New Zealand

An Imputation Credit Account is an off-balance sheet, information account used to keep track of how much income tax the company has paid, and how many imputation credits it holds to pass onto its shareholders.

When a company pays income tax, the company gains the same amount of tax paid, in the form of imputation credits. These imputation credits can then be attached to dividends paid to shareholders by the company.

There are two Imputation Credit Account (ICA) notes available in Stat Reporter:

-

The Imputation note NTD is a simple paragraph using non-transaction data (NTD) values to disclose the balance of the Imputation Credit Account for this year and last year.

-

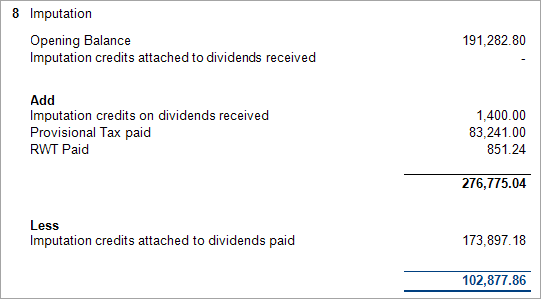

The Imputation Note provides a detailed analysis of the Imputation Credit Account with the Opening Balance, plus or minus movements to derive the closing balance.

By default, the Imputation note NTD is selected to appear in the Notes to the Financial Statements when generating reports for your client using Statutory Reporter. To display the detailed Imputation Note, this needs to be selected manually from the list of all reports.

If you prefer to use the detailed Imputation note in your client's financials, select the detailed Imputation note from the list of available reports in the Selecting default practice reports. The detailed note will be selected by default for all clients of the same entity type across the practice.

About the detailed Imputation note

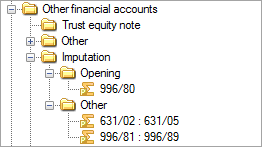

The detailed Imputation Note displays the balance of accounts in the Other financial accounts > Imputation account group. For an AO GL chart of accounts, the accounts in this group are:

-

996/80 - the Imputation Credit Account consisting of the opening balance (brought forward from last year's closing balance).

-

996/81 - 996/89 - the range of accounts to record other movements in the Imputation Credit Account. For example, Imputation Credits attached to Dividends paid.

-

631/02 - 631/05 - accounts used to capture tax paid during the year.

Imputation credits attached to Dividends paid

Imputation credits attached to Dividends received

There are two ways to handle imputation credits on dividends received:

A) Gross up dividends received in the Income Statement

When dividends are received, the journal entry would be:

|

Account Code |

Description |

Debit |

Credit |

|---|---|---|---|

|

631/04 |

Dividend withholding tax on dividends received |

$ xxxxx |

|

|

631/05 |

Imputation Credits on dividends received |

$ xxxxx |

|

|

600 |

Bank account |

$ xxxxx |

|

|

272 |

Dividends received |

$ xxxxx |

This approach requires no additional adjustments or manual mapping of account groups and, will work in both the Tax Note and the Imputation Credit account note.

B) Show net dividends received in the Income Statement

With this approach, dividends received are shown at the net amount received (including any withholding tax), and the difference between accounting profit and taxable income is adjusted for in the Tax Note as a permanent difference. There are several pieces here:

To record imputation credits on dividends received:

|

Account Code |

Description |

Debit |

Credit |

|---|---|---|---|

|

996/82 |

Imputation credits on dividends received |

$ xxxxx |

|

|

996/99 |

Information accounts contra |

$ xxxxxx |

By default, the 996/82 - Imputation credits on dividends received account is mapped to the Other financial information > Out of Range account group. This account will need to be re-mapped into the following account groups:

-

Other financial information > Tax Note > Non-assessable non-deductible (to appear in Tax Note).

-

Other financial information > Imputation > Other (to appear in Imputation note).

Duplicate mapping is required to display imputation credits attached to dividends received in both the Tax Note and Imputation note. We recommend performing this account mapping at a Practice Level to avoid the duplicate mapping message when reports are generated.

To record dividend imputation credits to be claimed against this year's tax:

|

Account Code |

Description |

Debit |

Credit |

|---|---|---|---|

|

996/90 |

Imputation credits utilised this period |

$ xxxxx |

|

|

996/99 |

Information accounts contra |

$ xxxxxx |

The amount debited to 996/90 Imputation credits utilised this period will usually be the same as the amount debited to 996/82 - Imputation credits on dividends received. However, this needs to be a different account to allow for excess imputation credits that cannot be utilised.

The account 996/90 - Imputation credits utilised this period does not affect the Imputation note however, it must be taken into account in the tax reconciliation note.