, for example, to calculate the amount you need to account for if you have broken a term deposit in full.

For further information about the financial arrangements rules, please see Tax Information Bulletin (TIB) Vol 11, No 6 (July 1999), page 3.

Any RWT will be deducted on a cash basis.