To claim this expense as a deduction you need to answer Yes the question:

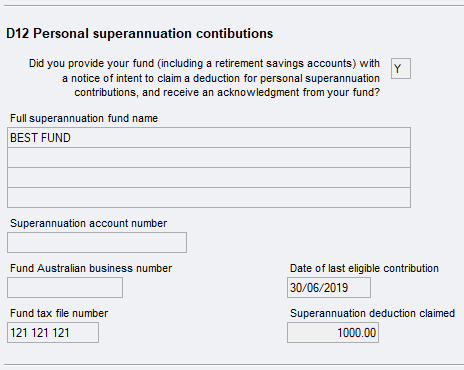

Did you provide your fund (including a retirement savings account) with a notice of intent to claim a deduction for personal superannuation contributions, and receive an acknowledgement from your fund?

See Personal superannuation contributions (psc) 2023.

You cannot claim a deduction for personal superannuation contributions if:

-

your personal superannuation contributions were not received by your superannuation fund or RSA provider before 1 July 2019 – contributions received by the superannuation fund or RSA provider after 30 June 2019 can only be claimed as a deduction in the following income year (2019–20), even if you took steps (such as posting a cheque, or initiating a direct debit) prior to 30 June 2019

-

you made the contributions more than 28 days after the end of the month in which you turned 75 years old

-

you were under 18 years old on 30 June 2019 and you did not receive any income from activities that resulted in you being treated as an employee for the purposes of the superannuation guarantee law or from you carrying on a business

-

either of the following applied to you

-

you made a contribution that was attributable, either in whole or in part, to a capital gain that you made and you chose to apply the small business capital gains tax retirement exemption to all or part of that capital gain, and you were under 55 years old just before you made that choice, or

-

the contribution was attributable, either in whole or in part, to a capital gain and a company or trust chose to apply the small business capital gains tax retirement exemption to all or part of that capital gain, and you were under 55 years old just before the contribution was made

-

-

you did not provide your superannuation fund or RSA provider with a valid notice of intent to claim a deduction in the approved form

-

you made contributions to a superannuation fund or RSA provider that are attributable to the following super housing measures

-

downsizer contributions

-

re-contributions of amounts released under the First home super saver (FHSS) scheme, or

-

-

you provided your superannuation fund or RSA provider with a valid notice of intent to claim a deduction in the approved form but you have not received an acknowledgment of this notice from your superannuation fund or RSA provider.

You can have more than one psc worksheet. The ATO allows up to 25 psc worksheets.

If you have made eligible contributions to more than one complying superannuation fund or a retirement savings account, create a separate psc worksheet for each. If there is only one schedule, there is no Index. Creating the second worksheet creates the Index. Click the New button to create the second and additional worksheets.

Click label H to open the psc worksheet.

When you close the worksheet we'll add up all the entries and pass the total to item D12: label H:

The Personal superannuation contributions worksheet (psc) populates label H with the Amount of contribution.