IR9 Types of income for organisations - Q11 and Q12

Interest and dividends

Show any gross net interest received in Box 11 or 12, and any dividends in Box 11A or 12A. Costs incurred in deriving the interest can be deducted before entering the amount in Box 11 or 12. This includes interest paid by Inland Revenue.

Interest on broken term deposits

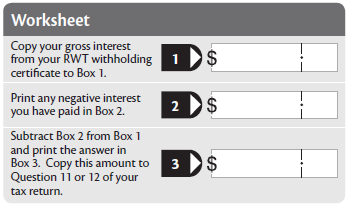

If you have broken a term deposit during the year, there may be “negative interest” to account for. This is interest repaid on a term deposit. This may reduce the amount of interest to declare on the tax return.

If the term deposit was broken in full, or it was business-related, deduct the negative interest from the gross interest shown on the RWT withholding certificate (IR15 or equivalent statement).

Deduct the allowable negative interest component using the worksheet below before entering the gross amount at Question 11 or 12 of the return. In all other cases, the negative interest is deductible in a later return when the term deposit matures.

Interest paid or charged by Inland Revenue

Include any interest paid by Inland Revenue as income in the year it is received, or if you paid interest to Inland Revenue for late payment of tax, it is allowed as a deduction in the tax year the interest is paid. If your overall interest is also a negative amount, put a minus sign in the last box.

Taxable Maori authority distributions

Maori authorities can make various types of distributions. You’re only required to declare taxable Maori authority distributions made from gross income that Maori authorities earned during the 2004–05 income year or subsequent income years.

Fill in Box 11B or 12B if you received any taxable Maori authority distributions between 1 April 2018 and 31 March 2019. The Maori authority that paid you the distribution sends you a Maori authority distribution statement.

Credits attached to distributions

The Maori authority may attach a credit to the distribution it makes to members. This credit will be classified as a “Maori authority credit” and is part of the tax the Maori authority has already paid on its profits so the distributions are not taxed twice.

What to show in your return

Your Maori authority distribution statement shows:

the amount of the distribution made to you, including what portion is taxable and what portion is non-taxable

the amount of Maori authority credit.

These amounts, not including any non-taxable distribution, will need to be transferred to the following boxes:

taxable Maori authority distributions should be shown in either Box 11B or 12B

Maori authority credits should be shown in “other tax credits” Box 18I.

Example

A Maori authority makes a pre-tax profit of $10,000. They pay tax of $1,750 on this profit (Maori authority tax rate of 17.5%) and distribute the entire profit to their 10 members, so each member will receive $825 as a cash distribution and $175 of Maori authority credits.

Each member of the authority liable to file an IR9 return would show the following information:

Box 11B or 12B – $1,000 (made up of $825 + $175)

Box 18I – $175

Non-taxable distributions

Any other distributions received from a Maori authority, which are not taxable in the hands of a Maori authority member don’t need to be included in the IR9 return. These amounts are classed as non-taxable distributions and can’t have credits attached.

Other income

Print the net profit in Box 11C or 12C. The net income is the gross income less expenses related to earning the income. If it is a negative amount, put a minus sign in the last box.

Overseas income

You can convert all overseas income and tax credits to New Zealand dollars by:

using the rates table available on www.ird.govt.nz (search keywords: overseas currencies)

contacting the overseas section of a trading bank and asking for the exchange rate for the day you received your overseas income.

Australian dividends from non-foreign investment fund investments

If you hold shares in an Australian company which has elected to maintain a New Zealand imputation account, you may see a “New Zealand imputation credit” on your dividend statement. It’s possible for dividends to be paid with these credits attached. Show any Australian dividend income at Box 11A or 12A. Claim the New Zealand imputation credits in the dividend imputation credits box at Question 18C and include overseas tax credits at Question 18A.

This does not mean Australian imputed or franking credits can now be claimed. Inland Revenue approval may be required for an exemption from income tax.

Foreign-sourced dividends

Under the foreign investment fund (FIF) rules, dividends received from overseas companies may no longer be separately taxable. Generally, clubs or societies would use the default FIF income calculation method, called the fair dividend rate (FDR), which does not tax dividends separately. However, the foreign tax deducted from the dividend can be claimed as a credit against the tax payable on the calculated FIF income. To learn more about FIF rules go to www.ird.govt.nz/toii/fif/

Foreign rights

If you’re calculating controlled foreign company (CFC) or FIF income you may be required to complete an additional disclosure form for that investment.

The types of foreign investment that may not require an additional disclosure are investments in countries New Zealand has a double tax agreement with as at 31 March 2019, which have used the comparative value (CV) or FDR method.

If you need assistance making a CFC disclosure please call 0800 377 774 to get the appropriate disclosure form.

Full details of the disclosure requirements are available in the Tax Information Bulletins (TIBs). The disclosure forms are available from www.ird.govt.nz

Portfolio investment entities (PIEs) and attributed PIE income/loss

Certain PIEs attribute their net income/loss, and tax credits they derive, across their investors. Clubs or societies that are investors include the attributed income or loss in their tax return.

Each year, the PIE is required to provide an investor statement setting out the details of the income/loss attributed to the investor for the year. The statement also shows the various types of tax credits associated with the income attributed. These tax credits are subject to the tax credit limits calculated in relation to the tax on the attributed PIE income.

The attributed PIE income/loss is included in the club or society’s return for the period that includes the end of the PIE’s income year. Generally, PIEs will have a 31 March balance date.

Taxable property sales

Under the bright-line test for the sale/disposal of property, if the club or society invested in residential property on or after 1 October 2015 and sold/disposed of it within the bright-line period, any profit is taxable income, even if there was no intention to sell when it was purchased. The bright-line period for:

properties purchased/acquired on or after 1 October 2015 through to 28 March 2018 inclusive, is two years,

properties purchased/acquired on or after 29 March 2018 is five years.

Show the net profit as part of the income total in Box 11C or 12C. If there is a net loss it can only be offset against income from other property sales/disposals.

Complete a Property sale information (IR833) form for each property sold/disposed of and include it with the return. The form explains how to calculate and correctly return the resulting profit or loss. You can download the form from the Inland Revenue website www.ird.govt.nz (search keyword: IR833). Complete the form even if the details have been included in a Financial statements summary (IR10) or set of accounts.

Box 12E Income deduction for non-profit bodies

A non-profit body can claim a deduction of up to $1,000. This deduction is the smaller of:

the amount at Box 12D, or

$1,000.

If the organisation’s income is less than $1,000 before the deduction, it will have no taxable income.

This deduction is not available to organisations covered by Questions 10 and 11.

If your organisation has an exemption from RWT as a non-profit body, it does not necessarily mean it has non-profit status and is exempt for income tax purposes.