net income from rents (rents after expenses) in Box 8C.

Attach a breakdown of gross rents and expenses to show how the net rents were worked out. You may use an IR3R form.

Taxable Maori authority distributions

There are various types of distributions that can be made from Maori authorities. You are only required to declare taxable Maori authority distributions made from gross income that Maori authorities earned during the 2004–05 income year or subsequent income years.

Fill in Box 8B if you received any taxable Maori authority distributions between 1 April 2018 and 31 March 2019. The Maori authority that paid you the distribution sends you a Maori authority distribution statement.

Credits attached to distributions

The authority may attach a credit to the distribution it makes to members. This credit will be classified as a Maori authority credit and is part of the tax the authority has already paid on its profits so the distributions aren’t taxed twice.

What to show in your return

Your Maori authority distribution statement shows the amount of:

the distribution made to you, including what portion is taxable and what portion is non-taxable

Maori authority credit.

These amounts, not including any non-taxable distributions, will need to be transferred to the relevant boxes as follows:

Taxable Maori authority distributions should be shown in Box 8B.

Maori authority credits should be included in Box 9G.

Example

A Maori authority makes a pre-tax profit of $10,000. They pay tax on this profit of $1,750 (Maori authority tax rate of 17.5%) and distribute the entire profit to their 10 members. So, each member will receive $825 as a cash distribution and $175 of Maori authority credits. Authorities that are liable (as members) for filing an IR8 return of income would show the following information in their return:

Box 8B – $1,000 (made up of $825 + $175)

Box 9G – $175 (included with other tax credits)

Non-taxable distributions

Any other distributions received from a Maori authority, which aren’t taxable in the hands of a Maori authority member, don’t need to be included in the IR8 return. These amounts are classed as non-taxable distributions and can’t have credits attached.

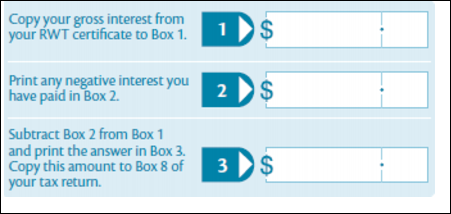

Interest on broken term deposits

If you’ve broken a term deposit during the year, there may be “negative interest” to account for. This is interest repaid on term deposits. This may reduce the amount of interest to declare on the tax return.

If the term deposit was broken in full, or it was business-related, deduct the negative interest from the gross interest shown on the RWT certificate (IR15 or equivalent statement).

Deduct the allowable negative interest component using the worksheet below before entering the gross amount at Box 8 of the tax return. In all other cases the negative interest is deductible in a later tax return when the term deposit matures.

Worksheet

Interest paid and charged by Inland Revenue

Include any interest paid by us in Box 8. If Inland Revenue pay interest include this in the return for the income year you received it. If you paid interest, include it in the return for the year it is paid. (Only offset interest paid in Box 8 if it hasn’t been claimed as a deduction in your accounts.)

If the overall interest is a loss, put a minus sign in the last box at Box 8.

RWT withheld

Any RWT withheld should be shown in Box 9E.

If the overall interest is a negative amount, print the total in Box 8 and put a minus sign in the last box.

Box 8D Net income

This is the amount of business income that the authority earned after deducting the allowable business expenses. If the authority made a loss, put a minus sign in the last box.

If expenses are deductible against income declared in Box 8 or 8A, claim them at Box 8G. Attach either:

a fully completed Financial statement summary (IR 10) form, or

a set of the authority’s financial accounts.

The Financial statement summary (IR10) is a short form of the financial statements of a business. Use an IR10 and speed up processing of the return. We don’t need a set of accounts if you use an IR10. You still need to complete a set of financial accounts and keep them in case we ask for them later. For help with filling out the IR 10, please see the IR10 guide.

Box 8E Other income

Show any other income received by the authority at Box 8E.

If you received income from overseas, such as interest, a foreign investment fund (FIF) or a controlled foreign company (CFC), convert your income to New Zealand dollars and show it at Box 8E. If your overseas income is from an FIF or a CFC you may need to file an additional disclosure. Read the notes to Question 13 at IR8 Question 13 Foreign rights.

Overseas income

You can convert all overseas income and tax credits to New Zealand dollars by:

using the rates table available on www.ird.govt.nz (keywords: overseas currencies)

using the mid-month conversion rates in our leaflet Conversion of overseas income to New Zealand currency (IR 270)

contacting the overseas section of a trading bank and asking for the exchange rate for the day you received your overseas income.

If the income was received from a financial arrangement, refer to Determination G9A or G9B prescribed under section 90 of the Tax Administration Act 1994.

Have you received any income from the sale/disposal of property?

Show any income from taxable property sales at box 8E of the return, if not already included elsewhere in the return. A Property sale information (IR833) may also need to be completed if not already done.

Under the bright-line test for the sale/disposal of property, if the Maori Authority acquired residential property on or after 1 October 2015, and solid it within two years, any gain will need to be accounted for.

FIF income

If at any time during the 2019 income year the Maori authority held rights such as shares, units or an entitlement to benefit in any foreign company, unit trust, superannuation scheme or life insurance policy, you may be required to calculate FIF income or loss. Generally, the company will use the new fair dividend rate to calculate FIF income.

