Release date—June 2024

This is the latest version for:

-

Accountants Enterprise (AE)—MYOB AE 2024.0

-

Accountants Office (AO)—MYOB AO 2024.0.

Update 6 August

We’ve released Tax 2024.0b KB253689907 hotfix (Australia). Make sure to install the hotfix as it includes tax fixes and the Small business entity threshold changes and other fixes.

2024 Tax webinar

Learn about the ATO's 2024 tax compliance changes, access the 2024 tax tables, and new workflows in MYOB Practice tax. Register for a free MYOB tax webinar.

.png?cb=1ca0617a4ab5348b5bb5d4c16fe8a529)

What’s changing in AE/AO

Activity statements are moving online

After installing 2024.0, you can no longer create new Activity statements in AE/AO.

If you have any existing activity statements, you can complete and lodge them by 30 September. After that, you can only amend activity statements.

|

Version/timeline |

Create new

|

Pre-fill/Pre-lodge |

Lodge

|

Amend (existing statements) |

|---|---|---|---|---|

|

Tax version 2024.0 (till 30 September 2024) |

No |

Yes |

Yes |

Yes |

|

Tax version 2024.0 and prior (after 30 September 2024) |

No |

No |

No |

Yes |

See Activity statement EOL FAQs for more information.

Upgrading to SQL 2019 is not mandatory before installing 2024.0. You can install 2024.0 and upgrade SQL later.

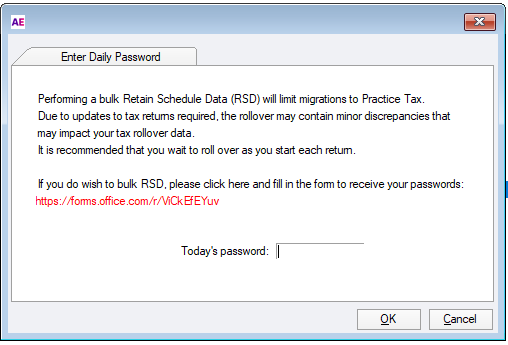

Bulk RSD changes (AE only)

We’ve made some changes to the Bulk RSD routine. As we move towards the more streamlined online workflow in MYOB Practice tax, we recommend rolling over tax returns one at a time so the data rolls over accurately when you move online.

What are the changes?

When you perform a bulk RSD rollover after installing 2024.0, you’ll see a message to enter Today’s password.

To get the password click the form link and complete the details. We’ll then send you the password.

The passwords are valid only on the day mentioned and will expire afterwards. You’ll not be able to perform the Bulk RSD without entering the password.

2024 Tax changes

Multiple returns

Trust income schedule

As part of ATO’s change to Modernising trust administration systems, the ATO has introduced a Trust income schedule. This will assist with the correct income reporting and consistency across all beneficiary types required to lodge their tax return.

Read about the Trust income schedule on the ATO’s website.

Changes in MYOB Tax

The Trust income schedule layout is different depending on the return type.

-

Individual return: The Distributions received from trust (dit) worksheet has been modified to include all the fields required to complete the Trust income schedule.

-

Company, Fund, Partnership, SMSF, Trust: A new schedule called Trust income schedule (DISTBEN) has been included.

Small business instant asset write-off

Update on 1 July 2024

The threshold to increase the Small business instant asset write-off to $20,000 has passed both houses and received Royal Assent.

We’ve updated the threshold to $20,000 in Tax 2024.0a KB224821282 hotfix (Australia) release.

Read about the Small business asset instant write-off on the ATO’s website.

Temporary full expensing has ended

Temporary full expensing method for assets has ended on 30 June 2023.

You can't claim deductions under temporary full expensing for assets delivered, installed ready for use or improved after 30 June 2023.

Read about the Temporary full expensing on the ATO’s website.

