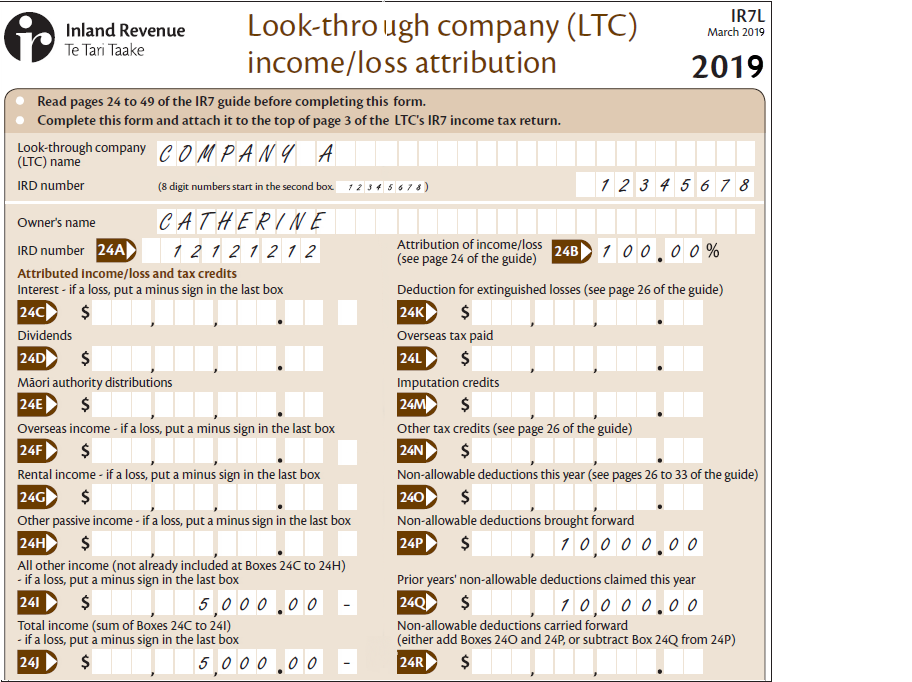

The following details are for Catherine who owns all of the shares in Company A, an LTC:

|

IRD number |

12–121–212 |

|

Total gross income |

$10,000 |

|

Expenses/deductions |

$15,000 |

|

Loss |

$5,000 |

|

Non-allowable deductions brought forward |

$10,000 |

Company A’s IR7L would look like this:

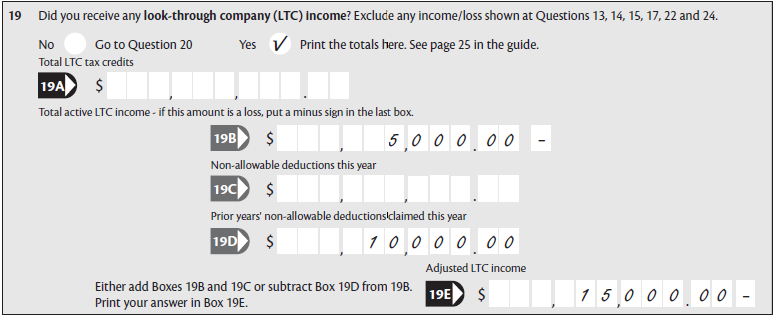

Catherine’s IR3 would look like this:

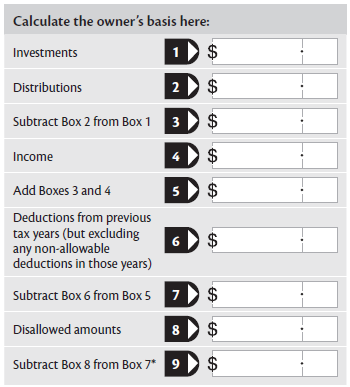

Calculate the owner’s basis here

* If Box 9 is a negative amount it means the owner has negative equity in the LTC and their owner’s basis will be treated as nil. Print “0.00” in Box 9.

Please note—deductions in Box 6 above also includes all the deductions claimed against gross income from the LTC from all sources in previous years in which the company was a LTC. For example, if the LTC has a rental property, all the deductions claimable against the rental income will be included in the total deductions figure, as well as expenses incurred in producing income from all other sources.

When each owner’s basis (Box 9 at Calculate the owner’s basis here) has been calculated you can work out if there is any limitation on the deductions claimable for each owner. If the:

-

owner’s basis (Box 9) is more than their attribution of the deductions (expenses), you won’t need to complete Box 24O—go to Non-allowable deductions.

-

attribution of deductions (expenses) to the owners are more than their owner’s basis you’ll need to complete Boxes 1 to 3 below to calculate the amount to declare at Box 24O.

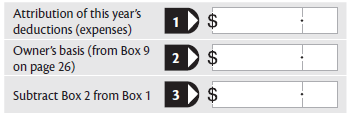

The result is non-allowable deductions this year. Copy the amount from Box 3 into Box 24O on your IR7L.

Any deductions an owner can’t claim because of the loss limitation rule are carried forward and may be claimed in future years, subject to the application of the loss limitation rule in those years. Owners may only use these deductions against income from the LTC.

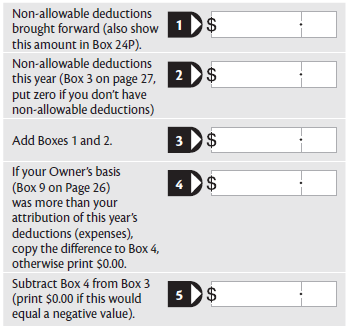

Non-allowable deductions

Complete the calculation (Boxes 1 to 5) below if you have:

-

non-allowable deductions brought forward from last year (copy the amount from Box 24R Non-allowable deductions on your IR7L 2018 form into Box 24P on your IR7L 2019 form) and/or

-

non-allowable deductions this year (that means Box 24O has an amount in it).

Prior years’ non-allowable deductions claimable this year

If there is a figure in Box 4, you will be able to claim prior years’ non-allowable deductions. Enter the smaller number of Box 3 and Box 4 as prior years’ non-allowable deductions claimed this year in Box 24Q on your IR7L.

Non-allowable deductions carried forward

The amount in Box 5 is the non-allowable deductions to carry forward. Copy this amount into Box 24R.