The main exclusions from an interest in an FIF are:

investments in certain Australian resident companies listed on approved indices on the Australian stock exchange, that maintain franking accounts

interest in certain Australian unit trusts

limited exemptions for interest in certain venture capital interests that move offshore (for 10 income years from the income year in which the company migrates from New Zealand)

a 10% or greater interest in a CFC

a trustee of certain trusts who holds, at all times in the income year, FIFs with a total cost of $50,000 or less.

Under the FIF rules, dividends received from overseas companies, except companies covered by the above exclusions, are not taxable separately. Generally, the authority would use the default FIF income calculation method, called the fair dividend rate, which doesn’t tax dividends separately. However, the foreign tax deducted from the dividend can be claimed as a credit against the tax payable on the calculated FIF income.

CFC income and losses

If you have an interest in a CFC, you must calculate any attributed income or loss from that interest.

There are rules for calculating income or losses from a CFC. Entities with balance dates from 30 June to 30 September are required to apply these rules from the beginning of the 2010 income year. All other entities are required to apply the rules from the beginning of the 2011 income year.

Losses from a CFC can’t be used to offset domestic income or be included in domestic losses that are being carried forward to the 2020 tax year. Generally, such losses can only offset income or future income from CFCs that are resident in the same country as the CFC that incurred the loss.

When CFC income or losses are calculated under these rules there are transitional rules that apply to the use of carried forward losses incurred under the old rules.

Further information on the taxation of interests in CFCs is available at www.ird.govt.nz/toii/cfc and in the Tax Information Bulletins (TIBs)—see the online index for relevant issues.

Investments in portfolio investment entities (PIEs)

Certain PIEs attribute their net income/loss and tax credits they derive across their investors. Investors that are Maori authorities include the attributed income or loss in their tax return.

Each year the PIE is required to provide an investor statement setting out the details of the income/loss attributed to the investor for the year. The statement also shows the various types of tax credits associated with the income attributed.

These tax credits are subject to the tax credit limits calculated in relation to the tax on the attributed PIE income.

The attributed PIE income/loss is included in the authority’s return for the period that includes the end of the PIE’s income year. Generally, PIEs will have a 31 March balance date. The amount of income derived by the authority as a distribution by a PIE is excluded income of the authority other than fully imputed dividends from a PIE that is a listed company. Refer to the website www.ird.govt.nz (keyword: PIE).

Australian dividends

Australian companies can pass on credit for tax paid in New Zealand to their shareholders if they maintain a New Zealand imputation credit account.

If an Australian company which you hold shares in has elected to maintain a New Zealand imputation credit account, you may see a “New Zealand imputation credit” on your dividend statement.

This does not mean:

Australian imputed or franking credits can now be claimed

dividends from certain Australian companies, not covered by the FIF Australian exemption, will not be included in the return because the dividend income will be covered by the calculation of FIF income.

Taxable property sales

If the authority invested in residential property on or after 1 October 2018 and sold/disposed of it before the end of the income year, any profit is taxable income, even if there was no intention to sell when it was purchased.

Show the net profit as part of the income total in Box 8E. If there is a net loss it can only be offset against income from other property sales/disposals.

Complete a Property sale information (IR833) form for each property sold/disposed of and include it with the return. The form explains how to calculate and correctly return the resulting profit or loss. You can download the form from the Inland Revenue website www.ird.govt.nz (search keyword: IR833). Complete the form even if the details have been included in a Financial statements summary (IR10) or set of accounts.

Residential land withholding tax (RLWT) credit

If the authority is an “offshore RLWT person” and has sold or transferred residential property located in New Zealand, RLWT may have been deducted from the sale price. The authority should have received a statement on the completion of the sale process showing the amount of RLWT deducted. The authority can claim a credit for any RLWT deducted. Show the amount of RLWT deducted, less any RLWT paid back to the authority and/or transferred to outstanding amounts during the income year.

If there was more than one amount of RLWT deducted, show the combined amount, less any RLWT paid back to the authority and/or transferred to outstanding amounts during the income year.

Box 8I Donations to Maori associations or donee organisations

The authority can claim a deduction for any donations it makes to a Maori association within the meaning of the Maori Community Development Act 1962. A Maori association includes a Maori committee, a Maori executive committee, a district Maori council and the New Zealand Maori Council. The authority may also claim a deduction for any donations it makes to any society, institution, organisation or trust that has approved donee status, for example, kohanga reo and Maori health boards. You can view a complete list of approved donee organisations at www.ird.govt.nz or call 0800 377 774 for assistance.

The deduction for donations can’t be more than the authority’s income after expenses (before the donation deduction is taken into account). Use the following steps to determine the donation deduction.

If the answer in Box 8H is a loss, print nil in Box 8I.

If the donations made by the authority exceed Box 8H, copy the amount in Box 8H to Box 8I.

If donations made by the authority don’t exceed Box 8H, print the amount of the donations in Box 8I.

Box 8K Losses brought forward

If the authority is bringing forward losses from previous years, show the total in Box 8K.