We’ve removed the temporary full expensing labels in the following return types.

|

Individual |

Company |

Trust |

Partnership |

|---|---|---|---|

|

Item P11 label C |

Item 9 Label P |

Item 50 label P |

Item 49 label P |

|

Item P11 label D |

Item 9 Label Q |

Item 50 label Q |

Item 49 label Q |

|

Item P11 label E |

Item 9 Label R |

Item 50 label R |

Item 49 label R |

|

Item P11 label F |

Item 9 Label S |

Item 50 label S |

Item 49 label S |

|

Item P11 label G |

Item 9 Label T |

Item 50 label T |

Item 49 label T |

|

|

Item 9 Label U |

|

|

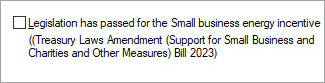

Small business energy incentive

Update on 1 July 2024

This Small business energy incentive measure has passed both houses and receives Royal Assent.

Follow the steps below to enable small business labels.

-

Open a 2024 return

-

Go to Utilities > Control Record > and select Legislation has passed for the small business energy incentive.

-

Now close and open the tax return. This will enable the labels for data entry.

The Small Business technology investment boost has ended, and ATO introduced the Small business energy incentive label.

Read about the Small business energy incentive on the ATO’s website.

Small businesses (with an aggregated annual turnover of <$50 million) can get access to a bonus deduction equal to 20% of the cost of eligible assets or improvements to existing assets that support electrification or more efficient energy use.

We’ve added the following labels so you can claim any eligible deductions.

|

Return type |

New labels |

|---|---|

|

Individual |

Item P12 Small business bonus deduction Label O Small business energy incentive |

|

Company |

Item 7 - Label K Small business energy incentive |

|

Trust |

Item 52 Small business bonus deductions Label C Small business energy incentive |

|

Partnership |

Item 52 Small business bonus deductions Label C Small business energy incentive |

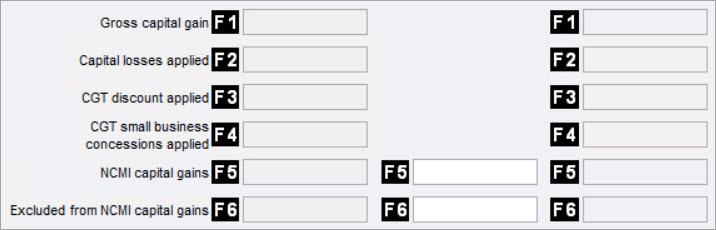

Trust tax returns

New capital gains labels

Read about the 2024 trust return changes on the ATO’s website.

As part of ATO’s change to Modernising trust administration systems, the ATO has introduced 4 new capital gains labels to the beneficiary distributions.

Use these labels to notify beneficiaries of their entitlement to income, and support the calculation of their CGT amount in their tax return.

These capital gain labels integrate into the respective labels that are being distributed into.

New validation rules from ATO

-

TRT.433088 - Type of trust must be a 'deceased estate' - code '059'

-

TRT.433089 - Type of trust must be a 'deceased estate' - code '059'

-

TRT.433090 - Type of trust must be a 'deceased estate' - code '059'

-

TRT.433091 - Type of trust must be a 'deceased estate' - code '059'

-

TRT.433102 -The beneficiary address and at least one positive TB statement information amount must be provided

-

TRT.433103 - The beneficiary address and at least one positive TB statement information amount must be provided

ATO has introduced these new errors in a 2024 trust return.

To fix these errors, make sure you’ve completed:

-

The Family trust election or Interposed entity election status field on the Front Cover

or -

the TB statement question on the Distribution statement.

Client Accounting

Need help?

We're here to support you through this busy tax season.

Extended support hours

Phone: 1300 555 117 Fast key code 3 1

-

Monday 1 July 2024 - Friday 5 July 2024

8.00 am – 7.00 pm AEST -

Saturday, 29 June 2024 - Sunday, June 30 2024

9:00 am - 5:00 pm AEST. -

Saturday, 6 July 2024 - Sunday, 7 July 2024

9:00 am - 5:00 pm AEST. -

Saturday, 13 July 2024 - Sunday, 14 July 2024.

9:00 am - 5:00 pm AEST.

Outside of these times, our support hours are:

-

Monday to Friday

9:00 am to 5:00 pm

Submit a support request via my.myob

Check out our community forum.